AM Market Report – November 10, 2025

ICE canola futures are trending $2 to $3/tonne lower this morning, pushing overnight lows, with the nearby Jan contract down $2.50 at $637.50/tonne. Canola futures were supported last week by the upward move in soybeans, with the benchmark Jan contract trading up $3/tonne for the week ended Friday.

Note that ICE canola futures will be closed Tuesday for Remembrance Day…and there will be no AM Market Report.

US grain markets are higher this morning, supported by the news late Sunday that the US Senate is moving closer to agreeing on a deal to reopen the US government.

Chicago soybean futures are trading up 2 to 7 cents/bu, led by the front month contracts. Although daily price fluctuations occurred, the Jan soybean futures contract gained only 1.75 cents for the week ended Friday amid a potential topping pattern on price charts following the October tally.

Soybeans traded to a 16-month high last week before facing corrective selling late in the week as China s return to the US soy market remains a matter of debate given the Asian giant s lack of follow-through buying interest of US beans after the much-hyped Trump-Xi trade agreement. For soy complex futures traders, the meal market will also be one to watch closely. As goes the meal futures market in the near term, so will likely go soybeans.

CBOT corn futures are fractionally to 2 cents higher right now. The corn markets sputtered late last week. Dec corn futures saw another week of sideways trade, though we saw wide daily ranges as prices bounced between technical levels. Traders are caught between strength in soybeans and wheat and record US corn production. Friday s technically bearish weekly low closes in corn may still put the bulls on the defensive early this week. A price uptrend on the daily chart for Dec corn may be rolling over and bulls need to show more power soon to keep it alive.

US wheat markets are higher as well…winter wheats rising 5 to 8 cents and spring wheat futures up 1 to 5 cents. But similar to corn, recent wheat market gains were threatened last week. Spring wheat remains the weakest trender of the US wheat complex…edging sideways in narrow trade last week, crimped by technical resistance, though seller-interest lacked simultaneously. Recent price action suggests a breakout may transpire, which would confirm whether or not the Oct. 21 low marked a near-term bottom.

Traders in all ag markets remain uncertain about where to position their bets and will await USDA guidance on Friday (Nov 14) with the next supply/demand report. Meanwhile, expect continued choppy trading, especially as speculation about Chinese purchases is likely to be a key focus during the week.

In Other News

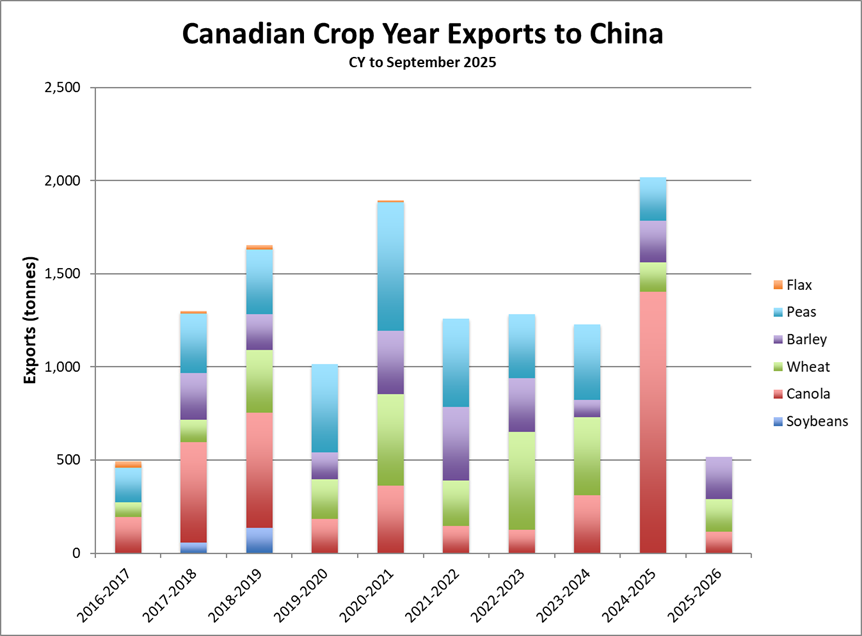

– Notable changes in exports to China, India... MarketsFarm reporter Glen Hallick writes that China and India figured prominently in the September export data issued by the Canadian Grain Commission on Nov. 7. For the most part, the CGC s numbers highlighted issues with grain, oilseed and pulse exports from licensed facilities to those countries.

