AM Market Report – March 12, 2026

GOOD MORNING…HERE IS YOUR MORNING MARKET NEWS

OVERNIGHT GRAIN TRADE

Grain markets are trending higher this morning. ICE canola futures are continuing to trend higher, posting early morning gains of $3/tonne and looking to establish an 8-month high. Chicago soybean futures are 3 to 15 cents/bu higher, led by its nearby contracts…pressing to establish a 2-year high.

CBOT corn futures are up 3 to 5 cents this morning…looking to post a 9-month high close today.

US wheat markets are also showing gains…5 to 7 cents higher for spring wheat futures and mostly 6 to 9 cent gains for the winter wheats.

Read Also

Prairie Weather

A low pressure system is tracking across the southern Prairies this morning. The heaviest snow/freezing rain is falling in southern…

More technically-based buying was featured overnight as the grain markets are in price uptrends and the bulls have momentum on their side.

The US/Israeli war with Iran is causing the largest oil supply disruption in history, according to the International Energy Agency…the key element driving commodity prices higher and financial markets lower. As crude oil goes, so go the row-crop markets. Broad-based commodities are feeding into the volatility frenzy.

In Other News

– Dire Strait of Hormuz standstill hardens oil supply shock… Global oil markets are suffering the largest supply disruption in history as the US/Israeli war with Iran drives production to the lowest level in four years, the International Energy Agency said in a report today. Gulf producers had cut oil production by at least 10 million barrels a day because the Strait of Hormuz is almost impassable to shipping, it said. The IEA expects world output to fall by 8 million b/d in March as a result. This represents a decline of more than 7% from the roughly 107 million b/d produced in February.

Big supply reductions have been seen in Iraq, Qatar, Kuwait, the UAE and Saudi Arabia, but declining production in the Gulf would be partly offset by increased output from Kazakhstan and Russia and by non-OPEC+ producers, said the IEA. Saudi Arabia and the UAE are rerouting some of their exports through ports outside the Gulf.

Crude oil markets are oscillating between paralysis in the Strait of Hormuz and the arrival of coordinated reserve releases, a tension that all but guarantees elevated price swings. Bloomberg vessel-tracking data show inbound traffic to the Persian Gulf effectively at zero in the past 24 hours, with outbound movements reduced to a handful of bulk carriers and Iranian-linked ships.

Just prior to the conflict, close to 100 vessels a day were transiting the waterway. Now, commercial flows through the channel are all but frozen. For oil, that collapse in ship counts is the only metric that matters.

Roughly 20 million barrels a day, about a fifth of global petroleum liquids consumption, and up to one-third of global trade in urea, typically moves through the narrow corridor between Oman and Iran. Both are of direct concern to farmers, with fertilizer and fuel accounting for more than 40% of a grain farmer s annual operating costs. Input prices have spiked, jarring the global economy and threatening to wipe out hopes of income gains with much higher costs.

When that transport artery is constricted, barrels accumulate inside the Gulf, refiners outside the region scramble for alternative supply and physical markets tighten abruptly. In effect, everything is trading as a derivative of oil as correlations have picked up considerably over the last 10 days. It ultimately comes down to the boats…no passage, no reprieve for markets.

That arithmetic explains the International Energy Agency s decision yesterday to deliver the largest coordinated emergency stock release in its history, a 400 million barrel drawdown aimed at cushioning the transit shock. Strategic reserves are designed to offset sudden supply interruptions, and a transit shock of this scale certainly qualifies. Yet even a release of that magnitude would only temporarily cushion the disruption. Until commercial shipping resumes at scale, the global backdrop…from crude to equities and FX…will remain at the mercy of the boats.

– Global diesel supply vulnerable… Diesel prices have led the way higher in the global energy complex due to squeeze on Asian refineries resulting from the virtual closure of the Strait of Hormuz. Reuters on Wednesday reported that traders and analysts are growing fearful that surging diesel prices will threaten to slow global economic activity. Energy economist Philip Verleger has estimated disruptions have resulted in a supply loss of around 3 to 4 million barrels of diesel a day, or around 5% to 12% of total global consumption, the report said.

