Feeder cattle market incorporates risk discounts

For the week ending March 7, western Canadian feeder cattle markets traded $5-$10 per hundredweight lower compared to seven days earlier.

The market held value on Monday and Tuesday but then softened in the latter part of the week.

Strength in the feedgrains complex, along with weaker deferred live cattle futures, set a negative tone. Feedlot operators exhibited a cautious tone because feeding margins are in deep in red ink for late March and April.

Read Also

The Western Producer Livestock Report – March 19, 2026

Western Producer Livestock Report for March 19, 2026. See U.S. & Canadian hog prices, Canadian bison & lamb market data and sales insight.

Alberta packers were buying fed cattle on a dressed basis in the range of $535-$539 per cwt. delivered, up $4-$5 from last week. Using a 60 per cent grading, live prices would equate to $321-$323 per cwt. delivered.

Southern Alberta break-even pen close-out values average $340 per cwt. for March and $350 per cwt. for April. If the fed cattle price doesn’t increase by $20-$25 per cwt. on a live basis over the next 30-45 days, feedlot operators will lower their bids for replacements.

At the Ponoka, Alta., sale, a group of black mixed steers averaging 1,022 pounds on a diet of 14 per cent barley, three per cent canola meal and silage with full processing records, including implants, sold for $458 per cwt.

The Lloydminster market report had a group of 41 Simmental-based steers weighing 920 lb. that silenced the crowd at $484 per cwt.

The St Rose market report included a group of 21 Charolais steers with a mean weight of 816 pounds traded for $529 per cwt.

The Vermillion market report included 10 exotic steers averaging 552 lb. that sold for $738 and a pair of tan steers weighing 482 lb. that traded for $810 per cwt.

The Killarney, Man., market report had a smaller package of red heifers weighing 526 lb. that were valued at $660 and a three-pack of black heifers averaging 466 lb. priced at $697 per cwt.

The financial and commodity markets are reacting to the short-term and potential longer-term consequences of the U.S./Israel-Iran war. The equity markets experienced a steep sell-off during the week ending March 7. Higher energy prices may enhance inflationary pressures and result in lower consumer spending if the war extends beyond a couple of months.

If disposable income decreases and consumer spending slows, restaurant traffic will also decline.

The live and feeder cattle futures are factoring in a risk discount in anticipation of softer beef demand.

Prior to the war, fed cattle prices in Kansas reached an historical high of US$249 per cwt. on a live basis. Live cattle futures were due for a correction. Let me explain.

The Commitments of Traders Report for the live cattle futures had the commercial short position at 139,589 contracts during the week ending Feb. 24. This was the largest short position since late September.

It tells us that U.S. packers were well covered for their nearby requirements at the higher prices. We can say that demand for fed cattle was full.

When there is limited or extremely weak demand, the market trades lower.

On the live and feeder cattle futures markets, the commercial has been a net buyer while the managed money has been a net seller. This behaviour characterize a bearish or downward trending market.

During the first week of the war, there wasn’t much change in consumer behaviour. For the week ending March 7, restaurant traffic in the United States was nine to 12 per cent above year-ago levels.

In Canada, restaurant visits were up 18 to 20 per cent, on average.

Wholesale Choice beef finished the week priced at US$387 per cwt., while Select product was valued at $380 per cwt. Wholesale beef prices are up $20 per cwt. from mid-February, and these are the highest prices since September 2025.

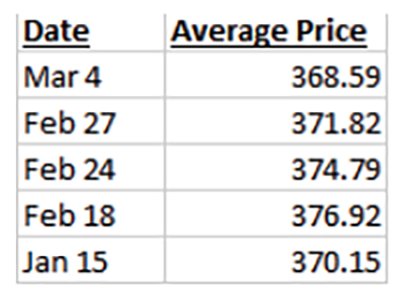

The CME composite price is the official cash settlement price for the CME feeder cattle futures at the contract final settlement. The U.S. Department of Agriculture provides the CME with the daily data.

The accompanying chart shows the seven-day average price for 700-899 lb. feeder steers.

Notice the composite price made an historical high on Feb. 18. This is important for Canadian cattle producers because it influences the North American price structure.

The USDA Jan. 1 Cattle Inventory Report had heifers for beef cow replacement at 4.714 million head, up one per cent from Jan. 1, 2025.

