AM Market Report – March 18, 2026

GOOD MORNING…HERE IS YOUR MORNING MARKET NEWS

OVERNIGHT GRAIN TRADE

ICE canola futures have turned overnight losses into small gains here in early morning trade…currently trading around $2/tonne higher to start this morning on front month contracts…much calmer price action after two days of wildly volatile swings. Chicago soybean futures are mixed this morning, but the front month contracts are down 2 cents/bu.

CBOT corn futures are narrowly mixed this morning. US wheat markets are mostly higher…spring wheat futures are up 1 to 3 cents, while the winter wheats are mostly 1 to 3 cents higher.

Read Also

AM Market Report – March 17, 2026

GOOD MORNING…HERE IS YOUR MORNING MARKET NEWS OVERNIGHT GRAIN TRADE After taking a beating on Monday, ICE canola futures are…

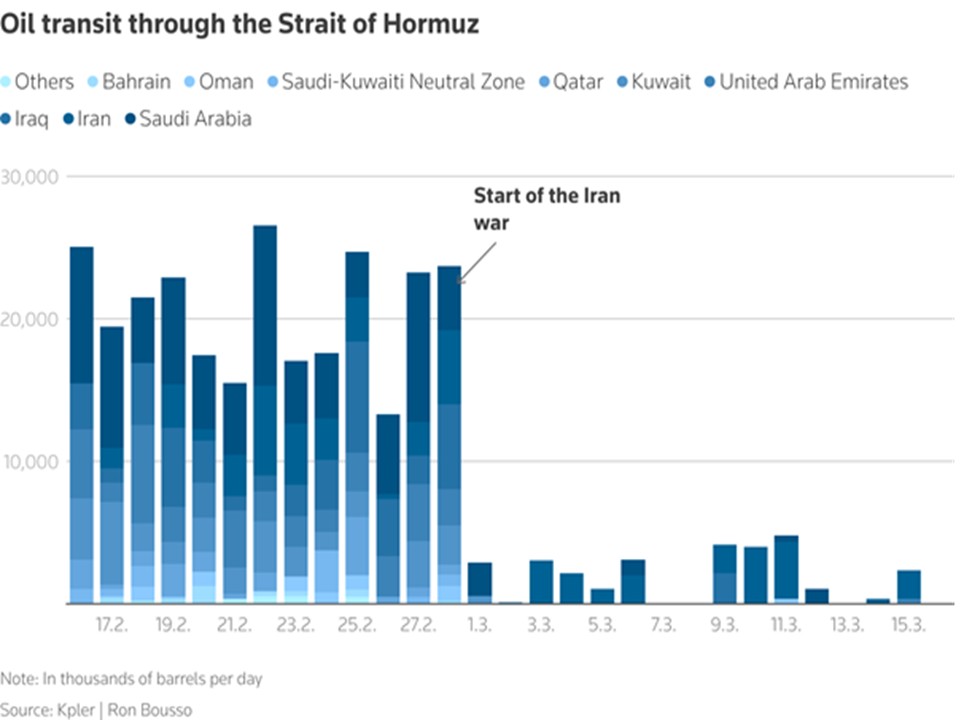

Grain market bulls at mid-week are working to stabilize their markets after early-week price volatility that still have them on their heels. Crop markets continue to react mainly to uncertain energy markets driven by the ongoing war in Iran. Markets are focused on efforts to reopen the Strait of Hormuz.

US President Donald Trump confirmed he would delay a highly anticipated meeting with Chinese leader Xi Jinping due to the Iran war. Trump, who was scheduled to visit Beijing March 31 to April 2, said Tuesday that the trip would take place in five or six weeks.

The discussion had been eagerly awaited for affirmation of the prospect for further purchases of US soybeans. A limit-down move by soybeans on Monday was sparked when Trump on Sunday questioned whether he would attend the summit amid dissatisfaction with China s lack of help in reopening the Strait of Hormuz.

In Other News

– Middle East war inflation shock… US Federal Reserve policy makers have more than just an oil shock on their hands. The closure of the Strait of Hormuz has also created a fertilizer supply shock that has clear-cut implications for food prices and is likely to further chill the outlook for additional rate cuts.

