AM Market Report – March 2, 2026

GOOD MORNING…HERE IS YOUR MORNING MARKET NEWS

OVERNIGHT GRAIN TRADE

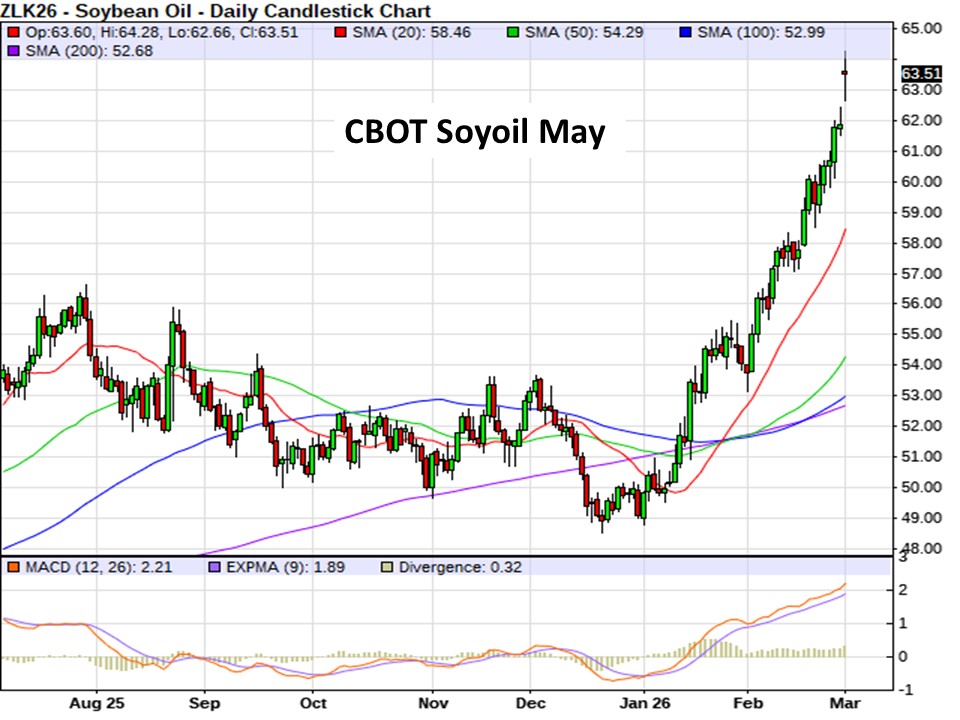

A bit of a mixed bag this morning for the grain markets, though ICE canola futures are charging mostly $10 to $12/tonne higher to fresh highs for the rebound rally started back just before Xmas. A catapult higher in CBOT soyoil futures (new contract and 2-year highs), comes with rallying world vegoil and energy markets this morning…giving our canola market some real jump. Also…China officially lowered tariffs on imports of Canadian canola seed over the weekend…bullish news.

Read Also

Prairie Weather

A low pressure system is pushing across northern Alberta this morning that will push across the northern areas of the…

Chicago soybean futures are trading 4 to 6 cents/bu lower on the market s front end contracts after hitting a 10-month high at one point overnight…torn between falling soymeal and rallying soyoil.

CBOT corn futures are rising 1 to 2 cents this morning to a six week high.

