AM Market Report – November 24, 2025

ICE canola futures are trading mostly $1 to $2/tonne lower to start this morning. The canola market dipped lower last week ended Friday (Nov 21), with the January contract down $6.40/tonne over the previous 5-session stretch.

Chicago soybean future are leaking 2 to 4 cents/bu lower this morning, with its by-products (meal/oil) also weaker. Bean traders saw speculative and farmer selling in response to recent price rallies…ending last week near unchanged.

The USDA confirmed 1.584 MMT in US soybean export sales to China last week despite US beans being more expensive than Brazil. Total sales may be closer to 2 MMT after a minimal volume was sold ahead of the end of Oct Trump-Xi summit with other recent purchases below the USDA’s daily reporting threshold. But China s purchases of US soybeans remain far off the 12 MMT that Trump officials said Beijing promised to buy by Dec 31.

China’s purchases of US soybeans offer psychological support, if nothing else. But bean futures on Friday faded last week’s confirmed China purchases and instead saw profit taking. What do the bulls need to retest the highs? More China business and/or clarity on the US-China deal?

CBOT corn futures are slipping fractionally to a penny lower this morning. After posting impressive gains early last week, Dec corn futures saw persistent selling pressure to close out the week, stalling out the recent uptrend dating back to the August low.

US wheat markets are also lower right now…spring wheat futures 1 to 2 cents lower, while the winter wheats are down mostly 3 to 5 cents. Wheat futures were mixed Friday but ended lower for the week. Wheat markets have made attempts recently to break through overhead resistance levels, but upside price potential faces ongoing bearish constraints…overhead chart resistance and a lack of buying interest due to the large global supplies.

The near-term technical postures for grain markets have deteriorated, which has emboldened chart-based speculators to start this US holiday-shortened trading week…US Thanksgiving holiday is Thursday (Nov 27).

In Other News

– Canada and China can reset their relations in Trump’s new trade world…Prime Minister Mark Carney was in South Africa this weekend for the G20 summit, a meeting that was tellingly boycotted by the world s largest economy. It’s the latest in a series of moves by US President Donald Trump indicating the world order is rapidly shifting.

But as Canada starts to diversify its ties with other countries amidst an increasingly unpredictable and unreliable relationship with the US, its pivot toward China, in particular, will need to be strategic…the work must be done while balancing the risks and strengthening the country internally.

Some analysts say a first step in diversifying and increasing trade with China is ending the trade war between the two countries. That would include Canada removing its 100% tariff on Chinese electric vehicles…and look for possible partnerships in electric vehicle battery production and electric vehicles…something the federal government is now reviewing. Currently, China has levied counter-tariffs on Canadian canola, seafood and pork. The Canada China Business Council (CCBC) estimates the impact to be in the billions.

– Carney views India as a reliable trading partner… The prime ministers of Canada and India have agreed to launch negotiations towards a new Comprehensive Economic Partnership Agreement (CEPA). On Sunday, Prime Minister Mark Carney and Indian President Narendra Modi met on the sidelines of the G20 summit. The two countries…who are in the midst of a reset of a strained relationship…are now beginning talks about boosting cooperation, an official said, and a readout is expected. This development came just hours after Carney made it clear, that yes, he does consider India to be a reliable trading partner. Carney went on to add that, not dissimilar from other nations, issues can arise, but there are mechanisms and systems in place to adjudicate.

We can be both a reliable trading partner, and there will be some sources of friction. What I will say, with respect to India is that we don t have a Comprehensive Economic Partnership Agreement with India, one of the world s largest and fastest growing economies, Carney said. The ability to have more effective trade with them, to scale that trade with them, would be greatly helped by that.

After years of tension, Carney has sought to reset relations with India amid US trade uncertainty. Sunday s sit-down between the two leaders was their second one-on-one in the last six months.

Modi and Carney last had a bilateral at the G7 summit in Kanansaskis, Alta. in June. Both leaders also met on the sidelines of the G20 summit in South Africa on Saturday, along with Australian Prime Minister Anthony Albanese to announce a new trilateral partnership in technology and innovation.

– Canada joins world leaders saying Trump s plan to end war in Ukraine needs work… Prime Minister Mark Carney, along with more than a dozen world leaders meeting in South Africa, issued a joint statement on Saturday saying US President Donald Trump’s plan to end the war in Ukraine “will require additional work”…in other words, it s not good enough.