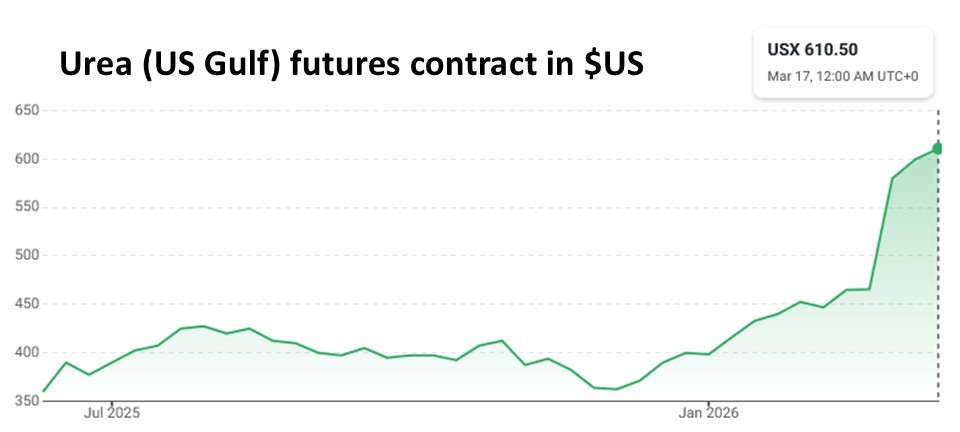

Canadian growers face rising input costs as global urea prices jump 40%, with analysts warning nitrogen fertilizer prices could double if the conflict drags on. With global supplies already tight from Chinese export restrictions and lost Russian gas, Canadian farmers heading into spring planting should expect tighter availability and margin pressure on nitrogen inputs.

The real-time inflation data, including real-time grocery prices, now suggest that the energy shock is worth at least 0.4 to 0.6 percent for CPI, and this may accelerate as the fertilizer price hike ripples through, said Ben Emons, founder of FedWatch Advisors, in a Substack post, referring to the consumer price index.

The closure of the strait, which accounts for 20% of global oil trade, has also trapped around 30% to 35% of global nitrogen exports and nearly half of global sulfur trade, he noted. Urea prices jumped 30% to 44% in less than two weeks, from around $475 to $680 a ton, while US Midwest nitrogen prices jumped more than $100/tonne in days.

When it comes to inflation, the transmission mechanism is fast and direct because fertilizer is one of the highest variable costs in crop production…the most exposed are fresh vegetables (nitrogen intensive), bread, pasta, cereals (wheat), and cooking oils (soybean and canola oil), Emons wrote.

Compared to the 2022 fertilizer shock that followed Russia s invasion of Ukraine, the 2026 shock may be worse, Emons said. As others have also noted, 2022 saw Russian fertilizers rerouted rather than taken off the market. Rerouting isn t an option with the strait closed.

The total shock effect could end up at 2.0 to 2.3 percentage points above baseline for food prices, peaking at 4% and then staying in place for 8 months, significantly clouding the inflation outlook, Emons said.

– Edible oils caught between weak demand and biodiesel bets… Global edible oil markets are behaving unpredictably as energy supply disruptions from the Middle East war lift hopes for biodiesel demand, though subdued buying from major importers such as India has clouded the price outlook, industry veteran Dorab Mistry said. “Wartime market behaviour is always very different and many developments come unexpectedly,” Mistry, the director of Indian consumer goods company Godrej International, told Reuters.

Crude oil prices jumped to a near four-year high last week after Iran responded to joint US-Israeli attacks by threatening to fire on vessels moving through the Strait of Hormuz. This rally has made the use of vegetable oils for biofuel production more attractive. “But right now, edible oil demand is subdued as prices have jumped. The market has high hopes for biodiesel. It remains to be seen which factor will eventually prevail,” Mistry said.

