AM Market Report – April 30, 2026

GOOD MORNING…HERE IS YOUR MORNING MARKET NEWS

OVERNIGHT GRAIN TRADE

Grain futures markets are taking a breather this morning from recent gains. ICE canola futures are trading $1 to $2/tonne lower after charging $50/t higher since April 17.

Chicago soybean futures are posting modest 1 to 2 cent/bu declines this morning, with fading soymeal, though recovering bean oil trade this morning is giving some support to beans.

CBOT corn futures are down 2 cents currently.

US wheat markets are also lower this morning…spring wheat futures down 4 to 7 cents, HRW selling down 7 to 9 cents and SRW wheat losing 5 to 8 cents.

Read Also

Prairie Weather

The radar image is clear for most of western Canada as a high pressure ridge builds into the region. This…

Profit-taking from the shorter-term traders was featured in corn and wheat futures overnight.

Grain and oilseed markets on Wednesday continued their higher trade, as traders factored in trade disruptions in the Middle East. Additionally, ongoing struggles with US winter wheat crop conditions underpinned wheat and corn prices. Wheat stocks remain plentiful in 2025/26, but widespread global output reductions are expected in 2026/27.

As the calendar turns to May, traders are squarely focused on updated weather forecasts. On the bear side, it’s that time of the month for spec funds to take some profits.

Latest on the war in the Middle East

– Brent crude oil hits four-year high before pulling back on reports US mulls Iran military options

– US seeks to deploy hypersonic missile for the first time against Iran

– California gasoline price surges above $6/gallon as Iran war spurs gains

– One by one, Asian currencies are faltering as oil worries worsen

– India s rupee currency drops to record low as amid crude oil surge

– US seeks forfeiture of seized oil tankers linked to Iran

US President Donald Trump will receive a briefing on new military options for action in Iran, signaling the potential for fresh escalation in the Middle East, Axios reported.

A US official told WSJ that the siege is crushing Iran s economy, underscoring that Washington sees economic pressure as a major point of leverage. The market takeaway is that this keeps geopolitical risk firmly embedded in energy, freight, and commodity markets, even if the situation stops short of a broader military escalation. For agriculture, the biggest read-through is not immediate grain demand, but the cost side: crude, diesel, fertilizer, freight, and biofuel-linked markets remain vulnerable to further risk premium as long as Iran s export flows and the Strait of Hormuz remain under pressure.

In Other News

– USDA attache projects Canada 2026 wheat harvest at 36.2 MMT… The USDA’s attache in Canada projected the country’s 2026 wheat harvest at 36.159 MMT, down about 10% from the prior year. The report cited expectations of a drop in planted area and a return to near-average wheat yields after a record-high national yield for Canada’s 2025 crop.

“Farmers are shifting away from wheat and planting alternative crops such as soybeans in Manitoba, Ontario, and Quebec, and barley and canola in Saskatchewan and Alberta,” the USDA’s report said, noting large wheat stocks and lower wheat prices compared to last year.

The report projected Canada’s 2026/27 wheat exports at 28.5 MMT, down from 29.7 MMT in current year 2025/26.

– USDA attache projects Australia wheat crop at 29 MMT... A report released by the USDA’s attache in Australia projected the country’s 2026/27 wheat harvest at 29 MMT, down 19% from the prior year. The report cited expectations of a smaller harvested area and a return to near-average wheat yields after relatively high yields in 2025/26. “While the season has begun favorably in most key regions, uncertainty around in-season rainfall and the potential development of El Ni o conditions present downside risks,” the report said.

The report projected Australia’s 2026/27 wheat exports at 23.5 MMT, down from 26 MMT in 2025/26, primarily due to lower production.

The report noted rising farm input costs due to geopolitical tensions in the Middle East. “Diesel and nitrogenous fertilizer prices have approximately doubled in the lead-up to planting,” the report said. However, the report said, “seasonal conditions remain the dominant factor influencing planting decisions and production outcomes.”

– Global biofuels boom… Demand for biofuels has been growing in many parts of the world. Governments, particularly those in countries with big farming sectors, have viewed crop-based fuels as a way to support domestic agriculture, cut transport fossil fuel emissions and help address climate change, said a Bloomberg report.

The energy crunch caused by the closure of the Strait of Hormuz has created a further incentive to boost production: energy security. Since the Iran war broke out, major biofuel producing countries Indonesia, Malaysia, Thailand, Vietnam and Brazil have moved to allow more biofuels to be mixed into transport fuels to cut down on imports and ensure security of supply. Biofuels now account for about 6% to 8% of global farmland use, compared with about 1% 20 years ago. In the US, production has been growing since the 1980s and it s the world s largest ethanol producer.

