AM Market Report – March 3, 2026

GOOD MORNING…HERE IS YOUR MORNING MARKET NEWS

OVERNIGHT GRAIN TRADE

Grain markets are on the rise to start this morning. ICE canola futures are building on Monday s rally, up another $4 to $5/tonne this morning. Chicago soybeans are posting impressive 6 to 11 cents/bu gains, led by the front month contracts.

CBOT corn futures are rising 2 to 5 cents, also led by the nearbys.

US wheat markets are also in the green this morning…spring wheat up 2 cents, HRW 6 cents higher and SRW adding 3 to 5 cents.

Read Also

AM Market Report – March 2, 2026

GOOD MORNING…HERE IS YOUR MORNING MARKET NEWS OVERNIGHT GRAIN TRADE A bit of a mixed bag this morning for the…

While canola was already higher yesterday, US soybean, corn and wheat markets are so far seeing a Turnaround Tuesday rally this morning following Monday s selling pressure. Monday’s US grain markets prices moved higher in their initial reaction to the US-Israeli strikes on Iran but turned lower (except for higher CBOT soyoil which is correlated to moves in crude oil).

As the war intensified overnight, and crude oil prices extended gains on worries of a prolonged conflict, farm markets are moving higher this morning. However, early gains in grains today may be challenged in the daytime session, as the gold and silver markets are getting hammered early today.

Latest developments on war in the Middle East…

— China has condemned the US-Israeli attack on Iran, urges all sides of the war to safeguard the Strait of Hormuz

— Iran says Strait of Hormuz is closed to shipping traffic, threatening to attack any ship entering the Strait; US denies that claim

— Europe s natural gas prices jump as much as 33%

— Two drones attack US embassy in Riyadh, Saudi Arabia

— US Sec. of War Hegseth rejects endless war, while Trump insists no fixed timeline

— Global stock markets lower and trader/investor anxiety increasing

— Iran launched new missile wave on US interests in Qatar, Bahrain, Oman

In Other News

– Global oil, gas shipping costs surge as Iran vows to close Strait of Hormuz… Global oil and gas shipping rates soared, with supertanker costs in the Middle East hitting all-time highs, as the US-Iran conflict intensified after Tehran targeted ships passing through the Strait of Hormuz, according to shipping data and industry sources. Shipping through the Strait of Hormuz between Iran and Oman, which carries around one-fifth of oil consumed globally as well as large quantities of liquefied natural gas, has ground to a near halt after vessels in the area were hit as Iran retaliated to US and Israeli strikes. The disruption and fears of prolonged closure have caused oil and European natural gas prices to jump as the conflict triggered multiple oil and gas shutdowns in the Middle East.

An Iranian Revolutionary Guards senior official said on Monday that the Strait of Hormuz is closed and Iran will fire on any ship trying to pass, Iranian media reported. The US military’s Central Command said the Strait is not closed despite the Iranian statements.

The escalating conflict is threatening supplies in one of the world s key energy producing regions, with the straight handling as much as 20% of the world s oil shipments.

– Iran conflict drives up urea prices… Hostilities in the Middle East are already affecting North American fertilizer prices. Urea barges in New Orleans traded roughly US $50-$80 per short ton, or 11 to 17 per cent higher, on March 2 compared to Feb. 28, according to Argus Media. The conflict presents a major risk to North American urea supplies ahead of spring planting, according to an analysis published on the Argus website.

If shipments from the Middle East are delayed or disrupted, the US would lose a critical source of urea, likely crunching supply and laying the groundwork for upward price volatility, Argus analyst Calder Jett said. Middle Eastern producers of urea so far have suspended offers and are grappling with shipping complications in the Strait of Hormuz.

StoneX fertilizer analyst Josh Linville said the conflict couldn t come at a worse time for North American farmers, who are gearing up for spring. Commercial shipping traffic through the Strait of Hormuz has started to grind to a halt. Vessel owners do not want to put their ships and crews in harm s way. The market impact will depend on how long the strait is shut down, he said.