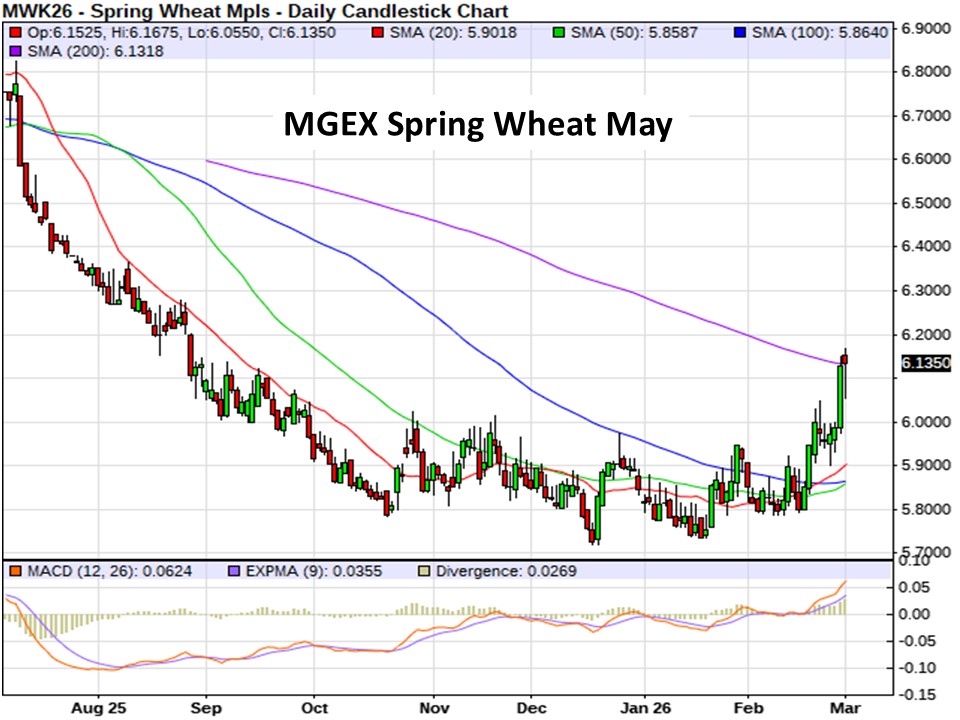

US wheat markets are mixed after rallying higher on Friday. This morning…Minnie spring wheat futures are starting the day mostly up a penny on the nearbys. HRW wheat futures are up 3 to 4 cents right now, but SRW wheat is 2 to 3 cents. Wheats surged to end last week as drought concerns sparked price strength as US winter crops come out of dormancy.

February was kind to agricultural commodities overall, with soyoil stealing the show so far in 2026…advancing 14.6% for the month. Year-to-date, soybean oil futures have rallied more than 26%.

In Other News

– China slashes anti-dumping tariff on Canadian canola… China on Saturday sharply reduced its tariff rate on imports of Canadian canola seed in the final ruling of a 17-month anti-dumping investigation, following a thaw in relations between Beijing and Ottawa. The announcement came a day after China said (Friday) it would suspend some tariffs on other Canadian agricultural products imposed during its trade spat with Canada.

The final anti-dumping tariff was lowered to 5.9% from a preliminary 75.8% imposed in August, according to a statement from China s commerce ministry. The levy will be effective from March 1 and will last for five years. In addition to the anti-dumping duty, Canadian canola remains subject to China’s standard 9% import tariff, bringing the total effective duty to a more manageable 14.9%.

The outcome broadly aligns with Canadian Prime Minister Mark Carney’s expectations. After his visit to Beijing in January, Carney had said he anticipated a total tariff rate of around 15%. China was Canada’s second-largest market for canola in 2024.

The decision comes amid a wave of visits to Beijing by Western leaders, including Carney, as US President Donald Trump’s trade policies have strained Washington’s traditional alliances. China has sought to present itself as a more stable and reliable economic partner in contrast.

Carney went further than his European counterparts by securing a deal with China and signalling Canada’s ambition to play a leading role in a new global trade order aimed at reducing dependence on the United States.

On Friday, China suspended its 100% tariffs on Canadian canola meal and pea imports and will halt 25% tariffs on lobster and crab imports from March 1 through the end of 2026. However, canola oil and pork were not mentioned in the statement.

– US-Israel wage war against Iran… US-Israeli air strikes on Iran continue for a third day today after the killing of Iranian Supreme Leader Ayatollah Ali Khamenei, a cleric who long seemed to preside not just over Iran but half of the Middle East?…raising the risk of regional instability. Oil and gas leaped and stocks slumped as the war intensified.

US President Donald Trump s explicit goal of regime change marks another move away from his previous non-interventionism and toward an aggressive foreign policy. Donald Trump is vowing to keep hitting Iran with air strikes, even as he holds out the possibility of returning to the bargaining table with Tehran.

At home: Prime Minister Mark Carney is backing the strikes on Iran but won t contribute militarily.

– US military action in Iran may threaten Trump-Xi summit in April… One month before Chinese President Xi Jinping and US President Trump are set to convene at a much-touted summit in China, the US leader s toppling of another friend of China risks stoking tensions between the world s biggest economies, Bloomberg reported Sunday. After US and Israeli military strikes on Iran wiped out the Islamic Republic s Supreme Leader, Chinese Foreign Minister Wang Yi on Sunday called it unacceptable to openly kill the leader of a sovereign country and institute regime change. Speaking by phone with his Russian counterpart, Wang warned that the US president risked driving the Middle East into the abyss.