“Diesel is the most exposed product to this conflict structurally,” Shohruh Zukhritdinov, founder of Dubai-based Nitrol Trading, told Reuters. “Diesel underpins freight, agriculture, mining and industrial activity, making it the most macro-sensitive barrel in the system.”

ULSD NY Harbor (heating-oil) futures, a proxy for diesel, have surged 52% so far in March.

– Cold Comfort Dept… The fertilizer supply shock resulting from the closure of the Strait of Hormuz is tightening the input squeeze on farmers and likely forcing an acreage shift away from use nitrogen use crops like corn this spring. But it could be worse. The North America has the most sophisticated nitrogen market in the world, Bloomberg Intelligence s Alexis Maxwell said in a webinar Tuesday. Producers here are capable of meeting between 75% and 90% of its urea, ammonia and urea ammonium nitrate needs, she said.

Brazilian producers, meanwhile, may struggle to compete for fertilizer supplies in the global market due to limited access to affordable credit, while the European Union is more dependent on imports, particularly from Egypt and other Middle Eastern countries where natural gas supplies are threatened, she said.

– Cargill halts Brazil soy shipments to China due to inspection changes...Cargill has paused soybean export operations from Brazil to China after inspection changes made by the Brazilian government that make it difficult for traders to comply, the company’s Latin America head Paulo Sousa said on Wednesday. Sousa said Brazil’s Agriculture Ministry adopted a stricter sanitary evaluation on soybeans bound for China to check for pests and weeds after a request from the Chinese government. He said the new system is something unusual in the grains market. Without the certificates, soy vessels cannot travel.

Cargill has also stopped buying beans from local farmers in Brazil, Sousa said, since it cannot export them to China for the moment. Some posts on X on Wednesday by Brazilian grain brokers and farmers cited that there were hardly any bids by traders to buy local soybeans. China is by far the biggest client of Brazilian soybeans, buying around 80% of the beans the South American country exports. Brazil is the world’s largest producer and exporter of the oilseed.

– Prairie drought watch… February brought notable dryness and drought relief across the Prairies, although localized areas continue to suffer. The latest monthly update of the Canadian Drought Monitor shows 47% of Prairie agricultural lands were being impacted by abnormal dryness or some form of drought as of the end of last month. That is down from 62% in both January and December, and 71% in November.

Most of the Prairie Region experienced above-normal precipitation during February, with large portions of the region receiving 115% to more than 200% of normal. In contrast, southern Alberta and parts of southwestern Saskatchewan remained comparatively dry, with precipitation totals below 85% of normal and localized pockets receiving less than 60%.

Most of southern Alberta and southwestern Saskatchewan is classified as being in moderate drought, but some isolated areas are in a severe drought rating. The ugly news is that the current forecast is calling for below normal precipitation in the region during the month of March. This is concerning news for farmers there as warmer than normal temperatures in the last half of the month are expected to result in early planting. Rains are urgently needed in order to get crops off to a decent start.

– More Saskatchewan pulse acres very likely in 2026… MarketsFarm reporter Glen Hallick writes that due to high fertilizer prices, there s a strong possibility that Saskatchewan farmers will plant more pulses this spring. That would be in addition to the planted area recently projected by Statistics Canada, as nitrogen-based fertilizers have seen price hikes of 30% since the start of the current Middle East war. Vessels transiting the narrow Strait of Hormuz to and from the Indian Ocean and the Persian Gulf have come to a stop, which threatens global supplies.

Dale Risula, provincial specialist for pulse crops with the Saskatchewan Ministry of Agriculture says switching to pulses would make sense due to the nitrogen benefits they provide. But it may not be as much as one might think because there are other aspects that could influence farmers decisions, he added. Farmers crop rotations would be a major consideration as well as concerns over root rot, which has been a problem for pulse crops in Saskatchewan. Of the choices for additional pulse acres, Risula said the most likely would be lentils. Another selection he said farmers would consider is chickpeas. They re growing it away from the area it was intended for, which was the drier part of southwest Saskatchewan, he said, noting there are more chickpea varieties available.