– Anticipation builds for possible US biofuel policy reveal at White House event… The Trump administration could be poised to make a big announcement on US biofuel policy next week. US Senator Chuck Grassley says he is hopeful US Renewable Volume Obligations for 2026 and 2027 will be announced during a celebration of agriculture at the White House March 27. We want RVO s to be what was speculated last year, that we get 5.6 billion gallons (bio/renewable diesel) without harm done to whatever they do on RINs. And then at least the 15 billion gallons or more on ethanol.

Trump has reportedly invited US farmers and biofuel producers to the White House as the industry awaits an official announcement on fuel additive mandates.

The US Environmental Protection Agency has indicated its decision on RVO s will be around the end of March.

– Oil and poor weather push up Ukraine rapeseed prices… Rising oil prices, driven by conflict in the Persian Gulf and poor weather conditions that damaged crops, are pushing up export forward prices for the new Ukrainian rapeseed crop, says the farmers’ union UAC. Ukraine, a large European rapeseed grower and exporter, harvested about 3.7 MMT of rapeseed in 2024. The harvest fell to 3.3 MMT in 2025, mostly because of unfavourable weather. Ukraine exports most of its harvest, mainly to Europe. The crop is used not only to produce edible oil, but also biodiesel. Rapeseed is currently selling at US $565-$580/tonne CPT Black Sea.

Consultancy APK-Inform said this month that Ukraine’s rapeseed harvest could increase to 3.83 MMT in 2026. Ukraine could export 2.7 MMT of rapeseed in 2026/27, versus 2 MMT in 2025/26, the consultancy said.

Outside Markets

The Dow Jones Industrial Average edged up 46.85 points on Tuesday to settle at 46,993.26, while the S&P 500 finished up 16.71 at 6,716.09. Early Wednesday, the March Dow Jones Futures are down 262 points.

Global stock markets were slightly higher overnight but have since turned lower coming into this morning. Investors await today s interest rate decisions ?from the US Federal Reserve and Bank of Canada.

Wall Street stock index futures are down this morning after major North American markets closed up slightly yesterday. Canada s TSX futures are also weaker this morning, pulling back from Tuesday s small gains, with investors expecting the BoC to keep interest rates here steady.

The Bank of Canada will announce its latest decision on interest rates this morning. The Bank is widely expected to hold rates steady at 2.25%. Since October the BOC has said borrowing costs are in the right place to support an economy impacted by US trade policy. Now, the war in the Middle East has added inflation risks and uncertainty globally.

The US Fed is also widely forecast to keep its policy steady, but the debate will very much centre on whether conflict with Iran is likely to disrupt US economic growth, threaten more persistent inflation or create a confounding mix of economic slowing and rising prices.

The June US Dollar Index is up 0.372 at 99.705. The Canadian dollar was little changed against its US counterpart…currently quoted at 73.09 US cents.

April crude oil futures are up $2.40 at US $98.61/barrel. Oil prices are higher this morning despite news crude exports resumed from Iraq s Kirkuk fields to Turkey s Ceyhan port via pipeline, providing modest relief to global markets concerned about supplies from the Middle East. The news provided some relief to the market. Any additional volume finding its way back to the market is valuable under the current situation. But we are still in a US $100/barrel oil environment, and ?the crisis around the Strait of Hormuz shows no sign of stopping yet.

Grain Markets

Chicago soybean futures are trading down 2 cents/bu in the front month contracts, but posting 1 to 3 cent gains in deferred new crop months. Bean futures close out Tuesday s session with deferred contracts 9 to 10 cents in the green, with front months only 1 to 3 cents higher. Soymeal futures are flat to less than $1/ton weaker this morning after finishing 20 cents to $1.30/ton lower on Tuesday. Soyoil futures are up a modest 2 to 10 points this morning after rallying 137 to 210 points higher yesterday.

The air was taken out of the soybean market earlier his week when US President Trump said he is delaying the trade meeting with China, now scheduled for five or six weeks away. The meeting between the two countries is now expected to be in mid/late April. Soy traders still have a lot of apprehension about future US soy business with China.