US President Donald Trump has stated that US military operations in Iran are likely to last at least one month. The unfortunate part is that means you have locked in three of your top 10 global urea exporters and three of your top 10 global anhydrous exporters, said Linville. Saudi Arabia is also a major exporter of phosphate fertilizer.

The phosphate market was already suffering from the lack of Chinese exports. The world s largest exporter of the product said it will not be shipping any product until August 2026.

– Carney, Modi pledge to boost trade… Prime Minister Mark Carney and Indian Prime Minister Narendra Modi have pledged to boost cooperation in trade and supply chains during Carney s first official visit to India. Carney announced a $2.6 billion agreement expanding Canada s uranium shipments to India for nuclear energy generation. The two sides also finalized the terms of reference for a trade deal. Both leaders said they expect a trade deal to double two-way trade and hailed a new era of partnership between the two nations. Canada and India have also agreed to cooperate in sectors including liquefied natural gas, critical minerals, solar and hydrogen.

– Russian wheat export prices edged up last week… Russian wheat export prices rose slightly last week, with the market still assessing the impact of strikes on Iran. Analysts lowered their export estimates for February, but expect an increase in March.

The price of Russian wheat with 12.5% protein content for free-on-board (FOB) delivery in April was US $233.50/tonne at the end of last week, up $0.50 from a week earlier, the IKAR consultancy, said. The situation with FOB prices at the beginning of this week, following the US and Israeli strikes on Iran, is not yet entirely clear, they noted. “Exchange prices have skyrocketed. But we have a number of factors that counteract the rise in FOB prices,” he said. Prices may be affected by the situation with purchases by importers from the Persian Gulf countries and neighbouring countries as well as by dynamics of insurance premiums. “In other words, it is not necessarily the case that the rise in exchange prices will result in an increase in FOB prices.”

Russian FOB wheat was supported last week by slow selling and a strong rouble, the head of SovEcon agency Andrey Sizov said. SovEcon estimated the price for Russian wheat with 12.5% protein at $233 to $236/tonne FOB, compared with $232 to $236 the previous week. The agency lowered its estimate for wheat exports in February by 0.3 MMT to 3 MMT. SovEcon also trimmed its total 2025/26 Russian wheat export forecast by 0.3 MMT to 45.4 MMT.