Condemnation of Washington from China s top diplomat stands out during a delicate period when officials on both sides are trying to steady relations before Trump arrives in Beijing on March 31. Complicating that task, (Trump) has ousted two leaders with ties to Beijing in quick succession this year, after the US in January snatched Venezuela s Nicol s Maduro, said the report.

Before this weekend s US-Israel attacks on Iran, there were already strains developing ahead of the high-stakes Trump/Xi summit meeting. The South China Morning Post reported last week of anxiety in Beijing due to a perceived reluctance on the part of the US to plan for the event. Just a month ahead of the March 31 to April 2 summit in China, preparations are inadequate, bilateral contacts anemic and outcomes diminished, the article said, citing analysts and former government officials who tied the shortfall to Trump s reluctance to delegate, disdain for process and focus on quick wins, banking instead on personal magnetism and his gut.

– Carney signs deals worth billions in diplomatic breakthrough with India’s Modi… Prime Minister Mark Carney and his Indian counterpart announced Monday what they re a calling a new partnership, a series of multi-million dollar deals and a commitment to sign a free trade agreement by year s end as the two look to turn the page on years of frosty bilateral relations marked by allegations of Indian foreign interference.

In a statement to reporters after a one-on-one meeting with Indian Prime Minister Narendra Modi, Carney said Canada is going all-in on diversifying trade. What s been agreed to after these leaders talks is designed to more than double two-way trade to some $70 billion a year by 2030, he said, as Canada continues a push to reduce its dependence on the US.

Carney framed this new course as not just a return to how things were but rather an ambitious revisioning of what the two Commonwealth countries can do together in an uncertain era marked by instability. At the centre of this more robust relationship will be a Comprehensive Economic Partnership Agreement…a free trade deal…that Carney said the two sides hope to sign by December, which will offer Canada exports relief from Indian tariffs that are quite high on some goods.

What Carney and Modi signed today: five memorandums of understanding expanding Canada-India partnership across energy and critical minerals, technology and AI, talent, culture and defence worth $5.5 billion in total. Perhaps the most significant is a $2.6 billion deal between the Government of India and Saskatoon-based Cameco to supply nearly 22 million pounds of uranium for nuclear energy generation from 2027 to 2035. That s a big boon for Saskatchewan, which sits on one of the world s largest reserves of high-grade uranium.

Saskatchewan separately announced that it has created a joint pulse protein centre of excellence with India. These farm products have been at the centre of past disputes because India imposed tariffs on Canadian peas and lentils. The press release announcing this new centre mentioned nothing about possible tariff relief for these agri-food imports.

– Trump EPA to shift at least half of waived US biofuel obligations to big refiners… The Trump administration has settled on a plan that would require big US oil refineries to make up for at least half of the US biofuel blending volumes obligations waived in recent years under the Small Refinery Exemption program. The report noted the decision could be unwelcome news for larger American oil refiners that have argued that additional blending obligations would raise their costs. But it could help the US biofuel industry by boosting demand for blending credits.

The US Renewable Fuel Standard requires oil refineries to blend billions of gallons of ethanol and other biofuels into fuel or buy credits, called RINS, from refiners that do. Small refineries, however, can apply to have those requirements waived if they can show economic hardship. The question of whether to reallocate those exempted blending obligations to big refiners has sparked a long running battle between US farm and fuel industries.

Biofuel groups have pushed the administration to fully reallocate the exempted gallons, saying it is crucial to support biofuel producers and the farmers growing their feedstocks. Refiners, meanwhile, have warned that reallocation unfairly forces larger plants to cover for smaller rivals, raising their compliance costs and potentially increasing pump prices.

– Canadian cattle herd sees first annual increase since 2018… The Canadian cattle herd was larger on Jan. 1, 2026 than it was one year prior…the first year-over-year increase since 2018, Statistics Canada reported on Friday. Canadian farmers and ranchers held 11.1 million cattle and calves on Jan. 1, up 2.5% from one year before. Inventories rose across all categories of cattle. Beef heifers for breeding were up 4.8% and beef cows were up 1.9%.

Producers held 3.6 million calves, 4.3% more than a year prior. This was mainly due to a 42.7% increase in international imports of calves between July and December.

In the last six months of the year, slaughter of cattle and calves fell by 6.5% to 1.6 million head, StatCan said. International exports dropped by 8.9% to 361,300 head. Despite decreases, feeder and slaughter cattle prices climbed to record highs over the latter half of 2025 on global demand.