The leaders met on the edges of the G20 summit in Johannesburg to talk about Ukraine after President Volodymyr Zelenskyy warned that his country is facing one of the most difficult moments in its history.” Zelenskyy is facing a deadline imposed by Trump to take or leave his plan to end the war…that’s clearly viewed as favouring Russia…by Nov. 27.

“We are clear on the principle that borders must not be changed by force,” the leaders’ joint statement said. “We are also concerned by the proposed limitations on Ukraine’s armed forces, which would leave Ukraine vulnerable to future attack.”

Ukrainians were not even invited to the negotiations for their future. If Ukraine doesn t accept, the Trump is threatening to cut off US intelligence sharing and weapons supplies. And a meeting ahead of the deal between Trump admin representatives and a Russian envoy under US sanctions is raising alarm among American officials and lawmakers.

Trump s 28-point plan is essentially a call for Ukraine to surrender…Kyiv is to cede territory, accept limits on the size of its military with only vague security guarantees, renounce ambitions to join NATO, and lift sanctions on Moscow over time…all long-standing Kremlin demands. The plan also contains some proposals Russia may dislike, including pulling back its military from some areas it’s captured in Ukraine, buty hardly a big ask.

Canada, the European Council and the European Commission, the UK, France, Germany, Italy, Japan, Finland, Spain, Norway, the Netherlands and Ireland were all at the meeting.

– Bumper harvests boost global grain stocks… With better-than-expected harvests taking place in many parts of the world, the International Grains Council (IGC) forecast record grain production in the 2025-26 season. The IGC s latest Grain Market Report projected output for total grains (wheat and coarse grains) to increase by 5% over the previous year, with year-on-year increases for all grains. The larger global harvest will more than compensate for the tightest opening stocks in 10 seasons, boosting overall supply by 3%, to an all-time peak (2.43 billion tonnes), the IGC said.

The increase will be needed as the Council sees total grains consumption rising by 2% in 2025-26, to a new high of 2.4 billion tonnes due to higher food, feed and industrial uses.

World wheat production was revised higher by 3 MMT over the previous month s forecast to 830 MMT. If realized, it would be an increase of 31 MMT (4%) over the 2024-25 total.

While the forecast for global corn production increased only slightly (1 MMT) month on month, a 5% year-on-year increase to a record 1.298 billion tonnes is anticipated by the IGC.

Conversely, global soybean output was revised lower by 2 MMT. Production is seen dropping by 3 MMT year on year to 426 million tonnes. However, the IGC noted that the projected figure is well ahead of the recent average, including a potentially record outturn in Brazil.

With soy consumption seen at a new peak (431 MMT), on gains in Asia and the Americas in particular, inventories could tighten by around 5 MMT year on year, the IGC said.

– Europe’s barley prices climb as buyers chase supply… Prices for animal-feed barley in Europe are matching or surpassing milling wheat, an unusual trend driven by strong export demand and tight supply, traders said. Feed barley, which represents most of the market for barley, typically trades at a steep discount to bread wheat. Its overall price is lower than last year, against the background of a heavily supplied grain sector. But its relative strength against wheat has brought higher-than-expected costs for buyers, particularly in North Africa and the Middle East.

Despite a larger EU harvest this year, availability of barley has shrunk due to brisk French shipments to China, slow farmer selling elsewhere, and Turkey’s switch from exporter to importer after a poor crop. Barley is currently like gold, a German trader said.

Traders said west EU and Baltic feed barley prices were around the same as wheat at between US $221-$226/tonne FOB for December loading. Black Sea barley prices were higher with Russian and Ukrainian at around $227-$229/tonne FOB.

France has already shipped half its projected non-EU barley exports for 2025/26, including nearly 900,000 tonnes to China, and is still loading for Saudi Arabia. With French farmers largely sold out, export premiums have risen above wheat. Black Sea supplies are also dwindling, leaving Germany to fill gaps, though reluctant farmer selling is maintaining supply tension.

However, while barley is rarely priced premium to wheat, absolute price levels remain below last year amid ample global grain supply. In addition, some say large crops in Argentina and Australia could soon dampen the market and prevent price increases going forward.

– Trump cuts US tariffs on Brazil… US President Donald Trump signed an order removing the 40% tariffs he had placed on Brazilian beef, coffee, cocoa and several fruits, reversing the punitive duties imposed in July over Brazil s handling of the Bolsonaro prosecution. The rollback, retroactive to November 13, is aimed partly at easing food-price pressure in the US and restoring smoother US Brazil trade flows. The move opens the door for increased Brazilian shipments of coffee and beef…key imports for US consumers…while annoying US beef producers by heightening competitive price pressures. It also underscores how quickly Trump s erratic trade policy can shift, with political actions abroad creating rapid swings in tariff treatment and market conditions.