For September, total Canadian exports worldwide were nearly 3.71 MMT compared to 3.87 MMT the same month a year ago. At two months into the 2025/26 crop year, Canadian licensed facilities shipped out about 5.86 MMT versus 6.77 MMT the previous September.

Trade action taken by China against Canada generated notable declines in the former s canola and pea imports. Currently, Beijing has its 75.8% tariff on China s intake of Canadian canola seed along with 100% levies on canola oil and meal as well as yellow peas.

That has seen China s purchases of canola seed from Canada tumble to a mere 113,900 tonnes compared to more than 1.4 MMT a year ago. Peas held at zero, while those imports were 233,000 tonnes the previous September. Added to that, China s imports of Canadian lentils were also at zero versus 20,700 tonnes last September.

A sudden about-face in Indian trade policy will set Canadian pea exports to that country on a downward slide. As October wrapped up, the Indian government announced it would impose a 30% tariff on its yellow pea imports effective Nov. 1. Although rumours of such a move began circulating in September, the Indian government remained on course to maintain its latest duty-free period until March 2026. Reports said pressure from the country s sizeable farm lobby pressured the government into an earlier-than-expected change as to prop up domestic prices.

India imported 397,500 tonnes of peas from Canadian licensed facilities during September, up from 387,100 a year ago. The government said the duty will apply to yellow pea imports dated after Nov. 1, so any sharp drop in Canadian exports to India won t be seen in the CGC s report for a few months.

Despite India having a 10% surcharge on its lentil imports, those from Canada soared to 173,100 tonnes as opposed to 38,000 a year ago.

– US Supreme Court mulls Trump tariffs… Canadian businesses are watching developments in Washington closely, as the US Supreme Court considers arguments on the legality of US President Donald Trump s trade tariffs. The court will have to decide if the president overstepped his authority by declaring a national emergency to unilaterally impose tariffs on 90 countries, including the one it shares its northern border with. The Court is a six to three majority of Republican-appointed judges, yet in last week s oral arguments, several conservative-leaning judges, including those appointed by Trump seemed skeptical. The court is expected to move swiftly on the issue, which could mean weeks or by the end of the year.

– China soybean imports hit record October high on strong South American supply… China’s soybean imports reached a record level for the month of October, a Reuters calculation of customs data showed on Friday, as buyers ramped up purchases from South America, while Beijing and Washington were mired in a trade war. The world’s top soybean buyer brought in 9.48 MMT in October, the General Administration of Customs said, up 17.2% from 8.09 MMT a year earlier. China’s soybean imports have set records from May through October of this year. In the first 10 months of the year, China’s soybean imports rose 6.4% from a year earlier to 95.68 MMT, the customs data showed.

“October typically marks the start of the US soybean harvest, but due to the earlier suspension of China-US soybean trade, shipments of new crop US beans were almost nonexistent,” said Liu Jinlu, an agricultural researcher at Guoyuan Futures.

Beijing initiated modest purchases of American farm products after the leaders of China and the US met just more than a week ago. But traders were still awaiting significant purchases of US soybeans after the White House said Beijing pledged to buy 12 MMT by the end of the year. But Beijing has said little of making such a commitment. Traders and analysts said China’s decision to maintain a 13% tariff on soybeans made US shipments too expensive for commercial buyers, when compared with Brazilian cargoes.

Recently, Chinese importers bought 20 cargoes of cheaper Brazilian soybeans as South American prices eased on expectations that US sales would resume, while COFCO took only three US cargoes ahead of the US-China leaders’ meeting.