Meantime, Canadian hog farmers reported 13.9 million hogs on farms as of Jan. 1, down 0.8% from one year prior. They reported 1.2 million sows and gilts, up 0.4%. The number of boars was unchanged at 15,300 head.

The pig crop for the second half of 2025 rose by 3% year-over-year to 15.2 million. StatCan attributed this to an increase in demand from processors and international trade. International exports of live hogs were up 8% year over year at 3.5 million head. Hog slaughter rose by 1.8% to 10.9 million head.

– Brazil to raise soy sales to China… Brazil, which is reaping a record soy crop this year, may increase bean exports to China in 2026 amid lower Argentine shipments and in spite of stronger competition from US farmers. Last year, lower US soy sales to China allowed Brazil, the world’s largest soybean producer and exporter, to ship 85.4 MMT to China, an 18% increase from 2024, according to Brazilian government data. Analyst Hedgepoint Global Markets is betting Brazil’s soy sales to China may increase further this marketing year.

China is expected to raise imports by 4 MMT to 112 MMT in 2026, according to Hedgepoint, creating demand that either Brazil or the US could supply. “Argentina will export less this year because its crop is smaller,” said Luiz Fernando Roque, a Hedgepoint Global analyst. “That already puts another 4 or 5 MMT in the hands of the Americans or Brazil.”

In 2025, the US share of China’s soybean imports fell to 15%, from 21% the year before, while Brazil’s rose to 73.6%, up from 71% in 2024, according to Hedgepoint data. Argentina’s share jumped to 7%, from 4%, according to Chinese government data.

– Soybeans back up at Brazil river port… Truck drivers in Brazil are facing unusually long delays to deliver soybeans at the Miritituba port terminal in the Amazon rainforest, as a record harvest of approximately 180 MMT overwhelms logistics at one of the world’s key export hubs for the crop. The backlog for moving soybeans from the world’s largest producer and exporter highlights ongoing logistical hurdles in Brazil’s agricultural supply chain. Much of Brazil s soybean exports are destined for China.

Miritituba, a critical transshipment point, handles roughly 12 MMT of grains annually, including soy and corn. Firms such as Cargill, Bunge, and Brazil’s Amaggi, operate river terminals where crops are loaded onto barges for downstream transport to larger facilities capable of filling ocean-going vessels. Traffic is usually heavy at this time of the year. Adding to the industry’s setbacks, Indigenous activists invaded a Cargill transshipment facility in Santarem this month in protest against government policy to dredge and expand shipping capacity through the Amazon basin.

– EU fast-tracks trade deal with South America… The European Union will provisionally apply a contentious free trade agreement with South American bloc Mercosur to ensure the bloc secures first-mover advantage, European Commission President Ursula von der Leyen said on Friday. The European Commission concluded its largest ever trade pact in terms of tariff reductions with Argentina, Brazil, Paraguay and Uruguay after 25 years of negotiations. The EU executive has said it will remove some 4 billion euros (US $4.7 billion) of duties on EU exports.

Germany and other supporters such as Spain say the deal is essential to offset business lost due to US tariffs and to reduce reliance on China for critical minerals. Opponents led by France…the EU’s largest agricultural producer…say the deal will sharply increase imports of cheap beef, sugar and poultry, undercutting domestic farmers who have staged repeated protests.

– India likely to see above-average temperatures in March… India is likely to experience above-average temperatures across most regions in March following a warmer-than-usual February, predicts the India Meteorological Department. Both maximum and minimum temperatures are expected to remain above average in most areas during March. Higher temps during the crucial grain-filling and maturity stages in key wheat, pulse and rapeseed-growing states could cut yields, trimming overall production from what was expected.

– US farm cash subsidy payment enrollment begins… USDA announced the opening of the enrollment period for the US Farmer Bridge Assistance (FBA) program. The enrollment period for the $11 billion in cash handout s opened Feb. 23 and closes April 17 with payments expected to hit accounts in

short order. The following commodities are eligible for FBA: barley,

chickpeas, corn, cotton, lentils, oats, peanuts, peas, rice, sorghum, soybeans, wheat, canola, crambe, flax, mustard, rapeseed, safflower, sesame, and sunflower.