Governments see biofuels as a quick win: They can be blended into existing fuels and used in most engines, while leveraging existing infrastructure like refineries and fuel stations, said the report. For countries with large agricultural sectors…particularly emerging economies…biofuels offer a way to repurpose crops, support farmer incomes and cut fuel imports.

– World rice supply threatened by Iran war, El Nino… Rice supply is expected to fall this year as farmers cut planting acreage across Asia because of fertiliser shortages and soaring fuel costs ?from the Iran war, with an emerging El Nino also set to squeeze output of the world’s most consumed staple. Rice is central to global food security, ?and even modest supply disruptions can ripple through countries, lifting prices and straining household budgets, particularly among price-sensitive consumers in Asia and Africa.

The effects of the Iran war are impacting farmers in top exporters Thailand and Vietnam as well as the import-reliant Philippines and Indonesia, growers and traders said. The war has cut fuel and fertiliser ?flows through the Strait of Hormuz, a key chokepoint that connects the Gulf to global markets. Southeast Asia’s mainly smallholder farmers also face mounting stress as the El Nino ?weather phenomenon is set to usher in hotter, drier conditions for the region in the second half of the year.

Farmers have already started planting ?rice in some countries and are using fewer inputs because prices have gone up,” said Maximo Torero, chief economist at the UN FAO. “We are going to see a tighter global supply situation ?in the second half of the year and early next year.”

In 2008, export curbs by key suppliers more than doubled prices to about $1,000/tonne, triggering unrest in several countries. More recently, ?supply tightness in 2022 to 2023, exacerbated by India’s export restrictions, lifted prices and prompted panic buying.

– Vessel carrying grain Ukraine says was stolen will not unload in Israel...Ukrainian Foreign Minister Andrii Sybiha ?said that a ?vessel carrying grain that ?Kyiv says was stolen from its territories occupied by Russia would not unload ?its cargo in Israel, describing it ?as a “welcome development” on Thursday. Ukraine has asked ?Israel to ?seize ?the vessel, ?amid a diplomatic tussle between the two countries over the shipment.

– EU kickstarts Mercosur pact to counter US trade hit... The European Union and South American bloc Mercosur will implement on Friday a contentious free trade agreement that ?the EU in particular hopes will benefit exporters and calm critics, even if it cannot fully offset the blow from US tariffs. Backers including ?Germany and Spain say the agreement will help compensate for the hit from US President Donald Trump’s tariffs and reduce reliance on China for critical minerals. France and other critics argue it will increase imports of cheap beef and sugar and undercut domestic farmers, and environmentalists say it will increase rainforest destruction.

Either way, economists caution that the economic gains from this pact and others concluded in recent ?months by the EU will be modest and are unlikely to fully make up for lost US trade.

The European Parliament, whose approval is required, voted in ?January to challenge the agreement in the EU’s top court, which could take up to two years to rule, but the European ?Commission decided to provisionally apply the deal from May 1. Supporters hope the EU’s largest ever agreement in terms of tariff reductions, which took 25 years to negotiate, will swiftly ?benefit EU exporters so that when the EU assembly does vote, perhaps in two years’ time, the advantages will be clear.

Alongside Mercosur, the EU has ?rushed to conclude trade agreements with India, Indonesia, Australia and Mexico since Trump’s re-election. The accords help to shore up free trade at a time when Trump’s tariffs and Chinese export curbs on critical minerals undermine a rules-based global order.

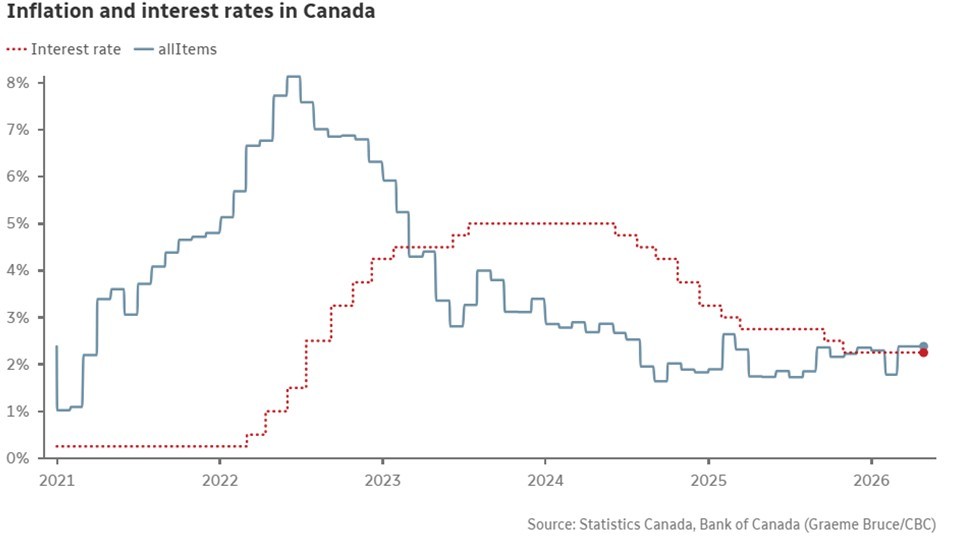

– BoC holds rate at 2.25%, but warns of energy and trade risks… The Bank of Canada held its benchmark interest rate steady on Wednesday, but warned that interest rates may need to change depending on the duration of the oil price shock and the outcome of trade talks with the United States and Mexico. As widely expected, the bank s governing council kept its policy rate at 2.25% for the fourth consecutive time, even as the conflict in the Middle East has pushed energy prices sharply higher and squeezed Canadian consumers at the gas pump.

