AM Market Report – November 19, 2025

ICE canola futures are following the US soy complex lower to start this morning…with the canola market mostly down $4 to $5/tonne. Chicago soybeans are leaning 7 to 9 cents/bu lower, with the products (oil/meal) also weaker.

CBOT corn futures are down 1 to 2 cents this morning.

Oilseed traders are taking some profits from recent gains…and that sell-off pressure has spilled somewhat into the corn market.

US wheat markets are mixed…Minnie spring wheat futures easing 1 to 2 cents lower, HRW fractionally mixed, while SRW wheat mixed with nearbys 2 cents higher.

Corn and soybeans are seeing modest, routine corrective price pullbacks at mid-week, amid price uptrends in place on the daily bar charts. Winter wheat bulls continue to work on restarting their price uptrends.

Looking ahead, traders will watch South America’s crop weather conditions and ongoing export news for price guidance.

In Other News

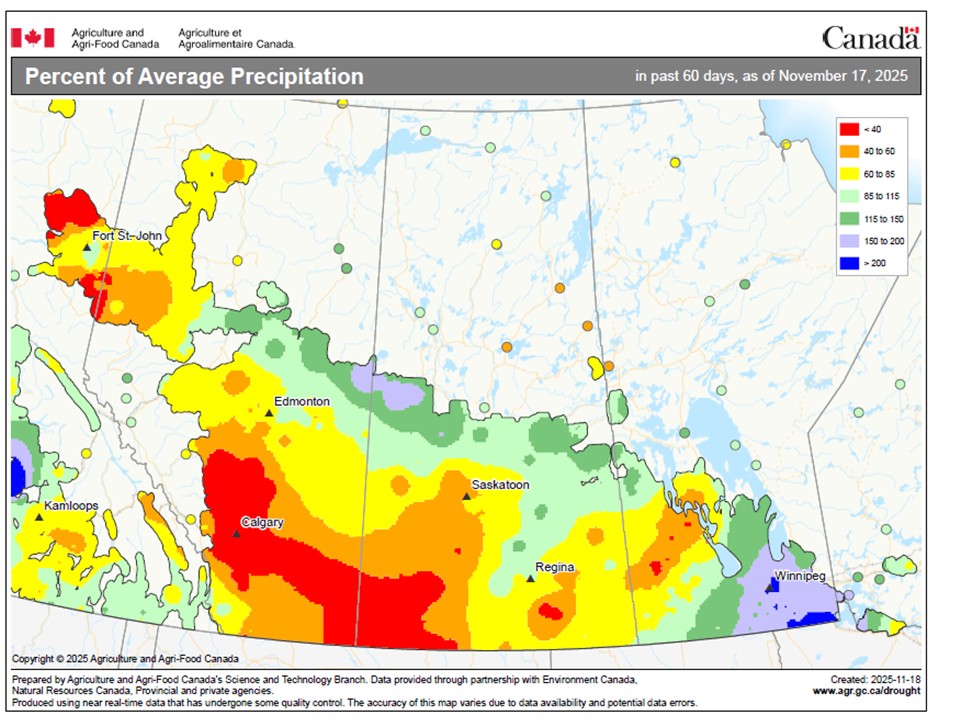

– Prairie soil moisture still short in some areas… Portions of Western Canada remain stubbornly short on soil moisture, and with temperatures set to turn sharply colder, the window for meaningful replenishment is closing fast.

According to World Weather Inc., this week marks the last stretch of milder conditions for a while, with much colder weather beginning next week. Although the transition is expected to bring some snowfall that may provide cover for winter crops and help limit frost in the ground, it will not be a fix for the driest areas, most notably the central and southwestern Prairie.

In fact, World Weather said described the odds as quite high, that those regions will come into next spring with a dry bias in the soil.

As can be seen on the map below, soil moisture across Western Canada is highly variable, with southern Manitoba quite wet, but the more western Prairie areas well below normal.

Overnight temperatures in Edmonton by next weekend are forecast to fall to around 20 degrees C, with Calgary readings dropping to around 15 degrees. The cold will eventually spread eastward, but not before Western Canada bears the brunt of the first major Arctic outbreak.

According to the latest monthly update of the Canadian Drought Monitor last week, abnormal dryness or some form of drought was impacting 68% of Prairie agricultural lands as of the end of October. That s up 4 points from September and above 59% in August but still well below 81% in July.

– Chinese, Indian tariffs take toll on pea prices… MarketsFarm s Bruce Burnett notes it all started with the Chinese tariffs on peas that were announced this past March. The tariff rate was placed at a punishing 100%, which quickly stopped Chinese purchases of peas. According to Canadian Grain Commission data, Chinese imports were 513,500 tonnes last year, which made the country the second largest importer.

