Rising interest rates: When will it end?

By BDC

MONTREAL, Canada – Between runaway inflation and rapidly rising interest rates, cost pressures have been mounting for consumers and businesses in Canada. These are conditions Canadians have not been experienced in a long time and the impact can be felt from real estate to financial markets to everyday prices and wages. The era of cheap money is over, but how high will rates go? It all depends on inflation.

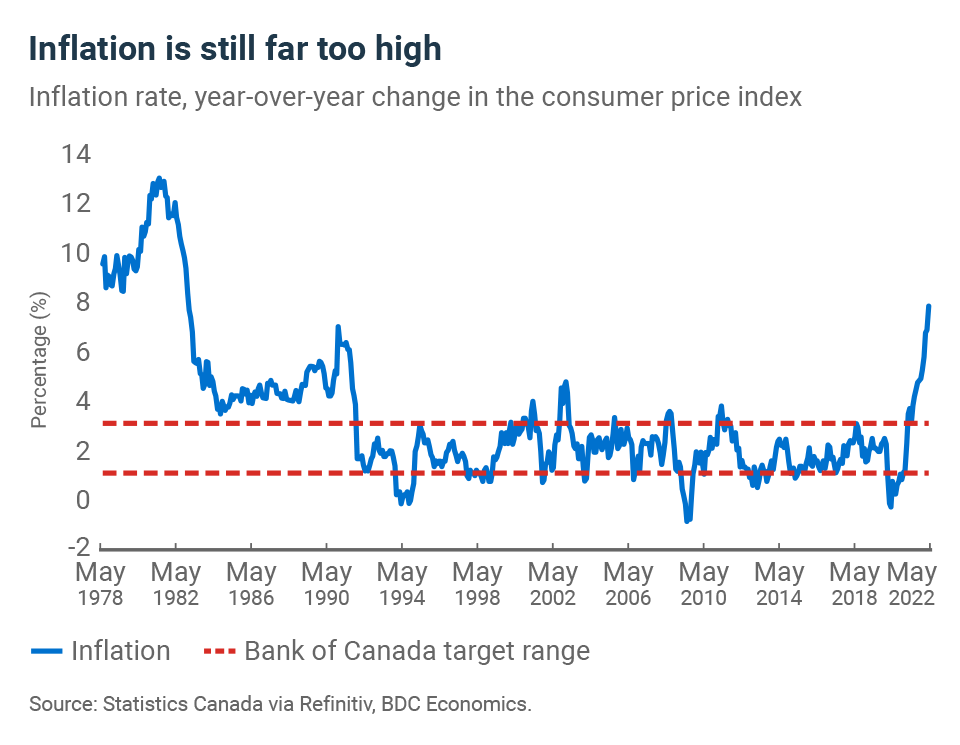

Inflation to break new records this summer

Inflation has been accelerating since the reopening of economies around the world from COVID lockdowns. It’s causing an inflationary shock that is stretching longer than expected, fueled by persistent supply chain disruptions and the war in Ukraine.

The good news is that the inflation picture should get better with time. Supply chains are showing encouraging signs of improvement as businesses diversify their suppliers. And while the war and accompanying sanctions on Russia are still hampering several commodity markets – notably food and energy – the worst of the initial shock appears to be behind us.

{kind=link}

On the other side of the coin, price increases will remain substantially higher than those observed a year earlier for several more months.

Shortages have led companies to massively boost inventories with many businesses moving from “just-in-time” inventory management to “just-in-case.” As they try to meet high demand and build inventories, they are contributing to further clogging of transportation networks.