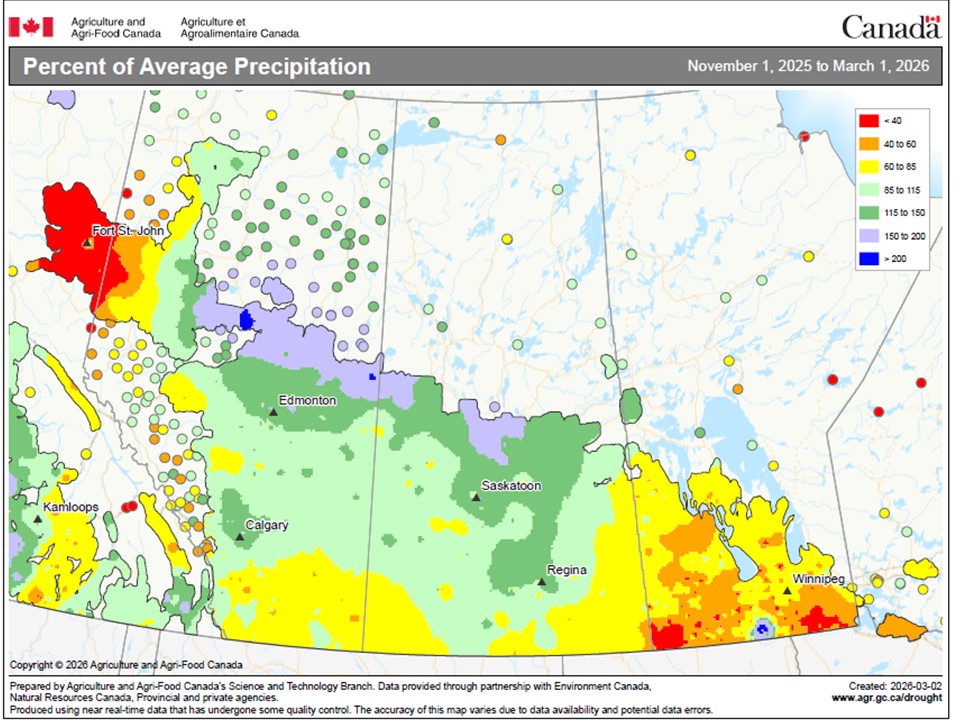

– Prairie winter precipitation variable… The winter months brought near to below normal amounts of precipitation to most of Western Canada, but with pockets of variability. As shown on the map below, central and northern Alberta generally received near to slightly above normal precipitation during the Nov. 1 March 1 period, while parts of central Saskatchewan also saw close-to-average moisture levels.

In contrast, drier conditions were focused across the southern Prairies, particularly southern Manitoba and southeastern Saskatchewan, where precipitation was below normal, in places falling below 60% of average and locally even lower. Southern Alberta also shows sizeable areas of below-average precipitation, though conditions improve moving northward. The Peace River region was drier farther west.

As spring draws nearer, some Prairie areas remain stubbornly dry, particularly parts of the Peace River region and the southwestern Prairies, which continue to wrestle with long-term moisture deficits.

A spring flood outlook from Manitoba last week said overall basin conditions in that province point to low to moderate spring runoff potential. Soil moisture levels at freeze-up were near normal to below normal across most regions, with winter precipitation trending near or below seasonal averages, the outlook said.

The latest monthly update of the Canadian Drought Monitor showed 62% of Prairie agricultural lands were being impacted by abnormal dryness or drought as of the end of January. That was unchanged from December and down from 71% at the end of November. The February update should be released in the coming days.

– South American corn, soybean report… Noted crop consultant Dr. Michael Cordonnier s latest weekly South American corn and soybean crops report saw him leave his 2025/26 Brazil soybean estimate unchanged at a record large 178.0 MMT with a neutral-to-lower bias. Brazil s soybeans were 39% harvested as of late last week compared to 50% last year, according to AgRural. This is the slowest harvest pace in five years.

Cordonnier also left his Brazil corn estimate unchanged this week at 135.0 MMT, with a neutral-to-lower bias. Safrinha corn in Brazil was 66% planted as of late last week compared to 80% last year, according to AgRural. The planting remains the slowest since 2022.

Cordonnier s Argentina soybean production estimate was left unchanged this week at 47.0 MMT, with a neutral-to-lower bias, but if rainfall during March ends up dryer-than-normal, the production estimate will decline, he said. His Argentina corn crop estimate was left unchanged this week at 53.0 MMT, with a neutral-to-lower bias. Corn in Argentina was 3.6% harvested as of late last week. The late-planted corn will continue to need additional moisture through the months of March and April, said Cordonnier.

– Australia s winter crop production revised higher… Higher-than-expected yields have pushed Australia s total winter crop production for marketing year 2025-26 to 68.4 MMT, according to the Australian Bureau of Agricultural and Resource Economics and Sciences (ABARES). The new estimate in the March Australian Crop Report is up 2.1 MMT from the December estimate and 13% year-on-year for winter crops that include wheat, barley and canola, for which Australia is a major global supplier. Production would be 15% above the five-year average of 59.5 MMT to 2024-?25 and the second largest winter crop on record, ABARES said.

Winter crop harvest results indicate that yields outpaced expectations, particularly in Western Australia and Victoria where total winter crop production has been revised up 2% and 11%, respectively, from the December 2025 forecast, ABARES said.

Wheat production is estimated to increase by 5% to just under 36 MMT in 2025 26, 7% above the five-year average. Barley is estimated to have reached a record 16.3 MMT, up 23% from the previous year and 21% above the five-year average. Canola production is estimated to have increased by 20% to 7.7 MMT in 2025 26, the second largest canola crop on record.