India was the largest importer of Canadian peas last year at 880,200 tonnes, but that won t be the case this year now that India has announced a tariff on yellow peas that began Nov 1. The tariff of 30% will essentially price Canadian peas out of the Indian domestic market. This comes as no surprise because the Indian government has normally protected its pulse farmers with tariffs on peas, lentils and chickpeas. But this was bad news for nearby Prairie cash pea prices, which have dropped by $15 to $20/tonne since the announcement.

The disruption of pea exports from Canada s largest customers will likely result in slow pea exports for the remainder of the crop year.

The Australian pulse crop harvest is going to start over the next month and will provide additional competition for Canadian pulse exports.

The positive news for peas is that CBOT soymeal futures are setting new contract highs. This makes peas a viable alternative for the North American vegetable protein market. Unfortunately, the increase in demand will only slowly eat away at the current supply of peas in Western Canada. Until tariffs are reduced by China and/or India, the cash pea market in Western Canada will remain under pressure.

– EU wheat exports back on track after French data delays… EU soft wheat exports, which had been lagging due to missing French data, are now matching last year’s volume, European Commission data showed on Tuesday. Since the start of the 2025/26 season in July, EU soft wheat exports had reached 9.05 MMT by Nov 16, compared with 9.09 MMT at the same point last year. France was still the largest EU soft wheat exporter so far this season with 3.03 MMT, followed by Romania with 2.90 MMT, Lithuania with 1.10 MMT, Latvia with 0.58 MMT and Germany with 0.67 MMT.

The Commission said export data for France dating back to the beginning of 2024 was still incomplete. However, the fact that the French wheat export volume rose by nearly 2 MMT over two weeks suggested a catch-up.

EU barley exports also jumped, totalling 4.27 MMT compared to 3.85 MMT a week earlier and up 130% from the corresponding period of 2024/25.

The volume of corn imported into the EU so far this season had reached 6.02 MMT, against 5.60 MMT the previous week and 23% below a year earlier.

– Ukraine will not limit wheat exports in 2025/26… Ukraine will not restrict wheat exports in the 2025/26 (July-June) season due to a higher harvest and lower export tariffs rates at the beginning of the current season. Ukraine, one of the world’s leading wheat producers and exporters, has been restricting wheat exports over the past few seasons to prevent a rise in bread prices.

“According to our estimates, the wheat harvest will be around 23 MMT, and exports are expected to reach around 17 MMT (in the 2025/26 season),” says Ukraine s deputy economy minister Taras Vysotskiy. Ukraine harvested 22.6 MMT of wheat in 2024 and exported 15.7 MMT of the commodity in 2024/25.

The economy ministry data showed that the country had exported 6.8 MMT of wheat so far this season versus 8.6 MMT at the same period a season earlier.

– Farm equipment sales slump… US farm-tractor and combine sales slumped sharply in October compared to a year ago, an industry trade group reported this week. The Association of Equipment Manufacturers said US sales of agricultural tractors declined 19.6% in October 2025 compared to the year before, while combine sales decreased 26.8% during the same time frame. Through the end of October, year-to-date tractor sales were down 9.2% at 171,680 units, with combines down 38.4% at 4,970.

Canadian sales of agricultural tractors dropped 11.6%, while combines fell 17.6% in October 2025 compared to the year before, the AEM said.

The decline in sales follows a slight uptick in both Canadian and US sales in September, said Curt Blades, AEM senior vice president. However, we understand the uncertainty and volatility that remains in the marketplace, he said.

Indeed, tough times in the industry have been well documented. Creighton University s Rural Mainstreet Index s farm-equipment component has been in contraction territory, with a reading below 50.0, for 26 straight months, with survey respondents putting the blame on high input costs, tighter credit conditions, low farm commodity prices and tariff-related market volatility.

– Workers at Maple Leaf s Winnipeg plant vote for strike mandate... Workers at the Maple Leaf Consumer Foods plant in Winnipeg voted 98% in favour of a strike mandate. The 1,880 workers are members of UFCW Local 832. This union has been bargaining with Maple Leaf since February. Jeff Traeger, President and Chief Executive Officer with UFCW Local 832, said the strike vote was a first for the plant and was taken in response to Maple Leaf s refusal to take the bargaining process seriously so far.

Maple Leaf has been pushing major concessions at the table, and the union members have shown they are united and want a fair deal, he said.

The union and Maple Leaf were back at the bargaining table Monday, Nov. 17. Negotiations are expected to continue right up to the current contract s expiry on Dec. 31.