– Lentil opportunities in Europe… Pulse Canada is hoping to expand lentil demand in Europe. The European Union and the United Kingdom import about 400,000 tonnes of the crop per year with Canada supplying about 100,000 to 140,000 tonnes on any given year. That makes Europe Canada s fourth largest customer behind India, Turkey and the United Arab Emirates.

We see opportunity for increased exports to that market as demand for lentils grows, said Julianne Curran, vice president of market innovation with Pulse Canada. And that is trending in the right direction. Consumers in Europe are very familiar with lentils and have a strong, positive perception of the crop. It is a market that consumes both red and green lentils. A 2024 study commissioned by Pulse Canada found that 30% of consumers in the United Kingdom and Germany eat lentils weekly, and more than half view them as healthy and nutritious. UK familiarity is also on the rise due to the influence of its large Indian population, who regularly consume lentils in dahls and curries.

Pulse Canada has been conducting technical training with food service operators in Germany and the Netherlands. The focus has been on universities, health care facilities and corporate dining.

– Expana sees EU 2026-27 rapeseed plantings rising… Rapeseed crops are developing well in the main producing countries of the European Union, Expana said, estimating the area sown in the bloc at 15.96 million acres in 2026-27, up 7% on the current season and 11% higher than the five-year average. Favourable weather boosted the sowing of winter grains in the EU this year with early-sown rapeseed seen gaining area due to better margins than for cereals, whose prices have declined sharply this season, Reuters reported.

Rapeseed is the largest oilseed crop in the EU. The leading producers are France, Germany and Poland. For the current season, Expana kept its rapeseed harvest estimate at 20.4 MMT, 20.9% higher than last season s rain-hit crop.

Sunflower and soybean plantings, which take place in the spring, are also expected to rise ahead of next year s harvest. Expana forecasts the sunflower seed area for 2026-27 at 11.58 million acres, a rise of 1% compared to 2025-26, while soybean plantings are projected to increase by 5% to 2.89 million acres.

– Bunge sells assets per merger approval… Bunge has sold five Western Canadian elevators as required under the federal approval for its merger with Viterra. All five have been sold to local companies. Direct Grain Ltd. will operate Dixon, Sask., Linear Grain Inc. bought Fannystelle, Man., and BP & Sons Grain and Storage Inc. purchased elevators in Manitoba at Beausejour, Tucker and Coulter. A sixth sale, of the facility in Valparaiso, Sask., is still waiting for approval from the federal transport minister. Bunge said it expects that sale to close shortly.

– US farm inputs could boost fertilizer prices… With fertilizer prices remaining elevated, StoneX fertilizer expert Josh Linville says there s little relief in sight. Despite speculation USDA and the US White House could issue additional tariff aid payments to American farmers to offset ongoing trade and input challenges, Linville says that cash could actually trigger another round of price inflation.

USDA is preparing to roll out $12 billion in trade aid to US farmers once the American government reopens. Linville says the potential for new government aid has some unintended consequences for the fertilizer market. Unfortunately, no, Linville says when asked if fertilizer prices might ease if aid payments don t go out. If the payments come out, I m afraid it s gonna boost fertilizer prices. It doesn t change the supply and demand for most of these products, but it does change the timing, and timing is everything.

Linville says the fertilizer market is as much about when farmers buy as it is about how much they buy. Injecting fresh cash into the market at once could cause a surge in demand that suppliers can t absorb smoothly…and that inflationary influence on fertilizer could spill across the border into the Canadian fertilizer market.

If there s a big fat check that goes into the (US) farmer s pockets and that gets spent on fertilizer, and you pull all that demand into one period, fertilizer is going to see its prices boosted as a result, he adds. We saw that the last time the (US) checks went out.

If not, I think we fall back to the global S&D…the production problems and supply problems…and prices probably hold tight, he says. We re hearing from our people in the fields…demand is better than we expected. I don t think we see anything short term that causes prices to go down. I m more afraid of the upside.