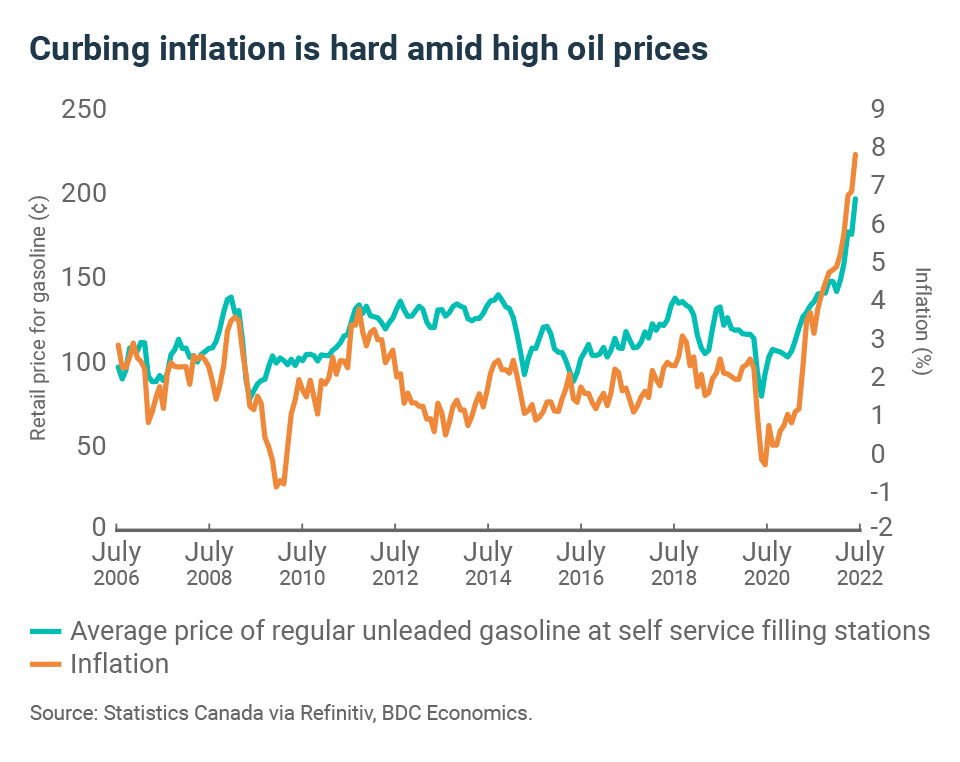

Oil prices are pushing prices higher

High oil prices are also contributing to inflation as global crude supply struggles to meet demand. Obviously, surging oil prices are being felt by motorists at the pump, but they are also having significant spillover effects elsewhere in the economy. For example, energy is a major input in commodity production and distribution.

While businesses are passing on cost increases to consumers, Canadian households remain resilient, at least for the time being. According to a recent BDC survey, 25 percent of Canadians have not changed their spending habits because of inflation and the rest say they’re more likely to search for bargains than to restrict their purchases.

We believe it will likely take until the beginning of the new year before inflation falls below 5 percent and until the spring of 2023 before it returns to the Bank of Canada’s target range of between 1 percent and 3 percent. That said, while inflation will continue to break records in Canada over the summer, we don’t expect to hit double digits.

{kind=link}

No choice but to hike rates

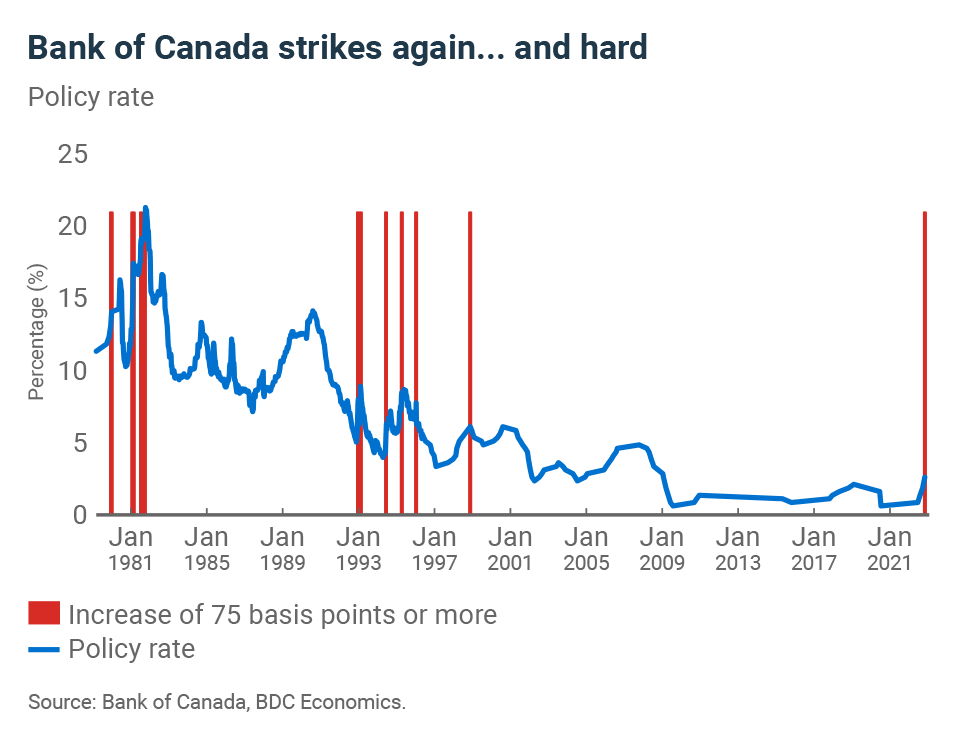

Faced with high levels of inflation and tight labour markets, central banks have no choice but to act aggressively.