The plant produces and packages pork products, including bacon.

– Trump opens door to easing some steel and aluminum tariffs… The United States has quietly opened the door to lowering tariffs on some Canadian steel and aluminum exports…a move that stops short of the kind of relief Ottawa is pursuing, but which signals a shift in how the Trump administration is approaching trade policy. In an executive order published last month, President Donald Trump gave the US Department of Commerce discretion to lower tariffs on imports of steel and aluminum from Canada and Mexico by up to half if certain conditions are met. To get the exemption…which has the potential to lower the tariff rate to 25% from 50%…a steel or aluminum company must be expanding its production footprint in the United States, and the metal must be destined for use in US auto manufacturing.

This is much narrower than the kind of relief Canadian negotiators were seeking before trade talks with Washington broke down again last month. And to date, no companies have received the exemption. But the amendment does point to two emerging features of US trade policy: The White House is willing to lower some tariffs to address consumer and business concerns about rising costs; and the Trump administration is prepared to cut tariff deals with specific companies if they commit to expanding production in the US.

Outside Markets

The Dow Jones Industrial Average tumbled 498.50 points lower on Tuesday to settle at 46,091.74, while the S&P 500 was down 55.09 points to 6,617.32. Early Wednesday, the December Dow Jones Futures are down a very modest 2 points.

Global stock markets remain shaky this morning amid cautious trading after another sell-off driven by nerves over extended AI valuations, as investors eyed what could be make-or-break earnings from microchip giant Nvidia and US jobs data this week.

Wall Street futures are mixed this morning after major North American markets closed down hard yesterday. Canada s TSX stock index futures are trying to edge slightly higher this morning.

Nvidia, which sells the graphics processing units underpinning artificial intelligence, has been at the heart of a global rally that has carried stocks to all-time highs. It reports after the US market close today. It looks like Nvidia s stock price has been priced for perfection, so GPU demand must continue to grow strongly for many more years for the stock to stay up, said Wong Kok Hoi, founder and CEO of APS Asset Management in Singapore.

Meanwhile, Goldman Sachs president John Waldron said stock indexes are primed for possible further declines as investors await the quarterly earnings report from technology leader Nvidia Corp later today. It strikes me the market could pull back further from here, Waldron said in an interview on the sidelines of the Bloomberg New Economy Forum in Singapore on Wednesday. I do think the technicals are kind of more biased for more protection, and more downside.

The S&P 500 is down more than 3% this month, on course for its worst month since March, while volatility has surged. A sell-off in the world s largest technology companies has reignited a debate on AI, and whether it is generating enough revenue or profit to justify the massive spending on infrastructure.

Wall Street s so-called fear gauge, the CBOE Volatility Index, topped 24…above the key 20 level that causes concern for traders…and reached its highest in a month.

The December US Dollar Index is up 0.291 at 99.740. The Canadian dollar weakened against its US counterpart…currently quoted at 71.43 US cents.

Jan crude oil futures are down $1.63 at US $59.04/barrel. Oil prices are under pressure this morning as an industry report showed higher crude inventories in the United States, reinforcing concerns about oversupply…though declines were limited by a tighter fuel market because of attacks against Russian oil infrastructure.

Grain Markets

Chicago soybean futures are trading 7 to 9 cents/bu lower this morning, with the nearby contracts leading the declines. Bean futures experienced back and forth trade on Tuesday, but closed on the weaker side…down 2 to 4 cents across the front months as traders were selling the fact on Monday s Chinese purchases. Soymeal futures are down $1 to $3/ton this morning after dropping $3 to $5 on Tuesday. Soyoil futures are 46 to 60 points lower this morning after rallying 93 to 103 points higher yesterday.

Bean futures have pulled back yesterday and again this morning after reaching their highest level since June 2024 on Monday as China purchased American supplies. The USDA confirmed China purchased 792,000 tonnes of US soybeans on Monday. China previously shunned US soybeans during its trade war with US President Donald Trump and is grappling with a glut after importing cargoes from South America. Monday s purchases were the largest from the US since a summit between Trump and Chinese President Xi Jinping in South Korea last month.

While a start, Monday s China bean buy from the US seems more a token move relative to White House claims that China had agreed to buy 12 MMT of US soybeans by the end of December and 25 MMT for each of the next 3 calendar years. China was still far from that target.

The drama due to the media and politics surrounding China’s return for US soybeans has had an oversized recent impact on the market. China does not need the US soybeans; they are being purchased for political appeal at a high cost. Behind the scenes the trade expects China to secure maybe 2 to 3 MMT of US soybeans for January/February shipment, and make additional purchases of 6 to 10 MMT of summer shipment US soybeans later.

