AM Market Report – November 18, 2025

ICE canola futures are narrowly mixed to slightly higher this morning…still trending up from the October low and around its highest levels since late August. Chicago soybeans were up overnight, but gains have since faded to small declines in the past hour…Jan contract still up a quarter of penny, but deferreds are now 1 to 3 cents/bu lower after Monday s rally surge higher.

CBOT corn futures are starting the day trading 1 to 2 cents higher. Monday’s weekly export inspection confirmed strong demand in the corn market.

US wheat markets are opening mostly steady to 2 cents higher, though some wavering in the spring wheat market. Wheat prices reflected Monday’s bullish US export inspections data, which are now 19% ahead of last year.

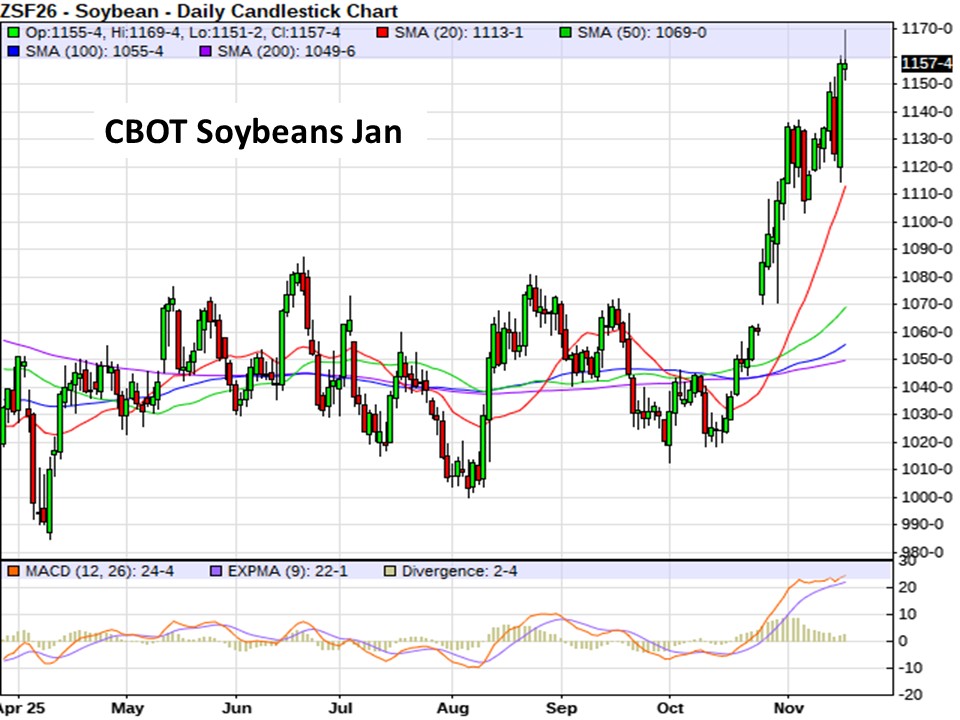

On Monday, soybeans led the rally, reaching their highest level since July 2024. The sharp move higher was backed by news that China purchased multiple cargoes of US soybeans. Record monthly US soybean crush for October also supported buying strength.

After last Friday s beat-down, US grain market bulls could not have asked for a better trading day on Monday. Monday s bullish price action suggests the grain futures markets have good underlying strength and that bulls are confident to step in and buy the dips. Corn, soybean and soymeal futures markets are enjoying near-term price uptrends, with soyoil starting to join in, while wheat bulls are working on restarting their near-term price uptrends.

But after Friday’s generally bearish-leaning USDA report, this week’s rally just might turn out to only be temporary. But for now…the market trades based on current information. And if the demand news continues, it could attract traders’ attention daily. If not, they fall back.

In Other News

– Carney government wins crucial confidence vote on budget... Prime Minister Mark Carney’s minority Liberal government budget passed a third and crucial confidence vote on Monday evening thanks to the support of the Green Party and multiple abstentions, averting the possibility of a federal election at the end of this year.

* MPs voted to approve the Liberal government s budget.

* Budget motion passed 170 to 168.

* Two NDP MPs and two Conservative MPs abstained from voting.

* Green Party Leader Elizabeth May voted yes. May announced her decision after Carney committed to meeting Paris climate targets during question period.

* Budget votes are treated like confidence votes, so the government needed a win to avoid another election.

* Carney’s first budget calls for billions of dollars in new spending to help the economy in the face of the trade war, along with cuts to the public service the government says would save billions of dollars.

– China buys US soybeans… China bought at least 14 cargoes of US soybeans (840,000 tonnes) on Monday for shipment in December and January, traders with knowledge of the deals said, its largest purchase since at least January and the most significant since a summit between US President Donald Trump and China s President Xi Jinping in October. China’s state-owned grain trader COFCO is buying US soybeans to meet the pledges it made to Washington at the trade summit in Busan, South Korea, even though the cargoes are priced much higher than rival Brazilian offers. The sales total may ultimately be larger if more deals are finalized, traders say.