Outside Markets

The Dow Jones Industrial Average tumbled 521.28 points lower on Friday to settle at 48,977.92, while the S&P 500 was down 29.98 at 6,878.88. Early Monday, the March Dow Jones Futures are down another 572 points.

Oil prices have rallied, while stock markets sell-off this morning as military conflict in the Middle East looked set to last for weeks, threatening to upend a global economic recovery and perhaps reignite inflation. Wall Street stock index futures fell after all three major indexes ended decisively lower on Friday. TSX futures are also lower after Canada s main stock index ended Friday s session in the red.

The March US Dollar Index is up 0.910 at 98.475. The Canadian dollar weakened against its US counterpart…currently quoted at 73.15 US cents.

April crude oil futures are surging up $5.10 at US $72.12/barrel. Oil and natural gas prices surged as Israeli and US strikes on Iran and retaliation by Tehran forced shutdowns of oil and gas facilities across the Middle East and disrupted shipping in the crucial Strait of Hormuz.

At least in the short term, the disruption to global energy supply is substantial, (and) this clearly adds upside risks to the oil price, said Michael Langham, emerging markets economist at Aberdeen Investments.

Grain Markets

Chicago soybean futures are steady to lower this morning…nearby contracts currently 4 to 6 cents/bu lower, while deferred new crop futures are flat. This has been a retracement after bean futures shot higher at one point at Sunday nights open. Bean futures posted 6 to 10 cents gains Friday in the nearby contracts, as May was up 17 cents/bu on the week.

Soymeal futures are falling $3 to $7/ton to start this morning after finishing steady to $2/ton lower Friday in the front months, though May did finish $6.70 higher on the week.

Soyoil futures are blasting higher this morning…soaring 134 to 165 points higher to fresh contract and 2-year highs. Crude oil is generating bullish spillover momentum this morning following the US/Israel strikes on Iran over the weekend. But soybeans are under pressure over uncertainty on US/China relations.

Bean oil has also been boosted so far in 2026 by optimism over US renewable fuel standards. The big news this past week was a Reuters report that the Trump administration has settled on a plan that would require US big oil refineries to make up for at least half of the biofuel blending volume obligations waived in recent years under the Small Refinery Exemption program.

Managed money added another 20,591 CBOT soybean futures contracts to their net long position as of Feb 24, taking the position to 184,202 contracts according to CFTC data released on Friday.

AgRural estimates the Brazilian soybean crop at 39% harvested, which is still shy of the 50% from the same period last year. They also trimmed their projection for the country s bean output by 3 MMT to a still record large 178 MMT.

Traders are watching weather in Argentina and Brazil, while waiting for any signs of new demand from China. That s a big question for beans right now because of tariff uncertainties and Brazil s price discount to the US.

Gut feeling…with after the soybean market has rallied $1/bu since the start of 2026, with bean futures now at their highs posted in November…charts have a double top look to them. Looks a place to make another incremental cash sale for old crop…might even consider a first forward sale on new crop for fall delivery.

The actual supply/demand balance sheet might not justify higher prices beyond current levels, unless there s a catastrophe during the US growing season. South American production prospects are trimming around the edges, not collapsing. Strong crush and oil support are limiting downside. But abundant global supplies mean rallies need respect.

Chicago corn futures are a bit mixed to slightly higher…nearby Mar contract down, but deferreds are 1 to 2 cents higher. The corn market rose 4 to 5 cents across the front months on Friday, as May managed an 8.75 cent gain last week to its highest level in six weeks. Crude oil is providing some spillover support this morning following the US/Israel strikes on Iran over the weekend.

Commitment of Traders data tallied managed money cutting another 13,548 contracts from their net short position in the week ending on Feb 24, taking it to 13,867 contracts.

Brazil s first crop corn harvest is now 36% complete according to AgRural, shy of the 46% pace from last year. The second crop is 66% planted in the center-south region, below the 80% from 2025. Rain chances for Argentina are scattered, while parts of Brazil are too dry for ideal second crop development. Any significant loss of quality in South America could set the stage for better demand for US corn globally. However, there s no sense of panic here…still good supply available.

US wheat markets are mixed this morning… Minnie spring wheat futures are mostly around a penny higher, HRW is up 3 to 4 cents, but SRW wheat is mostly 2 to 3 cents lower. The US wheat complex rallied across all three markets on Friday to lead the grain complex. Spring wheat futures posted 8 to 15.75 cent gains last week, with the May contract up 12.75 cents. Short covering was noted to close out February.