China normally will not chase a market higher for soybeans needed in the summer. A few cargoes of US soybeans for shipment off the PNW to China bought Monday are said to be for summer shipment. On the Jan/Feb soybean purchases, COFCO/Sinograin paid a $1.05 to $1.15/bu premium versus Brazilian soybeans. And that does not include the additional 10% tax that would be applied if a Chinese crusher were to make a private purchase of US soybeans. The soy premium paid reinforces that politics are behind China’s purchase. US soybeans to China are not commercially viable.

Chicago corn futures are down 1 to 2 cents this morning. The corn market posted gains across most contracts on Tuesday…closing up 1 to 2 cents.

US corn maintains a solid demand picture, but is also grappling with very large domestic supplies.

Traders are watching the tail end of the US harvest (91% completed according to USDA), along with planting and development conditions in Argentina and Brazil.

US wheat markets are trading with mixed action this morning…Minnie spring wheat futures steady to almost 2 cents lower, HRW fractionally mixed and SRW wheat mixed, but a penny or two higher on the front months. The US wheat complex also closed Tuesday with mixed action across the three exchanges…spring wheat futures up 6 to 9 cents in the nearby contracts to lead the bulls yesterday.

US winter wheat planting and emergence are behind average, with the crop in worse condition than this time last year. As of Sunday, the USDA says 92% of US winter wheat has been planted, compared to 95% normally this time of year, and 79% has emerged, compared to 84% on average, with 45% of the crop called good to excellent, 4% below a year ago. But no one is too concerned at this early stage of next year s US winter wheat crop production…especially with US wheat already priced above many other origins.

In addition to US winter wheat weather, the complex is monitoring early harvest activity in Argentina and Australia, along with winter wheat conditions in Europe, Russia, and Ukraine.

CANADIAN GRAIN MARKET

ICE canola futures ended with small gains on Tuesday, with strong advances in Chicago soyoil offering support. Malaysian palm oil was also a strong performer on the day, while European rapeseed posted more modest gains.

Reports also cited slow Prairie farmer selling as a supportive factor, as producers wait hopefully for a possible agreement with China that could see that country s prohibitive tariffs on imports of Canadian canola lifted. But no clear evidence of that happening at this time, despite more friendly ministerial talk of late.

January canola gained $1.20 to $656.40, and March was $1.90 higher at $668.60.

For today… canola future are retreating mostly $4 to $5/tonne lower this morning, scratching near the lows of the overnight session. Benchmark Jan canola remains in a short-term uptrend off its early October lower, but the contract is down $5.60 this morning at $650.80/tonne…trying to stay above recently cleared resistance at the $650 level, but so far unable to crack the next overhead target around $662 where the 100- and 200-day averages are currently converging. Still bullish technical signal…the 20-day average recent crossed up and over the 50-day…suggestive of a harvest low already made.

Related outside markets… CBOT soybean and soyoil markets are weaker this morning…as are Malaysian palm oil, EU rapeseed and crude oil futures.

On the feed grains… MarketsFarm reporter Adam Peleshaty writes that growing demand for feed grains are leading prices higher…surely but slowly…due to seasonal demand as more cattle enter Prairie feedlots. Overseas export demand for Canadian feed barley is also supporting prices.

There is a window that exporters have been taking advantage of to ship barley, principally to China, says Jim Beusekom, president of MarketPlace Commodities Ltd. in Lethbridge, Alta…adding there is enough barley to fulfill the needs of exporters and feedlots. There are no supply issues at all.

He also said cash feed barley delivered to the benchmark Lethbridge region is now selling at $265-$270/tonne, compared to $250 in August.

Other grains are also making their way into feed, including feed wheat, as well as oats, rye and triticale. Feed grains are also being augmented by an excess supply of corn across the Prairies.

When you have big crops, you have big crops of everything. It s not just canola, wheat or pulses. There s a lot of supply of everything and anything that is lower grade or cleaned out…all that clean-out ends up in feed, Beusekom said.

He added that if exports continue at their current pace, prices may be higher. However, the market is also following seasonal patterns. The seasonals on feed grains are pretty clear. Usually, the markets rally through October and November and then decline going into the latter part of winter and even into early spring, and then (they re) back up again, Beusekom said.

Delivered bids for feed barley in Saskatchewan were steady over the past month, ranging from $4.46 to $4.75/bu. In Alberta, prices ranged from $4.35 to $5.73/bu, up 13 cents this month. In Manitoba, feed barley was between $4 to $4.47/bu, up 15 cents.

To access the latest futures prices, go to https://www.producer.com/markets-futures-prices/

Source: producer.com