Outside Markets

The Dow Jones Industrial Average slipped 73.14 points lower on Monday to settle at 48,904.78, while the S&P 500 edged up 2.74 points to 6,881.62. Early Tuesday, the March Dow Jones Futures are plunging 893 points lower.

A sell-off across world stock markets has deepened this morning as the widening conflict in the Middle East fuelled a spike in energy prices that raised investor concern about the impact on the global economy.

Wall Street futures are deep in the red this morning after the major US stock indexes surprisingly bounced back from early losses yesterday to finish the day mixed on Monday. TSX futures stock index futures are weaker this morning, after Canada s main stock index ended Monday s session at a record high, up 201 points at 34,541.

For Western Europe, the most notable development is another surge in natural gas prices…which is bringing back quite a lot of fears of potentially a repeat of what we saw in 2022, when Russia invaded Ukraine, said George Moran, European macro strategist at RBC Capital Markets. It feels like the market is interpreting this as much more of an inflationary shock than a growth shock. Of course, it could still have a growth impact, he said.

Inflation around the world is seen picking up due to the US-Israel war with Iran, according to a global survey of economists by Bloomberg News. The biggest inflationary threat from the war stems from increased oil and gas prices, as well as knock-on effects from things like higher airfares and distribution costs. The majority of respondents predict the war will have a minimal impact on gross domestic product in either North America, Eurozone or China, but much will depend on how long the conflict lasts, said the report.

The March US Dollar Index is up 0.848 at 99.185. The Canadian dollar weakened against its US counterpart… currently quoted at 73.00 US cents.

April crude oil futures are charging $5.58 higher at US $76.81/barrel. Crude oil benchmarks continue to rally strongly higher this morning as the widening US-Israeli conflict with Iran heightens fears of further Middle East oil and gas supply disruption. While there are concerns about oil flows through the Strait of Hormuz, a greater risk to the market would be Iran targeting additional energy infrastructure in the region. This could lead to more prolonged outages, ING analysts said in a note.