Clearly, the Bank of Canada is determined to do what it takes to achieve relative price stability as evidenced by the latest 100 basis-point hike in its policy rate. That hike brought interest rates closer to what economists consider a neutral rate – one that neither stimulates the economy nor holds it back. However, monetary policy will likely need to move above the neutral rate for some time to allow supply and demand to rebalance and for the risk of high inflation to recede.

{kind=link}

A period of unusually low rates

In 2008-2009, central banks around the world adopted extremely low interest rates in response to the financial crisis. The US Federal Reserve lowered its key interest rate to 0 percent in December 2008 in an effort to stimulate the economy. It kept it at that level until December 2015 when it began to modestly raise the rate until it reversed the trend once again in response to the pandemic.

In the face of the financial crisis, the Bank of Canada lowered its rate to 0.25 percent in June 2010. Economic conditions allowed it to keep the policy rate at 1 percent until January 2015 when it had to be lowered again in response to plummeting oil prices.

This long period of abnormally low rates lasted so long that it seems to have become firmly entrenched in the expectations of Canadians for where rates should be, even when the economy is strong.

{kind=link}

We believe household and government indebtedness is high enough that the policy rate should peak at 3 to 4 percent in Canada. The most recent Bank of Canada announcement on July 13 brings it to 2.5 percent and we now expect it will reach 3 percent by the end of the year. This will still be low by historical standards, just not what we had come to expect during the recent period of ultra-low rates.

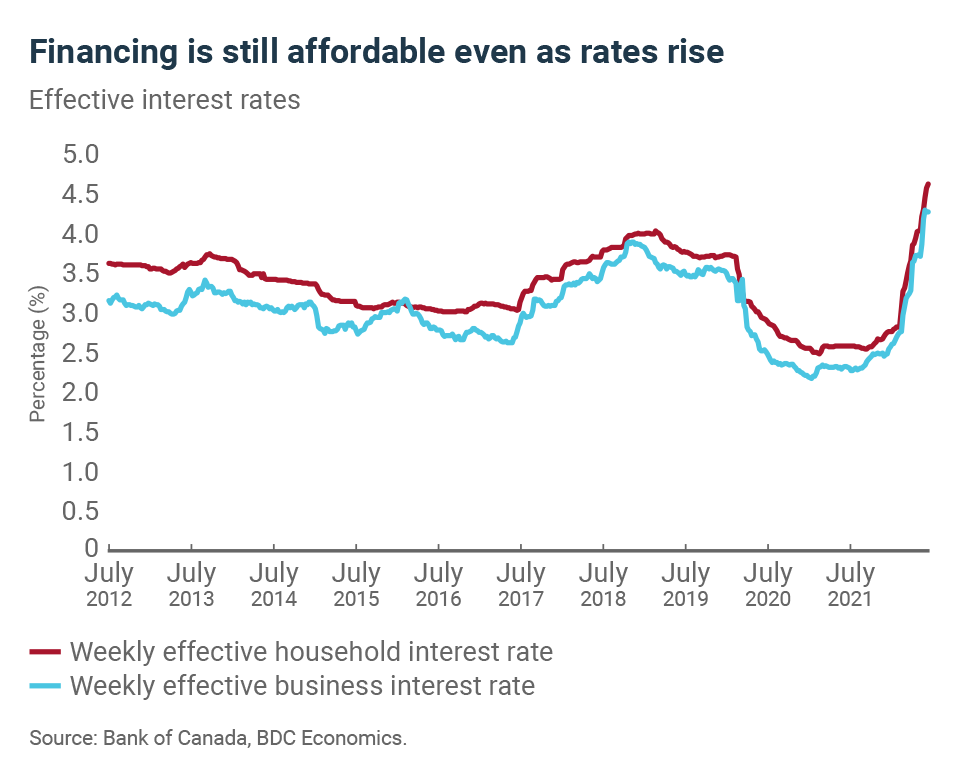

While the interest rate environment in the coming years will look different than what we’ve seen in recent years, this is not bad news. The risks of sustained inflation remain high. Despite the discomfort of rapid rate increases, they’re necessary for the economy to return to a healthy and sustainable pace of growth.

Source: caribbeannewsglobal.com