Minnie spring wheat futures have posted impressive gains of late off a multi-month flat pricing base, which looks rather encouraging chart-wise. General buyer interest has elevated prospects of an extended rally.

But in trying to find the bullish headlines to support last week s rally in wheat futures…to be honest…not much there…other than the heightened world geopolitical risks. There s still a lot of wheat out there. Just doesn t scream bullish breakout fundamentally. Suggests to me…short-covering…with markets still comfortable with supplies. In such environments, short-term rallies are typically meant to be sold.

Traders are watching the weather. Near-term, rain is forecast for the eastern US Plains (SRW). Long term, models show a dry pattern for the western Plains (HRW), with dry conditions expected through late March into April. The big test for winter wheat is conditions when the crop emerges from dormancy, which could happen early in parts of the Northern Hemisphere. Upcoming weather could provide volatility, but rallies still face supply headwinds.

CANADIAN GRAIN MARKET

ICE canola futures ended weaker on Friday, as traders took profits ahead of the weekend. Strength in Chicago soyoil futures, which were modestly higher again on Friday, remained a supportive influence for canola. European rapeseed and palm oil were also higher to end last week. But advances in the Canadian dollar weighed on canola.

May fell $5.30 on Friday to close at $687.70/tonne, and November lost $6 to $691.90.

For today… canola futures are rallying mostly $9 to $13/tonne higher this morning, though the expiring nearby March contract is up $15/t. May canola is up an impressive $13 to $700.70/tonne, flirting with the psychologically important $700 level.

Open conflict in the Middle East this weekend as US and Israel launched massive air strikes into Iran has triggered rallies in the energy sector. The death of Iran s leader Ayatollah Khamanei is notable as the potential void in leadership and calls for Muslims to avenge his death could make for a lengthy conflict. Iran has responded by attacking US bases in every surrounding Middle East country, risking a significant escalation in the region with few off-ramps.

As it relates to canola…the heating oil (ULSD diesel) market has charged higher, taking prices to levels not seen since October 2023. With the Strait of Hormuz being effectively shut down by Iranian threats of counterattack (causing insurance companies to cancel all coverage), energy markets are unlikely to fall back as quickly as they did in June. The surge in diesel has flowed through to soyoil and canola markets this morning.

The cards have been thrown into the air regarding how this all plays out. Price gaps higher in soyoil and canola on geopolitical chaos suggests one of two things to me as a chart technician. Option 1…this wild market uncertainty has seen the establishment of an exhaustion gap marking a short-term top after such a substantial rally, or…Option 2…could be a midpoint gap should the conflict escalate, which then puts the June 2025 high on the canola weekly chart in play.

Outside the Middle East turmoil dazzle, our canola market has some additional bullish news playing out as China announced over the weekend it has lowered import tariffs on Canadian canola seed to a cumulative at 14.9% for the next five years, down from 75.6%.

Bottom Line…canola price momentum remains supportive right now, but there is plenty of headline risk in this environment amid the lack of certainty. South America is trimming soy yields, but still producing big crops. US biofuel policy remains a key swing factor for oilseeds. Tariff news makes noise, but lacks clarity. Oilseed markets maintain comfortable supply, so price rallies should be deemed selling opportunities.

On the feed grains… Prairie old crop feed barley cash bids have quietly improved this week. Nothing flashy…but noticeable…Lethbridge cash pricing reaching as high as $274/tonne last week. If you ve got unpriced tonnes sitting in the bin, it s worth checking your local bids. Small improvements add up.

Corn imports from the United States are priced at a similar level to barley, with a delivered-Lethbridge price of $274/tonne.

Seasonal price movement in the feed grains typically sees values strengthen through the spring, as supplies tighten and farmers turn their attention to the next year s crop.

Solid export demand continued to underpin the domestic feed market, with more grain moving offshore this year. Canadian Grain Commission data showed 1.984 MMT of barley were exported through 29 weeks of the marketing year, up from 1.2 MMT at the same point a year ago. Country-specific data through December shows China remains the largest single destination for Canadian barley in 2025/26, accounting for just over half of the total export movement.

Stay informed with our daily market videos. Each video quickly covers key futures moves, price trends, and market signals that matter to Canadian farmers. Get clear, timely insights in just a few minutes. Bookmark https://www.producer.com/markets-futures-prices/videos

To access the latest futures prices, go to https://www.producer.com/markets-futures-prices/

Source: producer.com