Grain Markets

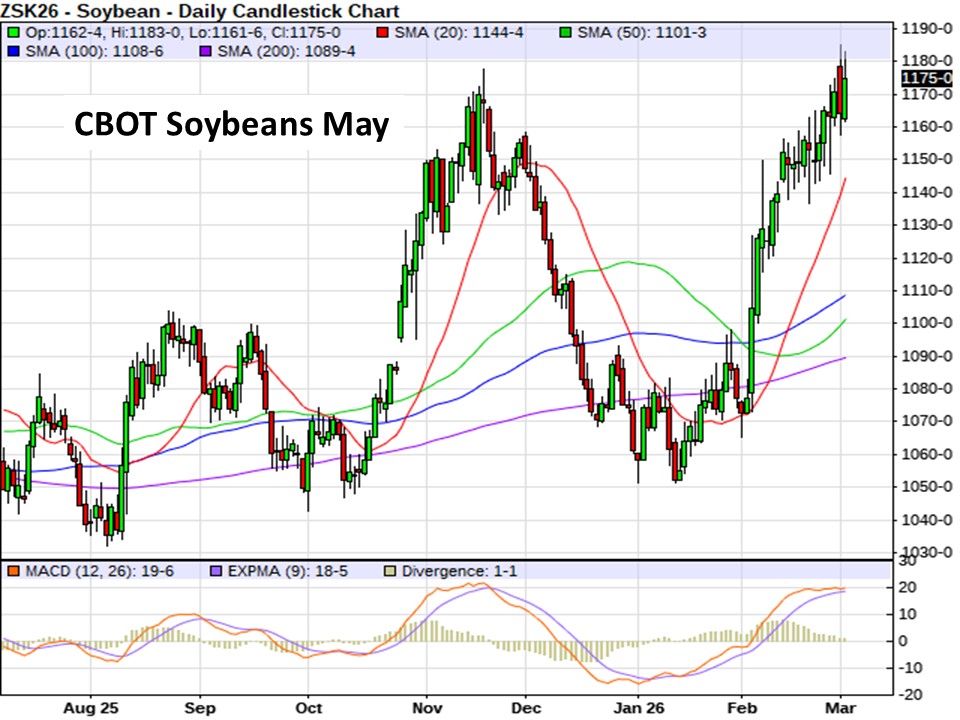

Chicago soybean futures are posting 6 to 11 cents/bu gains this morning, led by the front month contracts. Bean futures finished 5 to 8 cents lower in the front months on Monday, with new crop contracts fractionally higher. May beans are 11 cents higher right now at $11.75/bu…still flirting with its high posted in November…and needs to push higher soon before chartist talk of double top formation becomes more acute.

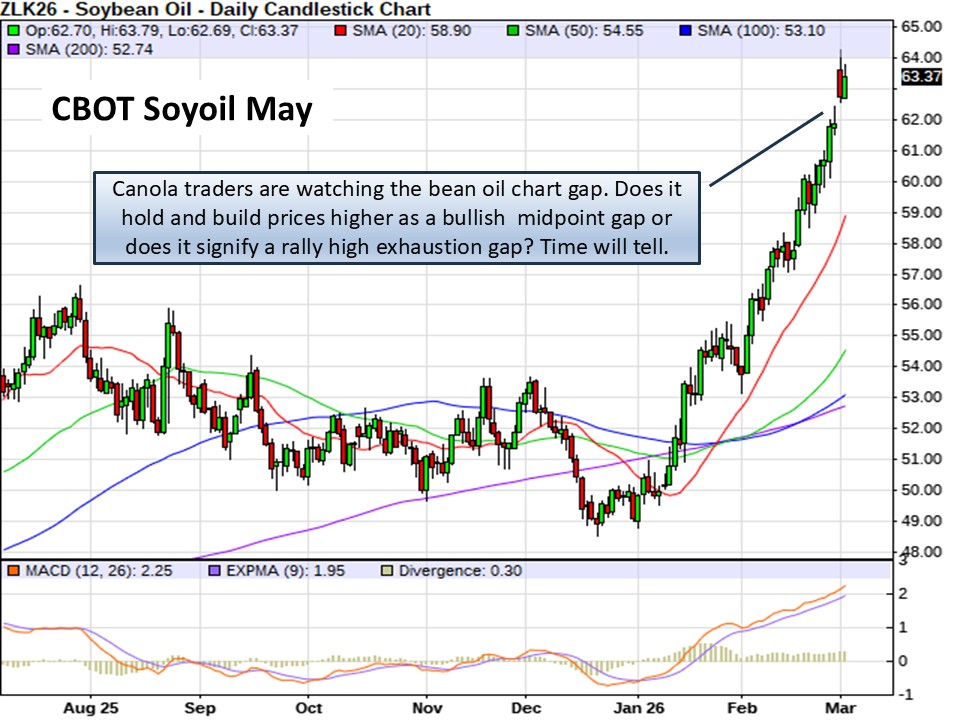

Soymeal futures are up $1 to $2/ton this morning after falling $2 to $7/ton on Monday. Soyoil futures are 52 to 67 points higher this morning, adding to yesterday’s 70 to 92 point gains. Soyoil is up on biodiesel demand expectations and the strength in crude oil.

Monday s US Export Inspections report showed 1.138 MMT of US soybeans shipped in the week ended Feb 26. That was 66.9% above the week prior and 62% larger than the same week last year. China was the largest destination of 734,698 tonnes. The US marketing year total is now 26.18 MMT of soybeans shipped since September 1, which is still 30.4% below than the same period last year.

Monthly US Fats & Oils data from Monday showed 227.8 million bu of soybeans crushed in January, exceeding trade estimates. That was a drop of 0.87% from December, but well above the same month last year. US soyoil stocks rose 11.72% from the end of December to 2.43 billion lbs, which was 33.9% larger than the same period last year.

Brazil s soy harvest is about 40% complete, and while some production estimates have recently been trimmed due to weather issues, it still looks like a record large crop.