– Canada s job market surprisingly expands in October… Canada s employment picture continues to look better than expected. The Canadian economy added 66,600 jobs in October, marking a second consecutive month of surprise employment gains. The employment increase helped bring down the jobless rate to 6.9%. Job gains were driven by part-time work. The employment increase was focused on Ontario, led by wholesale and retail trade, transportation and warehousing, information, culture and recreation as well as utilities. Despite pressures from US tariffs, Canada has added a net 164,500 jobs so far this year.

Outside Markets

The Dow Jones Industrial Average rose 74.80 points on Friday to settle at 46,987.10, while the S&P 500 ticked up 8.48 points to 6,728.80. Early Monday, the December Dow Jones Futures are up 173 points.

Global stock markets are higher this morning following signs of progress in Washington to end a record government shutdown that has stalled economic data releases and intensified concerns over the state of the US economy. The US Senate last night moved forward on a measure aimed at reopening the federal government and ending a now 40-day shutdown that has sidelined federal workers and snarled air travel. But the process to end the shutdown may yet take some time. Still…optimism buoyed Wall Street stock index futures. Canada s TSX futures followed sentiment higher as commodity prices climbed.

A possible end to the longest running US shutdown is a positive for markets. Our expectation is that the next step is for a House vote on Wednesday, with the government set to re-open this Friday, said Prashant Newnaha, senior Asia-Pacific rates strategist at TD Securities.

The December US Dollar Index is down 0.036 at 99.435. The Canadian dollar strengthened against its US counterpart…currently quoted at 71.44 US cents.

Dec crude oil futures are up $0.37 at US $60.12/barrel. Oil prices rose on optimism that a possible end to the US government shutdown could soon lift demand in the world s top oil consumer, offsetting concerns about rising supplies globally. US lawmakers first step in ending the shutdown helped the return of risk appetite to markets.

Grain Markets

Chicago soybean futures are trading 2 to 7 cents/bu higher this morning, led by the front month contracts. Bean futures posted some strength to close out last week, as contracts were up 8 to 10 cents. But the nearby Jan contract gained only 1.75 cents on the week ended Friday…a week that saw several double digit up/down swings. Soymeal futures are narrowly mixed this morning after rising $1 to $4 higher on Friday in the front months…Dec meal was down $4.50 on the week. Soyoil futures are up 17 to 23 points this morning, adding to Friday s 30 to 44 point gains, with the Dec contract bouncing a whole penny higher last week.

While China had agreed at an end of October meeting between presidents Trump and Xi to buy 12 MMT of US soybeans by the end of the year and 25 MMT for each of the following three years, we have not seen that in writing from China and to date only minor soy purchases by China have been reported.

Soybean, along with soymeal futures, have rallied sharply from mid-October, but both markets have become overbought technically. Although the Trump-Xi agreement was certainly a positive development for the soy market, I think traders will soon need to see some concrete proof that China will book those commitments by the end of December. Time is running thin to get 12 MMT loaded and shipped by year-end.

Complicating the issue is the fact that China left a 13% import tariff on US beans at a time when Brazilian soy values have declined and Brazil is more price competitive into China. Rumors had China picking up another 20 cargoes of Brazilian beans in the past week. This year, so far, China had bought zero new-crop US beans until COFCO picked up a reported three cargoes last week from the US (180,000 tonnes) as a good will gesture. Brazil beans on a delivered basis are said to be discounted in price vs US soybeans for nearby and that spread widens even more into February-April.

I remain quite skeptical that Beijing will meet the 12 MMT short-term and 25 MMT annual US purchase targets.

Chicago corn futures are trading fractionally to 2 cents higher this morning. The corn market posted losses of 1 to 2 cents across most contracts on Friday, with the nearby Dec contract losing 4.25 cents last week.