Statistics Canada’s Cattle Inventory Report for Jan. 1 had heifer retention at 543,700 head, up five per cent from 12 months earlier.

We’re expecting U.S. cow-calf producers to retain an additional 500,000 heifers for beef cow replacement in 2026. In Canada, we’re expecting cow/calf producers to retain an additional 50,000 to 60,000 heifers.

Heifer retention on both sides of the border will reduce the feeder cattle supply and result in lower feedlot placements.

Feedlots will be facing higher feedgrain prices moving forward due to higher energy prices. As well, we expect the corn and barley markets to incorporate a risk premium due to the uncertainty in production.

Grain and oilseed markets rallied in line with the crude oil market due to the energy component of the demand equation.

The USDA is factoring in a year-over-year increase in corn used for ethanol, and the recent rally in the crude oil has enhanced processing margins. This stronger ethanol demand comes on the heels of lower production estimates for corn and barley.

U.S. farmers are expected to seed 94 million acres of corn this spring, down 4.9 per cent, or 4.8 million acres, from the 2025 planted area.

Canadian farmers are expected to seed 6.440 million acres this spring, according to Statistics Canada. This is up five per cent, or 216,100 acres, from the 2025 planted area of 6.135 million acres.

Using a traditional abandonment rate and an average yield of 71 bushels per acre, production has potential to finish near 8.8 million tonnes, down from the 2025 output of 9.7 million tonnes.

Remember, the 2025 barley yield was a record 79.4 bu. acre.

Crude oil futures have potential to reach more than $100 per barrel. This will cause the Canadian dollar to trade near US80 cents.

The Canadian dollar has once again become a resource based currency. Canadian dollar appreciation against the U.S. greenback will temper the upside in the Canadian feeder cattle market.

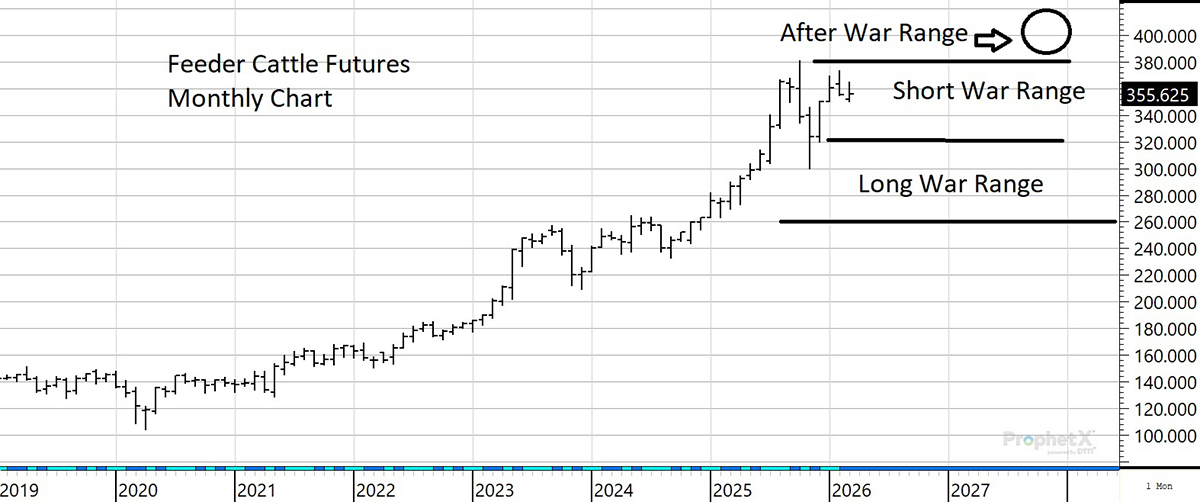

The feeder cattle futures have come under pressure in the short-term.

If the war lasts two months, I’m expecting the feeder cattle futures to trade in the range of $320-$380. If the war lasts longer than two months, the feeder cattle futures have potential to trade down to the range of $280-$300.

The downside of $260 is only for a prolonged war and extreme economic meltdown. If the war is over in a couple months, the feeder market would have potential to trade up to the $400 level in summer of 2026.

The feeder market needs to ration demand, and herd expansion is dependant on the feeder market remaining near or at historical highs.

Source: producer.com