– Tyson Foods to close major US beef plant as cattle supplies dwindle...Tyson Foods will close a major beef plant in Lexington, Nebraska, with about 3,200 employees in January after US cattle supplies dropped to their lowest level in nearly 75 years. The closure in the heart of cattle-feeding country signaled supplies will remain tight, forcing meatpackers to pay steep prices for cattle to process into steaks and hamburgers. Beef prices have set records due to low supplies and strong demand, raising costs for consumers.

President Donald Trump said last month that he was working to bring down prices. Tyson said it will also reduce operations at a beef plant in Amarillo, Texas, to a single, full-capacity shift, affecting about 1,700 workers.

Outside Markets

The Dow Jones Industrial Average rallied 493.15 points higher on Friday to settle at 46,245.41, while the S&P 500 gained 64.23 points to 6,602.99. Early Monday, the December Dow Jones Futures are up another 109 points.

Global stock markets are trending mostly higher this morning ahead of an event-filled week, as investors eyed growing expectations of a US Federal Reserve interest rate cut in December even as policymakers remain divided over such a move. Wall Street futures were mixed overnight, but are turning higher now this morning. Canada s TSX stock index futures have inched lower but recovering after major North American markets closed up Friday.

The December US Dollar Index is down 0.003 at 100.110. The Canadian dollar weakened against its US counterpart…currently quoted at 70.94 US cents.

Jan crude oil futures are down $0.04 at US $58.02/barrel. Oil prices have ticked slightly lower this morning following last week s notable 3% decline, as investors weighed the chances for a US rate cut against the prospect of a Russia-Ukraine deal that could free up more Russian supply through an easing of sanctions.

The sell-off (last week) was triggered mainly by President Trump s forceful push for a Russia-Ukraine peace deal, which markets see as a fast track to unlocking substantial Russian supply, IG analyst Tony Sycamore wrote in a note.

Grain Markets

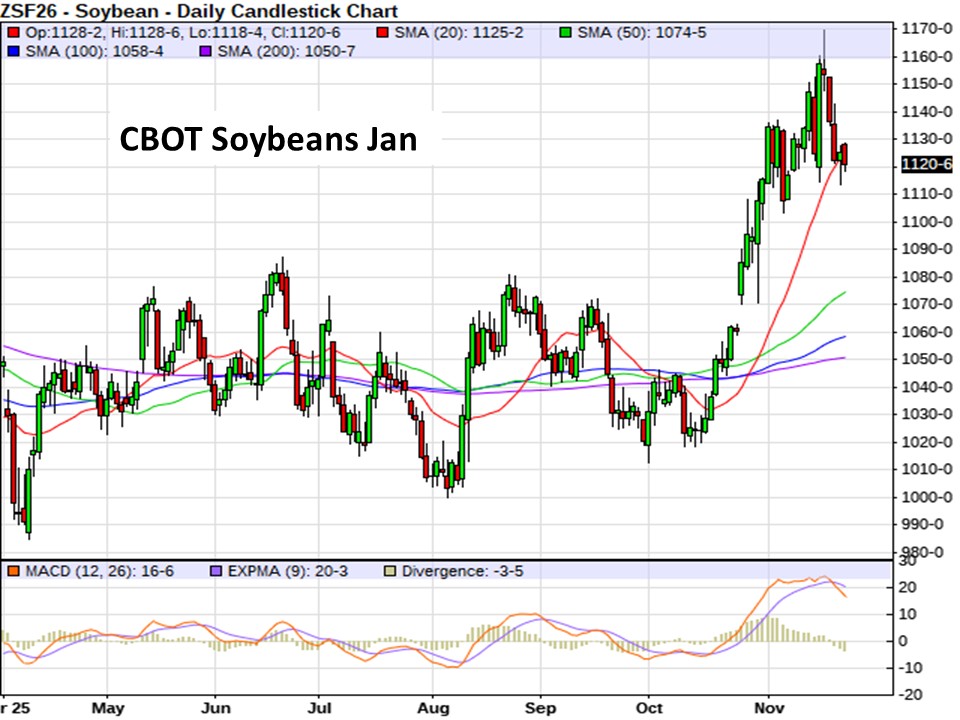

Chicago soybean futures are trading 2 to 4 cents/bu lower to start this morning. Bean futures closed mixed on Friday, with the nearby contracts up 1 to 2 cents. Jan beans managed to post a miniscule half cent gain on last week…closing 44 cents off last week s high.