(FLASH…USDA just reported as I write China officially bought 792,000 tonnes of US beans yesterday…~13 cargoes…good but not quite as big as initial trade rumors)

The White House said China had agreed to buy 12 MMT of US soybeans by end of this year, followed by 25 MMT annually over the next three years. But only a small volume of sales had occurred this fall season before Monday. And these targets would still be 14% below the five-year average of 29 MMT between 2020 and 2024, and slightly below the 10-year average of 27 MMT. China previously absorbed about 60% of US soybean exports in the years before

Trump took office and started his trade wars.

Chicago soybean futures rallied nearly 3% on Monday to a 17-month high on the China trade news.

– US October soybean crush record high… The US soybean crush topped all trade forecasts and hit a record high in October, according to a monthly National Oilseed Processors Association (NOPA) report released on Monday. NOPA members, which account for around 99% of all soybeans processed in the United States, crushed 227.647 million bu of the oilseed last month, up 15.1% from the 197.863 million bu crushed in September and up 13.9% from the October 2024 crush of 199.943 million bu. It also eclipsed the previous all-time monthly US soy crush record of 206.604 million bu set in December 2024.

US crush capacity has swelled in recent years as processors built new plants and expanded existing ones to meet rising vegetable oil demand from biofuels makers. Many plants that had been idled for seasonal maintenance ahead of the US harvest this year resumed operations by October in time to receive a flood of newly harvested soybeans.

US soyoil stocks among NOPA members as of October 31 rose to 1.305 billion pounds, up 5.0% from a nine-month low of 1.243 billion pounds at the end of September and up 21.5% from the 1.074 billion pounds in stocks a year earlier.

– Canada needs strong global lentil demand in 2025-26… One of Canada s top lentil customers had an extremely disappointing crop this year. Farmers in Turkey harvested 230,000 tonnes of red lentils, a 43% drop from the previous year, according to the Turkish Statistical Institute. It is the third lowest red lentil crop on record. Growers produced another 29,700 tonnes of greens, a 58% decline from the previous year. The hope is that Turkey s poor crop will stimulate import demand in Canada s second largest market behind India.

We do need good news, especially with what looks to be a pretty good Australian crop coming, said Western Producer markets desk analyst Bruce Burnett. The smallish Turkish crop helps.

Turkey purchased 406,738 tonnes of lentils through the first nine months of 2025. Kazakhstan was the leading supplier, accounting for 42% of those imports. Canada took second spot, supplying 36% of the country s needs during that timeframe.

Canada needs all the demand it can muster because farmers in this country produced an estimated 2.97 MMT of lentils in 2025…22% higher than last year and the second biggest crop on record. But production is also up in all the other major exporting regions, including Kazakhstan, Russia and Australia.

Canada s total exports are forecast at 2.1 MMT, up from 1.84 MMT in 2024-25. Year-end carryout is estimated at a burdensome 1.15 MMT, resulting in a heavy 45% stocks-to-use ratio.

Outside Markets

The Dow Jones Industrial Average plummeted 557.24 points lower to settle Monday at 46,590.24, while the S&P 500 ended down 61.70 points at 6,672.41. Early Tuesday, the December Dow Jones Futures are down another 392 points.

Global stock markets continue falling in a broad risk-off mood, sparked by worries about an overvalued tech sector and diminishing prospects of an imminent interest rate cut from the US Federal Reserve. The decline comes as investors brace for quarterly results from retailers as well as chip giant Nvidia tomorrow, and awaited a long-delayed US jobs report this week.

It s starting to feel like investor conviction at current levels is fading, said Tareck Horchani, head of prime brokerage dealing at Maybank Securities in Singapore. It s less about a sharp catalyst and more about positioning fatigue, valuation sensitivity and a growing sense that the rally needs a pause.

?

The artificial intelligence trade has started to wobble as investors worry the amount of borrowing needed to fund its buildout will become a burden. Just Monday, Amazon.com Inc. tapped the credit market for $15 billion in a bond sale. The US economy is showing signs of slowing, particularly in the labor market, and low-end consumers appear increasingly under pressure. With technical indicators also flashing warnings…both the S&P 500 and Nasdaq 100 closed below their 50-day moving average price…Wall Street strategists are questioning whether a year-end rally is in the cards, Bloomberg reported overnight. The rest of the week is shaping up as critical for any run back toward all-time highs. Consumer giants like Walmart Inc., Home Depot Inc. and Target Corp. will deliver results and commentary on the looming holiday shopping period. Nvidia Corp. is the last of the big seven to give its business update. And US government economic data, absent for the past seven weeks, will begin trickling out.

The December US Dollar Index is down 0.103 at 99.385. The Canadian dollar strengthened against its US counterpart…currently quoted at 71.26 US cents.

Dec crude oil futures are down $0.15 at US $59.76/barrel. Oil prices are steady to slightly weaker as supply concerns eased with the resumption of loadings at a Russian export hub, which was briefly halted by a Ukrainian drone and missile strike, as traders continued to assess the impact of Western sanctions on Russian flows.