StatCan recently forecast a 13.3% increase of planted chickpea area in Saskatchewan for 2026 at 559,100 acres. As for lentils and peas, Risula cautioned these pulses require good phosphorus levels, which is currently a problem in the province. Generally, our soils have been running down in phosphorus levels, which he said are cyclical. That would also mean farmers would have to consider the costs to applying phosphorus where levels are lower than normal and its availability. While urea prices have risen significantly, those for phosphorous are up only 5%.

– Cut to France non-EU soft wheat export forecast… Farm office FranceAgriMer cut for a fourth straight month its forecast for French soft wheat exports outside the European Union in 2025/26, leading it to raise its outlook for end-of-season stocks to a 16-year high. France is the EU’s largest wheat producer and it has faced stiff export competition. In a supply/demand outlook, FranceAgriMer reduced its forecast for non-EU soft wheat exports this season to 7.10 MMT from 7.20 MMT projected in February. That would still be double the amount exported outside the bloc last season and above the five-year average.

The office increased marginally its forecast for French soft wheat shipments within the EU in 2025/26 to 7.57 MMT from 7.56 MMT previously and 6.81 MMT in 2024/25.

It increased its outlook for soft wheat stocks at the end of 2025/26 to 3.39 MMT from 3.05 MMT last month, also due to a higher forecast of the delivered crop. The new stocks projection, now expected 37% above last season, marks the highest level since 3.43 MMT in 2009/10, FranceAgriMer data shows.

For barley, the office increased slightly its 2025/26 stocks projection to 1.38 MMT from 1.37 MMT last month, and 19% above 2024/25. For corn, projected 2025/26 stocks were raised to 2.33 MMT from 2.19 MMT, mainly due to an upward revision to harvest supply, now expected 6.4% above last season.

– US launches Section 301 probe against its major trading partners… as if the Trump administration doesn t already have enough wars on its hands…it has started the first of several sweeping trade investigations, setting the stage for new tariffs…the centerpiece of a push to replace levies struck down by the US Supreme Court.

US Trade Representative Jamieson Greer announced Wednesday that his office would begin a probe into more than a dozen major economies under Section 301 of the Trade Act focused on alleged excess manufacturing capacity. The investigations, which typically take months to complete, are required for the president to unilaterally place duties on imports from specific countries deemed to employ unfair trading practices. Economies that will be subject to the inquiry include some of the US s largest trading partners: China, the European Union, Mexico, India, Japan, South Korea and Taiwan. Switzerland, Norway, Indonesia, Singapore, Thailand, Malaysia, Cambodia, Vietnam and Bangladesh will also be investigated, said a Bloomberg report. Our view is that key trading partners have developed production capacity that is really untethered from the market incentives of domestic and global demand, Greer said during a telephone briefing for reporters.

Canada was not among the initial batch of targeted countries.

Outside Markets

The Dow Jones Industrial Average pushed 289.24 points lower on Wednesday to settle at 47,417.27, while the S&P 500 slipped 5.68 points lower to 6,775.80. Early Thursday, the March Dow Jones Futures are plummeting down another 445 points.

Global stock markets are skidding lower this morning as surging crude oil prices stoked inflation worries, which could force central banks to reassess interest rate moves. Wall Street futures were in the red as the escalating Middle East conflict dampened risk appetite. Canada s TSX stock index futures are following sentiment lower.

War headlines and energy prices will determine how risk appetite evolves in the coming days, Ipek Ozkardeskaya, senior analyst at Swissquote, wrote in a note. It is nearly impossible to give precise price forecasts. Instead, taking oil and energy prices as given, the longer they remain high, the shorter market rebounds are likely to be and the greater the risk of a notable (stock) market correction (lower).

The March US Dollar Index is up 0.285 at 99.510. The Canadian dollar was little changed against its US counterpart…currently quoted at 73.52 US cents.

April crude oil futures are rallying $7.16 higher to US $94.41/barrel. Oil prices are charging up as Iran stepped up attacks on oil and transport facilities across the Middle East, raising fears of a prolonged conflict and oil-flow disruptions through the Strait of Hormuz.