Governor Tiff Macklem said his team decided to look through the energy price shock in the near term. But he said the trajectory of monetary policy will depend to a significant degree on how long oil prices remain elevated…something that s contingent on the outcome of peace talks between the United States and Iran. Our baseline forecast assumes oil prices will come down and US tariffs will remain at current levels. If this holds true, a policy rate close to current settings looks appropriate, Mr. Macklem said.

– US also holds rates steady… Down in the Exited States of America, prospects for an interest rate cut by year-end all but evaporated Wednesday following what appeared to be a contentious Federal Reserve policy meeting. Federal Reserve officials left US interest rates unchanged Wednesday… at a range of 3.25% to 3.5%…as fully expected, but revealed a deepening division over the outlook for policy amid increased uncertainty caused by the conflict in the Middle East.

Four officials voted against the decision. The surprise was that three of the regional Fed presidents dissented not against the decision to remain on hold, but against language in the policy statement but because they did not support inclusion of an easing bias in the statement at this time. In other words, they don t want the Fed signaling that a rate cut remains more likely to be the next move than a rate hike.

Meantime, Fed Chair Jerome Powell said he intends to remain at the US central bank as a member of its Board of Governors, and will not leave until a controversial criminal investigation into the central bank is “well and truly over with transparency and finality.”

– Stagflation starting to grip European Union… The eurozone economy unexpectedly slowed at the start of 2026, with soaring energy costs triggered by the Iran war threatening stagflation in the months ahead, according to a report by Bloomberg. First-quarter gross domestic product rose 0.1% from the previous three months…below the 0.2% median estimate in a Bloomberg poll. Highlighting the dangers still unfolding just hours before the European Central Bank sets interest rates, a separate release from Eurostat showed consumer prices surged 3% in April…the fastest pace since September 2023 and led by rising energy costs.

Slowing economic growth and accelerating inflation are a recipe for dreaded stagflation. European Commission President Ursula von der Leyen has warned that the economic damage may be felt for years to come. France and Italy have already trimmed their outlooks for economic growth, while Germany has halved its forecast for 2026 to 0.5%.

Outside Markets

The Dow Jones Industrial Average finished Wednesday down 280.12 points at 48,861.81, while the S&P 500 slipped 2.85 points to 7,135.95. Canada s S&P/TSX composite stock index fell 266 yesterday to close at 33,318. Early Thursday, the June Dow Jones Futures are up 293 points.

Global stock markets are higher this morning. Oil prices initially climbed overnight following a report that the US was ?considering fresh military action against Iran and lead to a protracted Middle ?East oil supply disruption that could hurt global economic growth. But oil futures then pulled back from Trump clarifications that the current US blockade of Iranian shipping was sufficient for now.

Regardless…prospects for any near-term resolution to the Iran conflict or a reopening of the Strait of Hormuz remain dim.

The June US Dollar Index is down 0.452 at 98.375. The Canadian dollar strengthened against its US counterpart…currently quoted at 73.20 US cents.

June crude oil futures are down $2.46 at US $104.42/barrel.

Trump reportedly told aides yesterday to prepare for an extended blockade of Iranian ports. The Strait of Hormuz has been largely closed since the end of February, taking hundreds of millions of barrels of crude off the market. US data showed a sharp drop in US domestic crude inventories last week and record crude exports at 6.4 million barrels a day.

Grain Markets

Chicago soybean futures are trading 1 to 2 cents/bu lower this morning, pulling back from overnight strength, which saw the new crop November contract hit a new high for the move at $11.78/bu. Bean futures ended Wednesday s trade action with most contracts up 2 to 9 cents, led by the old crop contracts. Some back months were fractionally to 2 cents lower.

On Wednesday, the July bean contract posted its highest close since March 13. By Wednesday night, that same contract topped $12.00/bu before falling back to currently trade 2 cents lower at $11.95…and still contained within its 7-week sideways range.

Soymeal futures are down $2 to $3/ton this morning after falling 40 cents to $5.40/ton yesterday. Soyoil futures are mixed but turning slightly higher now this morning. Bean oil rallied 87 to 193 points higher on Wednesday to fresh contract highs.