Soymeal futures are down $1/ton this morning after rising $1 to $2/ton on Friday, though Dec meal dropped $7.40 on the week.

Soyoil futures are 39 to 43 points lower this morning, losing 33 to 40 points on Friday, with Dec bean oil posting a modest 11 point gain week-to week. Soyoil trade remains troubled on chatter the White House may delay removing incentives on imported used cooking oil…and persistent delays in advancing US biofuel policy.

In a CNBC interview this morning, US Ag Secretary Rollins indicated the US and China would be inking a deal this week or next week in terms of the 12 MMT soybean commitments that have been previously reported. I ll believe it when I see it.

The past month has seen a sharp rally in the soybean market…a rally that has since stalled…or at least paused. Jan bean futures are down 4.5 cents this morning at $11.20/bu, down 37 cents from its Nov 17 closing high and now tipping just below its 20-day moving average ($11.25).

Traders want to see China’s buying efforts of US beans getting to reportedly agreed-upon levels by the end of the year. But with Brazilian soybeans between US $30-40/tonne cheaper than US soybeans, one has to wonder how long China will purchase US beans. The large increase in Brazilian production is permanently changing the dynamics of the soybean trading relationship, and most US farmers don t seem to realize it.

Meanwhile, Brazil’s soybean planting and growing weather continues to be favorable. It is getting dry in southern Brazil, northern Argentina. However, rain is expected this week.

Chicago corn futures are down 1 to 2 cents this morning. The corn market ended weaker on Friday as contracts settled fractionally to a penny lower. Dec corn declined 4.75 cents last week as the contract s options expired on Friday. First notice day is this Friday. Dec corn futures failed in a tested up to its 200-day average at mid-month, and has since fell back below 20- and 50-day averages. The market has not yet violated trendline support drawn from the August low, but recent price action has been bearish leaning.

Traders will watch today’s weekly US export inspection report for signs of sustained demand for American corn. Backlogged weekly export sales reports will start trickling out from USDA, but will have less influence until they are current in January.

South America’s crop weather is now increasingly in focus. So far, conditions down south are mostly good (price bearish).

Corn traders will be positioning ahead of Thursday s US Thanksgiving holiday.

US wheat markets are weaker this morning… Minnie spring wheat futures are off 1 to 2 cents, while the winter wheats are losing 3 to 5 cents. The US wheat complex saw Friday s trade close with mixed action across the three markets, with spring wheat futures down 5 to 7 cents…through the Dec contract still snuck out a quarter cent gain of the week. Cash basis on both side of the Canada/US border continues to strengthen on solid export demand.

This week’s weather turns cold for North America. Arctic air will prevail to end the year, turning winter wheat dormant in a lot of areas. The possibility of heavy snow and blizzard conditions will put the chances for fieldwork behind a lot of farmers.

Heavy rain has delayed what s expected to be a record harvest in parts of Argentina. Wheat s also watching the early harvest in Australia, along with winter wheat conditions in Europe, Russia, and Ukraine. The USDA s attach in Australia has the 2025/26 wheat crop at 36 MMT, compared to the current official guess of 34.5 MMT and the 2024/25 total of 34.11 MMT, thanks to favorable weather, with exports also expected to be larger than the previous marketing year.

According to the Nov 14 USDA supply/demand report, major wheat exporter ending stocks increased by 6.375 MMT from the previous month estimate, which equates to 62.9 days of supply. This is the largest stocks to use level since the 2018-19 crop year. Increased stocks in the major exporters remains a bearish weight on wheat prices.