There are no signs of a de-escalation in the Persian Gulf and as a result, there is no end in sight to the disruptions to oil flows through Hormuz, ING analysts said. The only way to see oil prices trade lower on a sustained basis is by getting oil flowing through ?the Strait of Hormuz, ING said. Failing to do so means that the ?market highs are still ahead of us.

The International Energy Agency on Wednesday agreed to release a record 400 million barrels of oil from strategic stockpiles to combat the spike in global crude prices, with the US contributing the bulk of the supply. The IEA said all 32 member countries backed the move, the sixth coordinated stockpile release since the agency’s creation in the 1970s.

Meanwhile, explosive-laden Iranian boats appear to have attacked two fuel tankers in Iraqi waters overnight, setting them ablaze and killing one crew member, after projectiles struck four vessels in Gulf waters, said port, maritime security and risk firms. The latest attacks on ships linked to the US and Europe mark an escalation in the conflict, raising the number of ships struck in the region since fighting began to at least 16.

Grain Markets

Chicago soybean futures are rallying 3 to 15 cents/bu higher this morning, led by the nearby contracts and pressing 2-year highs. Bean futures saw gains of 12 to 14 cents in the front months on Wednesday. Soymeal futures are up $1 to $3/ton this morning after posting modest gains of 10 to 90 cents on Wednesday.

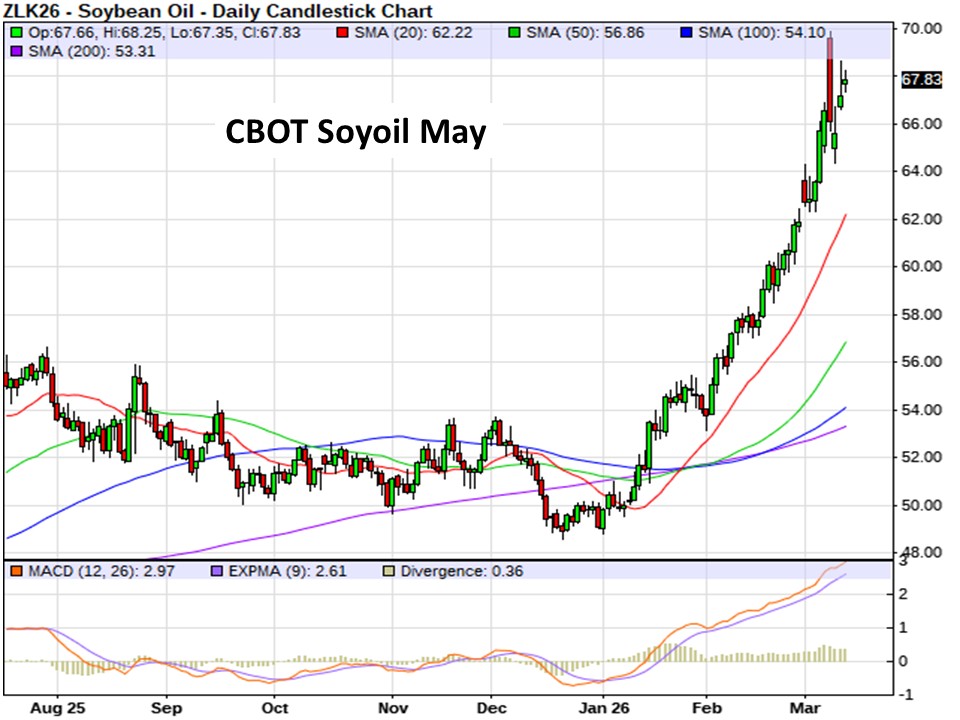

Soyoil futures are rising 36 to 70 points this morning, as it s massive surge higher for 2026 so far continues…rallying 122 to 175 points yesterday…with crude oil leading vegoil markets higher.