USDA this morning report US soybean export sales of 258,100 tonnes for the week ended April 23, down at the bottom end of trade expectations which ranged between 200,000 to 600,000 tonnes.

US soy planting progress should continue over the next week with much of the area from the Dakotas through Kansas stretching over to much of Illinois looking with very scattered rain totals in NOAA s 7-day forecast. There have been some delays due to weather in portions of the region, but nationally, soybean planting is running at a record pace.

Recent events in Iran and the Middle East make high-level, face-to-face trade talks between the US and China in mid-May less likely. But so far, those talks have not been canceled. China is a major trading partner of both the US and Iran.

Chicago corn futures are trading around 2 cents/bu lower this morning. The corn market held on to gains on Wednesday, despite pulling off early highs. Most nearby contracts were fractionally to 2 cents higher, with a few deferreds steady to fractionally lower.

EIA s weekly report showed a larger than expected drop in US ethanol production in the week that ended on April 24, of 31,000 barrels per day to an average 1.009 million barrels per day. That was also 31,000 bpd below the same week last year. The drop in output helped to draw down stocks, which were down 1.067 million barrels to 25.881 million barrels.

USDA this morning report US corn export sales of 1.598 MMT for the week ended April 23, midrange of trade expectations which ranged between 1.0 to 1.9 MMT.

US corn planting is ahead of average nationally, but heavy rainfall has led to some early chatter about replanting, and some areas are still dry. There s also some background talk about corn losing acres to beans due to input issues.

US wheat markets are weaker this morning as bulls take profits into the last trade day of April… Minnie spring wheat futures are mostly 4 to 7 cents lower, HRW down 7 to 9 cents and SRW wheat losing 5 to 8 cents. The US wheat complex fell off early session highs on Wednesday, as month-end profit-taking got off to a day early start, though spring wheat still managed to finish yesterday up 2 to 4 cents.

USDA this morning report US wheat export sales of 226,100 tonnes for the week ended April 23, mid to upper end of trade expectations which ranged between 0 to 300,000 tonnes.

The wheat complex does look overbought after the recent rally and US prices were already high compared to competing exporters. However, nothing s really changed weather-wise. Rain forecasts for parts of the Plains are scattered and not enough to break the drought heavily impacting the US hard red winter crop. Soft red winter is in relatively good shape, but parts of that region have recently received heavy rainfall. US spring wheat planting is slower than average.

Globally, planted area could be impacted by higher input costs. USDA s ag attach estimates the Australian 2026/27 wheat crop at 29 MMT, down 6 MMT from last year if realized. The attach office in Canada estimates the country s crop at 36.16, down 3.8 MMT from last year.

Traders are also monitoring crop developments in Europe, Russia, and Ukraine.

CANADIAN GRAIN MARKET

ICE canola futures ended with strong gains on Wednesday amid further strength in surging crude oil. Canola hit its highest levels since early last summer as there continues to be little progress toward ending the US-Iran conflict, even as a ceasefire between the two countries remains in place. The Strait of Hormuz, through which 20-25% of global seaborne oil normally flows, remains essentially blocked.

Chicago soybeans and soyoil were higher yesterday, with European rapeseed mainly stronger. Palm oil was mostly lower.

The Canadian dollar was mixed after the Bank of Canada held its key overnight lending rate at 2.25%.

July canola jumped $16 on Wednesday to close at $763.90/tonne, and November climbed $15 to $759.70.

For today… canola futures are seeing some modest month-end profit-taking so far this morning…trading $1 to $2/tonne lower. But overnight declines have been trimmed as CBOT soyoil is starting to turn slightly higher now. July canola futures are down $1.60 at $762.40/tonne currently…but are up a strong $50/t since April 17.

While some month-end profit-taking is at work this morning, the desire to be long commodities remains the prevail market sentiment, with canola futures flirting with contract highs. Strength in energy markets continues generally, as there has been little headway made on negotiations to end the war in the Middle East, and the Strait of Hormuz remained effectively closed to traffic.

Crude oil is key. With little sign of a resolution to the Iran war, prolonged strength in crude oil would remain supportive for world vegoils and canola.

US soybean crush margins are at record highs, while Canadian canola margins are also rising. The canola board crush margin calculated by ICE Futures showed domestic processors making profits of roughly $350 on every tonne of canola they crush. That compares with only $123/tonne at the same time a year ago. The gains in crude oil are making producing biodiesel more profitable, giving a bullish spark to soyoil and canola.

Stay informed with our daily market videos. Each video quickly covers key futures moves, price trends, and market signals that matter to Canadian farmers. Get clear, timely insights in just a few minutes. Bookmark https://www.producer.com/markets-futures-prices/videos

To access the latest futures prices, go to https://www.producer.com/markets-futures-prices/

Source: producer.com