ANEC estimates the Brazilian soybean exports for March at 16.32 MMT, a reduction of 16.47 MMT from the previous number. Officials from Brazil are expected to visit China next week to discuss recent sanitary complaints and negotiate inspections framework. Brazil s record soybean harvest is about 60% complete and their prices are significantly below the US.

EU soybean imports from July 1 to March 15 were tallied at 8.74 MMT according to the European Commission, down from 9.81 MMT last year.

Chicago corn futures are narrowly mixed this morning, with front month contracts up a penny. The corn market finished steady to 2 cents higher on Tuesday, though the July contract slipped cent.

Traders will begin to turn their attention to the March 31 US Planting Intentions Report, one of the major marketing moving reports of the year. The new crop soybean-to-corn price ratio, at a two-month low, is nearly favoring corn planting. But there are ongoing concerns about input costs and availability ahead of widespread US spring planting.

Traders are also watching Argentina s harvest, along with the first crop harvest and second crop planting in Brazil.

There s some chatter that an ag-focused end-of-the-month event at the White House will be positive for biofuels.

US wheat markets are slightly higher this morning…Minnie spring wheat futures are rising 1 to 3 cents higher, while HRW is gaining 3 cents and SRW wheat is up 1 to 2 cents. US wheat futures were under pressure on Tuesday, with losses across the three markets…spring wheat finishing down 7 to 10 cents in the front months yesterday.

The next week looks dry for much of the US Plains from Nebraska to Texas, with much of SRW country also remaining dry with scattered precip. The Kansas Crop Progress report from Monday showed winter wheat conditions down 4% to 52% good/excellent. Most US winter wheat growing areas are expected to see record or near record temperatures by week s end, which should speed up emergence.

EU wheat production was estimated at 142.6 MMT according to Coceral, down 1.3 MMT from the previous estimate. The European Commission estimates the EU wheat exports at 16.77 MMT from July 1 to March 15, up 1.23 MMT from the same period last year.

Fundamentally, old crop world wheat ending stocks remain robust, with mostly record production around the world for 2025-2026.

The trade is monitoring conditions in Europe and the Black Sea region, along with trade impacts from Russia s war on Ukraine and the military action in the Middle East.

CANADIAN GRAIN MARKET

ICE canola futures rebounded impressively on Tuesday, clawing back a good portion of Monday s steep losses. The bounce back in canola was largely tied to strength in competing vegetable oils and firmer crude oil. Chicago soybeans were higher yesterday…with soyoil futures strongly higher…with gains in European rapeseed and Malaysian palm oil offering support as well.

Gains in soybeans were attributed at relief that a planned meeting between US President Donald Trump and his Chinese counterpart Xi Jinping will still ultimately go ahead, even as Trump said it may be delayed five or six weeks. It was uncertainty over that meeting yesterday that led to limit declines in both soybeans and soyoil.

May canola jumped $26.90 yesterday to close at $729.50/tonne, and November was up $28.60 to $727.30.

For today… canola futures are clawing back declines seen overnight to now trade as much as $2/tonne higher. Nearby May canola futures are up $2.50 at $732.00/tonne as the market stabilizes/recovers following Monday s steep sell down.

With energy markets rising again this morning, should continue to support vegetable oil markets, and in turn support canola and soybeans. The impact of an exceptionally strong diesel market should provide good underlying support.

There is currently no sign of any off-ramp for Trump s war with Iran. In fact, attacks by Iran escalated overnight following the killing of one if its senior officials while reports also suggest Trump may have ground troops take over Kharg Island soon. With it being the outlet for roughly 90% of Iran’s exports, Iran has vowed to never let that happen. Add in the lack of international support for Trump’s desire to takeover of the Strait of Hormuz and the situation appears likely to get more volatile than less.

Reports that US biofuel blending mandates and small refinery exemption (SRE) reallocations will be announced March 27 helped to inspire Tuesday’s rally.

Stay informed with our daily market videos. Each video quickly covers key futures moves, price trends, and market signals that matter to Canadian farmers. Get clear, timely insights in just a few minutes. Bookmark https://www.producer.com/markets-futures-prices/videos

To access the latest futures prices, go to https://www.producer.com/markets-futures-prices/

Source: producer.com