Bean oil also gained some strength on rumors the US Environmental Protection Agency’s 2026 biomass-based diesel renewable volume obligation (ROV), expected to be announced sometime in late March, was leaked at 5.4 billion gallons…along with ideas 70% of previously granted small refinery exemptions would be reallocated to remaining obligated refiners, which is believed to result in the effective 2026 RVO being near the proposed 5.61 billion gallons, if verified. This is in line with overall market talk/ideas in recent weeks. However, with crude oil sharply higher again, and nearly all biofuels-related talk/headlines of late being deemed supportive/bullish by the market, soyoil trade continues to trend higher.

USDA this morning reported US soybean export sales at 456,700 tonnes for the week ended March 5…coming midrange of trade expectations between

250,000 and 800,000 tonnes.

Noteworthy that Cargill halted exports out of Brazil to China due to tighter sanitary inspection changes following a request from China.

Traders anticipate soybean trade talk during US President Trump’s first trip to China since 2017 later this month. Tariffs, investment, and trade imbalances are expected to be high on the agenda, according to the Wall Street Journal.

Chicago corn futures are trading 3 to 5 cents higher this morning. The corn market closed with 8 to 9 cent gains in the front months on Wednesday…supported by rising crude oil.

EIA data from Wednesday morning showed a 31,000 barrel per day increase in US ethanol production from the week prior to an average 1.126 million barrels per day for the week ended March 6, the third highest volume ever recorded. Ethanol stocks saw a 757,000 barrel draw down to 25.58 million barrels.

USDA this morning reported US corn export sales at 1.531 MMT for the week ended March 5…coming about midrange of trade expectations between 0.8-2.2 MMT.

Near-term rain forecasts in South America continue to generally favor Brazil over Argentina. The Buenos Aires Grain Exchange will update conditions in Argentina later this week, while CONAB s new production estimates for Brazil are out Friday. Stateside, all eyes are on conditions as early fieldwork gets underway in parts of the US.

US wheat markets are higher this morning… Minnie spring wheat futures are up 5 to 7 cents, HRW gaining 7 cents and SRW wheat rising mostly 6 to 9 cents. The US wheat complex saw higher trade on Wednesday…spring wheat finished up 3 cents in the front months yesterday.

USDA this morning reported US wheat export sales at 455,400 tonnes for the week ended March 5…coming in at the higher end of trade expectations ranging between 200,000 and 450,000 tonnes.

The trade is monitoring precipitation totals in US hard and soft red winter growing areas as the crop gets closer to emerging from dormancy. Recent rainfall has generally been better in soft red winter growing areas than in the hard red winter region. The next 7 days look on the drier side for much of the southern US Plains, with the eastern half of the country and SRW area looking wetter.

The global wheat supply remains ample, but demand is good.

Traders are also watching conditions in Europe and the Black Sea region, along with the impacts of Russia s war on Ukraine and the military actions in the Middle East.

CANADIAN GRAIN MARKET

ICE canola futures snapped back higher on Wednesday following two days of declines, supported by strength in the broader global vegetable oil complex. Sharp gains in Chicago soyoil futures amid Iran war-related strength in crude oil spilled over to provide notable support for canola, which posted double-digit advances.

Canola was further underpinned by the strength seen in competing oilseeds and vegetable oils, including European rapeseed and palm oil. Weakness in the Canadian dollar offered further support.

May canola rallied $13.20 higher on Wednesday to close at $733.30/tonne, and November was $13.50 higher at $727.60.

For today… canola futures are continuing to trend higher, posting modest early morning gains of $3/tonne and looking to establish an 8-month high. Nearby May canola futures are $3.80 higher this morning at $737.10/tonne.

Gains support the resumption of the canola market rally that began near the start of 2026. Higher trending US soy complex and energy markets continues to lend support to our canola markets. Malaysian palm oil is higher following soyoil and diesel markets. European rapeseed futures are also higher.

While canola s price uptrend remains in place from a chart perspective, picking market tops under the current volatile geo-political environment is difficult. This latest rally in canola could lead to some shift in spring seeding plans, so growers might want to consider locking in some new crop pricing.

However, planted area could also change depending on fertilizer availability. Roughly a third of the world s urea fertilizer trade passes through the Strait of Hormuz, and its closure has sent prices climbing higher. Farmers may have already pre-booked fertilizer, but some question whether everything will be delivered.

Source: producer.com