Chicago corn futures are up 2 to 5 cents this morning, led by the nearby contracts. Crude oil is up strongly again this morning, adding support to the corn market. Corn futures on Monday ended fractionally to 5 cents lower in the nearbys, while deferred new crop contracts were up fractionally to 2 cents.

Export Inspections data yesterday showed US corn shipments at 1.858 MT shipped for the week ended Feb 26. That was down 8% from last week, but still the 3rd largest this year and up 37.41% from the same week last year. Mexico was the top destination of 521,921 tonnes. US marketing year shipments have totaled 39.619 MMT, which is up 42.29% yr/yr.

USDA s Grain Crushing report showed a total of just 460.95 million bu of corn used for US ethanol production in January, shy of estimates. That was a decline of 1.49% from a year ago and down 4.5% from December s revised (~5 million bu lower) total.

Traders eye the movement of fertilizer through the effectively closed Strait of Hormuz during the Middle East conflict. The maritime chokepoint moves a lot of the world’s urea, phosphate, and anhydrous ammonia that farmers use to plant corn. Disruptions of crude oil flows will cause diesel prices to rise, another key input during the upcoming planting season.

Rain forecasts for South America this week look mixed, favoring portions of northern Brazil over other areas of Brazil and most of Argentina. While many projections are still calling for a record corn crop in Argentina, some of the top end potential has likely been lost, and early conditions for much of Brazil s second corn crop are too dry.

US wheat markets are working higher this morning… Minnie spring wheat futures are up mostly 2 cents, HRW is 6 cents higher, while SRW wheat is gaining 3 to 5 cents. The US wheat complex was in give back mode on Monday, with all three markets weaker…spring wheat ending down 1 to 3 cents for the session yesterday.

The 7-day forecast is calling for less than a half inch of precip in western potions of Kansas, and the OK/TX panhandles. Eastern portions of the US Plains are seen with heavier precip totals. It won t be enough to reverse drought conditions fully, but should be generally beneficial ahead of the US crop emerging from dormancy in the very near future. USDA will release state-by-state US winter wheat condition updates later this morning.

Globally, some weather damage is likely in Europe and the Black Sea region, and Russia s war on Ukraine is having an impact on shipping in the region.

USDA s export inspections report yesterday tallied US wheat export shipments at 344,272 tonnes during the week ended Feb 26. That was 38.9% below the week prior and 11.98% shy of than the same week last year. US marketing year exports for 2025/26 are 18.62 MMT since June 1, which is now 18.82% above the same period last year.

CANADIAN GRAIN MARKET

ICE canola futures saw strong gains to begin the week on Monday as rallies in crude oil and Chicago soyoil offered support.

Crude oil climbed in the aftermath of US and Israel military strikes on Iran over the weekend, which could crimp oil shipments through the Strait of Hormuz. The advances in crude spilled over to drive gains in soyoil, which is used in the production of biofuel. On the other hand, Chicago soybeans only posted a mixed close after an early short-covering rally ran out of steam. A lower Canadian dollar added to the upside in canola, along with gains in European rapeseed. Palm oil finished mainly lower.

May canola futures rallied up $10.70 yesterday to close at $698.40/tonne, and November gained $9.80 to $701.70.

For today… canola futures are advancing another $4 to $5/tonne higher this morning, with the nearby May contract up $5.50 at $703.80/tonne…again challenging psychological chart resistance at $700. Canola and CBOT soyoil are joining the ongoing rally in energy markets, with notable significance to a charging higher world diesel market.

The gap in soyoil futures to start this week is something to watch for canola traders…something that will play a key role technically in canola’s price outlook. An exhaustion gap versus a midpoint gap has differing chartist interpretations.

Stay informed with our daily market videos. Each video quickly covers key futures moves, price trends, and market signals that matter to Canadian farmers. Get clear, timely insights in just a few minutes. Bookmark https://www.producer.com/markets-futures-prices/videos

To access the latest futures prices, go to https://www.producer.com/markets-futures-prices/

Source: producer.com