Market worries centre around the build-up of oil on tankers as buyers assess the risk of potentially breaching sanctions, said Vivek Dhar, mining and energy commodities strategist at Commonwealth Bank of Australia, but added that history has shown Russia s ability to adapt to sanctions. We expect any disruption from U.S. sanctions will prove temporary as Russia finds ways to circumvent sanctions once again.

Grain Markets

Chicago soybeans were up overnight, but gains have since faded to small declines in the past hour…Jan contract still up a quarter of penny, but deferreds are now 1 to 3 cents/bu lower. Bean futures were in rally mode on Monday, with nearby contracts up 23 to 32.75 cents. Jan bean futures are up a quarter cent early Tuesday at $11.57/bu in steep rally mode over the past month. Rally seems extended.

Soymeal futures are $2 to $3/ton weaker this morning after rallying $2 to $6/ton on Monday. Soyoil futures are up another 53 to 71 points this morning after finishing Monday with 60 to 99 point gains.

Wire reports indicate at least 14 cargoes (~840,000 tonnes) of US soybeans were purchased by China on Monday, with some pushing that number towards 20 cargoes (1.2 MMT). But USDA just reported the real number at 792,000 tonnes. Worth noting…pledge to buy US beans or not, Brazil remains easily the lowest priced beans on the market right now.

Monday s weekly US export inspections report showed a total of 1.176 MMT of US soybeans shipped in the week ended Nov 13. The marketing year total is now 10.109 MMT of US beans shipped as of Sept 1, but that is 42.5% below the same period last year. USDA is estimating US soybean exports to total 1.635 billion bu in 2025-26, down 13% from the previous year.

NOPA data released yesterday showed a total of 227.65 million bu of soybeans crushed in the US in October, exceeding the trade range of estimates…and an all-time record for any month.

Brazil s soybean crop is estimated to hit a new all-time record at 177.7 MMT according to Abiove.

Traders have one eye on US exports and one on South America’s crop growing weather.

Chicago corn futures are up 1 to 2 cents this morning. The corn market saw 3 to 4 cent gains into Monday s close. March corn is flirting with $4.50/bu.

Weekly export inspections data showed 2.054 MMT of US corn shipped in the week that ended on Nov 13, the largest total for any week since April 2021. That was an increase of 38.35% from the week prior and more than double the same week last year. US marketing year shipments have totaled a massive 15.838 MMT already since Sept 1, a 73% increase yr/yr. USDA is currently estimating US corn exports to total 9% above the previous year.

US wheat markets are steady to edging cents higher…winter wheats steady to 2 cents higher, while Minnie spring wheat futures are more narrowly mixed though up 1 to 2 cents on the nearby Dec/Mar contracts. The US wheat complex posted a rally across the three US markets on Monday…spring wheat futures were 5 to 9 cents in the green at yesterday s close.

USDA tallied US wheat export shipments at 246,533 tonnes during the week ended Nov 13. That was 15.41% below the week prior, but up 25.06% from the same week last year. Marketing year exports for 2025/26 are now 12.363 MMT since June 1, which is now 19.3% above the same period last year.

The trade is also monitoring early harvest activity amid big wheat crop expectations in Argentina and Australia, along with winter wheat development weather in the US, Europe, Russia, and Ukraine.

There was some concern on news Russia shipped 58,000 tonnes of wheat to Mexico over the past month. A concern for US and Canadian exporters which are the primary wheat exporters to Mexico. These exports were shipped from the port of Kaliningrad in the Baltic Sea.

CANADIAN GRAIN MARKET

ICE canola futures closed higher on Monday, boosted by the strong performance of the Chicago soy complex. China demand and strong October crush data sent the soy complex sharply higher, with the nearby January soybean contract jumping nearly 33 cents/bu on the day. Advances in European rapeseed and palm oil supported canola as well, although crude oil slipped lower.

Declines in the Canada dollar added to the upside in canola, while weaker 2025-26 export demand for Canadian canola compared to a year earlier remains a bearish influence.

January canola gained $7.70 yesterday to close at $655.20/tonne, and March was $8.10 higher at $666.70.

For today… canola futures are narrowly mixed to slightly higher. Jan canola is down a very modest $0.20 at $655.00/tonne…still trending up from the October low and around its highest level since late August. Note the convergence of the 100- and 200-day moving averages just above at around the $662 level.

CBOT soy complex continued to trend higher in the overnight session, which helped support our canola market. But the bean market in the past hour has started to revert back down to modest losses, which has tipped canola back slightly. Soyoil is holding up positive though…which remains supportive to canola.

Malaysian palm oil futures are higher, lifting off its consolidation zone…helped no doubt by the bounce in soyoil. EU rapeseed is steady to slightly weaker, though like our canola has trended generally higher in the past month of its October lows.

To access the latest futures prices, go to https://www.producer.com/markets-futures-prices/

Source: producer.com