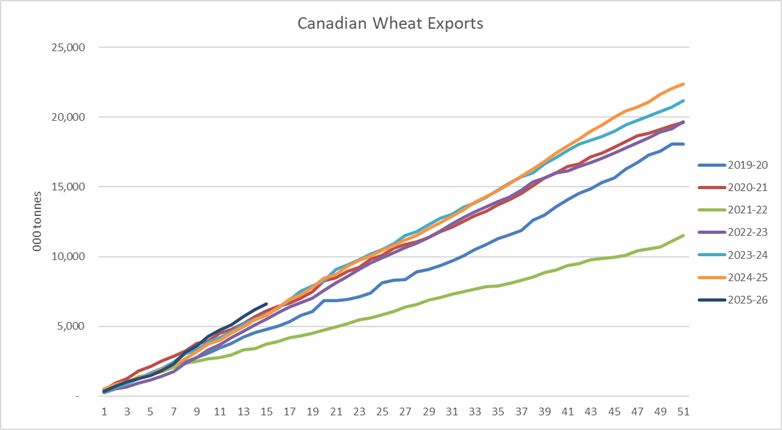

Wheat prices have been disappointing this year, but there have been positive signs in the cash markets in the Prairies. Cash prices in Western Canada are approaching the levels last year in mid-November. The reason for the strong prices has been record demand for Canadian wheat exports. Wheat exports to the end of Nov 16 (Week 15) was 6.601 MMT, which is 795,000 tonnes above the same time last year. The strong export demand should support prices in the face of the bearish fundamentals of the international wheat market.

Last week we saw Prairie cash bids for CWRS 13.5 wheat hit as high as $7.85+/bu for nearby delivery (western areas) and $8/bu bids for March onward.

CANADIAN GRAIN MARKET

Exports showed some weekly strengthening, but ICE canola futures still closed lower to end the week. Declines in Chicago soyoil, Malaysian palm oil, and European rapeseed all spilled over to pressure canola on Friday. Crude oil was also lower on the day.

January canola finished Friday $9.10 at $641.80/tonne, with March losing $9.30 at $654.30.

For today… canola futures are trading narrowly mixed this morning…less than $1/tonne either side of unchanged, but leaning slightly higher. Jan canola is up a very modest $0.60 at $641.70/tonne trying to hold trendline support drawn off its early October low. MACD and Stochastics chart indicators are weakening with last week s dip lower.

Softer CBOT soy complex and diesel markets are weighing…as is Malaysian palm oil futures which are pressing down into 4 month lows. EU rapeseed is also slightly weaker this morning.

Vegoil-relate markets continue to debate the inconsistent nature of the Trump s administration s policy for US biofuels. The EPA insists it is not backtracking on proposed record-high RFS blending volumes, but rumors continue swirling about possible delays. And Reuters last week reported the Trump admin may delay cuts to foreign feedstock incentives until 2027-28. This would be bearish soybeans/soyoil…but mildly supportive for canola/canola oil.

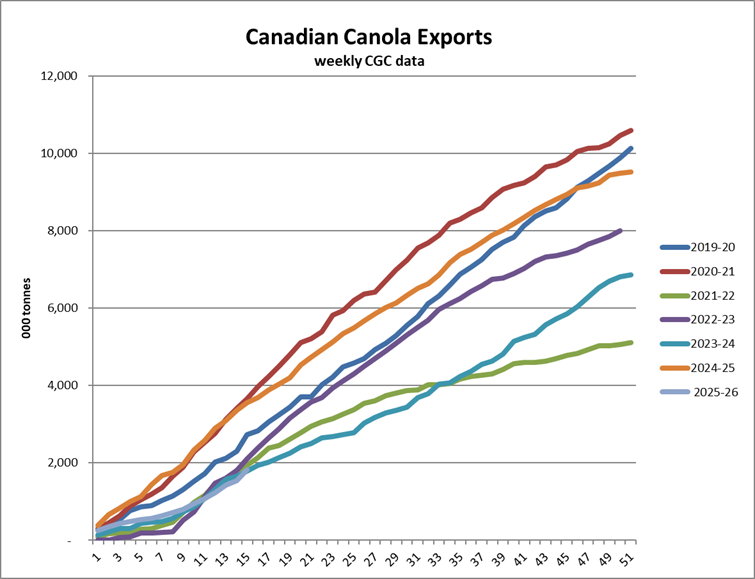

Strong canola crush use here domestically remains price supportive, but Canadian canola s export pace remains sluggish on lacking China demand. And then the canola remains caught in the crosswinds of soyoil, palm oil, and politics.

Interestingly…canola export shipments for the ended Nov 16 (Week 15) came in at the strongest of this new crop marketing year at 284,600 tonnes as report ed by the CGC. This brought the crop year to date total to 1.83 MMT, butt that s still well below the 3.564 MMT shipped by this same time last year. Canola exports to date this crop year are the second lowest of the past seven years.

To access the latest futures prices, go to https://www.producer.com/markets-futures-prices/

Source: producer.com