Friday’s USDA production and supply/demand report (Nov 14) represents the main focus in trading discussions this week. Expectations include a lower US national yield average estimate, but still high overall US output forecasts.

Traders will also monitor demand news. Later today, the USDA will release its weekly US export inspection report. Additionally, US ethanol production reached a record last week. On Friday, the Environmental Protection Agency approved 14 requests from small refineries for full or partial exemptions under the Renewable Fuel Standard. Earlier this year, the EPA approved 140 petitions, either partially or fully, while denying 28. Friday’s announcement effectively clears most of the backlog. Biofuel stakeholders will now watch to see if these exempted gallons are reallocated to larger refineries.

US wheat markets are higher this morning…winter wheat futures are 5 to 8 cents higher, while Minnie spring wheat futures are up 5 cents on the nearby Dec/Mar contracts. The US wheat complex was mixed on Friday, with the winter wheat contracts closing lower, while spring wheat futures were steady to up a penny in the nearby contracts, and closed the week with a nickel gain on China s recent purchase of US hard red spring wheat.

CANADIAN GRAIN MARKET

ICE Futures canola futures finished stronger on Friday, as chart-based positioning ahead of the weekend provided support. The benchmark January canola contract was back above its 20- and 50-day moving averages, which underpinned values from a chart standpoint.

Gains in Chicago soybeans and soyoil provided spillover support, with European rapeseed also higher on the day. However, Malaysian palm oil finished the week near its lowest levels in four months.

Weekly Canadian canola exports of 188,400 tonnes were up 21% from the previous week, according to the latest Canadian Grain Commission data. However, crop year-to-date exports (Week 13) of only 1.4 MMT were roughly half of what moved by the same point the previous marketing year as China remains absent from the market.

January canola futures rose $6.30 on Friday to close at $640.00/tonne, while Mar canola gained $7.10 to $651.80.

For today… canola futures are trading between $2 and $3/tonne lower so far this morning…ignoring modest strength in CBOT soyoil and soybeans in early trade with little news to go on. Nearby Jan futures are $2.50 lower at $637.50/tonne. Canola futures were supported last week by the upward move in soybeans, with the benchmark Jan contract trading up $3/tonne for the week ended Friday.

In related outside markets…again CBOT soy complex is slightly higher, but EU rapeseed futures are slightly low, as are Malaysian palm oil futures (though stabilizing after the October sell-off).

Export volumes continues to disappoint, and US biofuel policy delays limits bullish sentiment. The US EPA announced new small refinery exemptions (SREs) last week, but deferred major US biofuel reallocation decisions until spring 2026, frustrating renewable fuel markets.

Our canola market is hanging on…boosted by soybeans but weighed down by sluggish exports and unclear biofuel policy.

On the feed grains… Prices for feed grain are grinding higher says Evan Peterson, trader with JGL Commodities in Saskatoon. They re not going to go soaring higher, Peterson added. He said more cattle are going into the feedlots, leading to an upswing in demand for feed grains. We re starting to see a little more demand creeping into southern Alberta, Peterson said.

Lethbridge is home to a number of feedlots and the city is also known as feedlot alley. Feed barley has increased from $250 to $255/tonne delivered Lethbridge to now $260 with prices trying to push higher a little bit more.

Another factor in the recent upticks have been the farmers. Farmers sold pretty heavy off of the combine. That created some decent cash flow and now they re sitting back waiting for the next little bump up in the market, Peterson explained, adding increased export sales and the potential for more has also pushed up Prairie feed prices.

Prairie Ag Hotwire reported for the week ended Nov. 5, that feed barley prices were steady to lower. They held firm in Saskatchewan at $4.46 to $4.75/bu delivered. But in Manitoba they dipped six cents at $4 to C$4.30/bu delivered and shed four cents in Alberta at $4.35 to $5.66.

Over the course of the last 30 days, feed prices have been steady to higher.

To access the latest futures prices, go to https://www.producer.com/markets-futures-prices/

Source: producer.com