HALOs demostrate importance of diversifying your portfolio

The investment industry excels at creating acronyms. The newest one is HALO which stands for High Assets, Low Obsolescence. The last decade has been dominated by companies with minimal hard assets, rapidly scalable operations that generated plentiful free cash flow (cash flow minus capex, or capital expenditures), namely the technology sector, especially software.

The sentiment over the past six months has changed dramatically with concerns of artificial intelligence (AI) obsoleting other tech companies and industries. Nothing has taken it on the chin as much as the software industry. Most of the largest software companies have declined 25–50 per cent, while overall markets have been stable to increasing. The entire technology sector, including last year’s Magnificent Seven (Mag 7), has been flat to declining although the Mag 7 remains humungous relative to other companies.

Over the past couple of years, this narrow group of companies dominated the price appreciation of the S&P 500, with many of the other 493 holding back its overall performance. Today, two-thirds of 500 are outperforming the market while technology is holding the index back — which is great for those of us with widely diversified portfolios.

Read Also

How to develop a leader’s mindset at every stage of your career

Leadership looks different at every stage of your farm career. And the stories you hear, the ones you seek out or the ones you tell yourself all effect how you lead.

As money comes out of tech, it’s going into long-forgotten sectors defined by those that are capital intensive, high assets that AI cannot make obsolete. Energy, pipelines, utilities, mining and industrials fit that definition, and thankfully energy is no longer considered to be declining towards obsolescence.

Money is also moving internationally with the five international ETFs I mentioned in two articles last summer (“Where in the world are the best opportunities?” and “It appears I am not alone”), up from 13–40 per cent plus dividends in a short six to eight months.

Canadian market performance has benefited from this sector shift rising 8.3 per cent in the first two months of the year, while U.S. indices are flat and this despite our economic performance being the worst of the G7 and the only country with negative GDP in the fourth quarter of 2025.

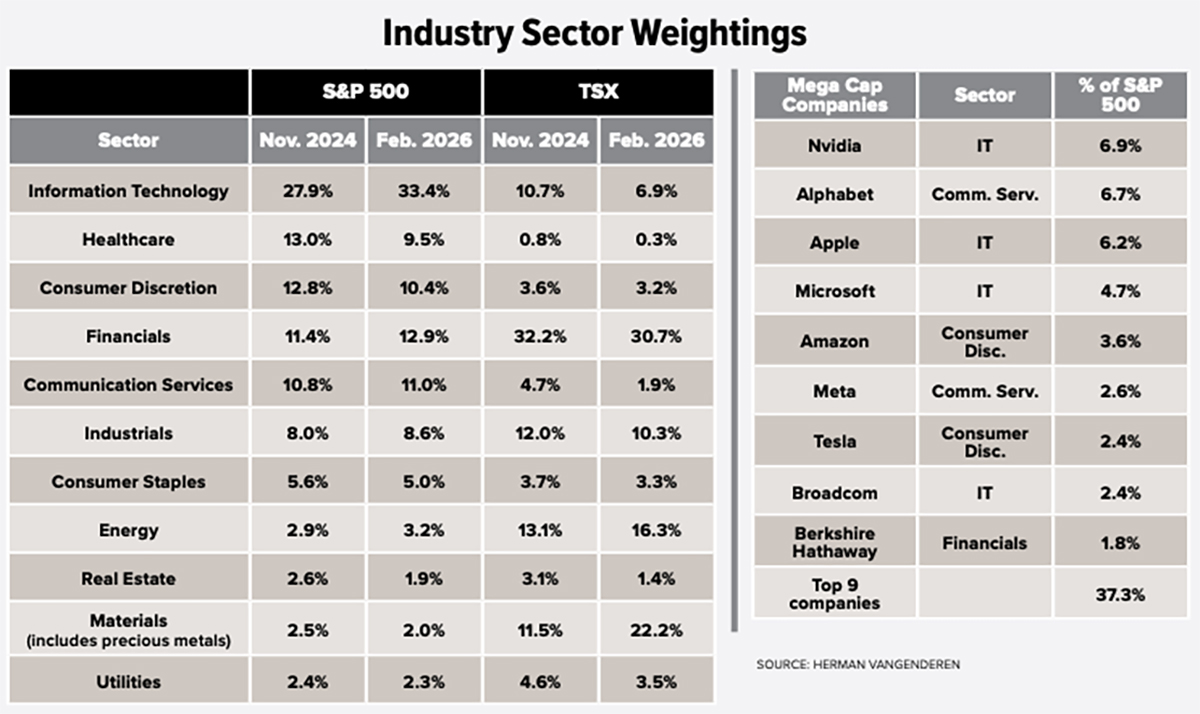

The market is broadly divided into 11 different sectors. I first put this chart (see Industry Sector Weightings in sidebar) together in November of 2024 and found it interesting to see how weightings shifted over time. In the U.S., despite the current sell-off, information technology is still up significantly from late 2024. Health care is down and the rest of the industries are relatively stable. The picture in Canada is quite different, with Materials (mostly mining) doubling its market weight and energy is up appreciably. Our small IT sector is down mostly because of two former market darlings, Constellation Software and Shopify.

Additionally, I included weightings of the nine largest U.S. companies to illustrate how dominant they remain despite their recent softness. All are down in 2026 except Berkshire, the only one I consider a non-tech company, although some are officially in other sectors.

Nvidia, with a market cap of $4.3 trillion after its recent 15 per cent decline, is still as big as the entire Canadian TSX market cap. It is also as big as the entire North American Energy and Materials sectors combined. Alphabet and Apple are similar in size. I would suggest that energy and minerals are significantly more important to our welfare than AI chips.

Except for Tesla, none of the mega caps are ridiculously valued if they continue to grow, making it hard to know whether the capital shift will continue. If it does, the sheer amount of money represented by technology — if moved to a smaller sector — could set off significant fireworks. At the end of the boom in 2008, the energy sector represented 15 per cent of the S&P and 30 per cent of the TSX.

Personally, I try to have both a U.S. and a Canadian company from each sector in each portfolio. That creates broad diversification. It means I never entirely miss any boat, nor do I catch each big wave. I buy fairly valued companies in sectors currently out of favour, holding for a long time while patiently waiting for their day in the sun. For example, I have owned Kinross Gold for a decade, as it did nothing except pay a small dividend. In the last two years it is up 500 per cent. That’s not just exceptional performance over two years, but pretty darn good even over a decade. As mentioned, I recently added international ETFs to this strategy.

Investors that focus on the current hot sector will miss many sector boats as they set sail. Like market tops and bottoms that nobody calls regularly, it is also difficult, if not impossible, to predict when an out of favour sector will leave the dock and set sail.

Source: producer.com