AM Market Report – May 4, 2026

GOOD MORNING…HERE IS YOUR MORNING MARKET NEWS

OVERNIGHT GRAIN TRADE

ICE canola futures trended lower to start the overnight session, then steadily build to slightly positive price action…now steady to almost $2/tonne lower this morning.

Chicago soybean futures are posting gains of 3 to 6 cents/bu this morning (6-week high), with the meal and oil byproducts slightly higher. Bean futures are working the higher end its sideways range and were threatening to break above $12.00/bu in the July contract. Bean oil is hitting another fresh contract high this morning.

Read Also

Prairie Weather

The cold front that swooped through the Prairies on the weekend brought some scattered light precipitation to the eastern…

CBOT corn futures are down 1 to 2 cents this morning.

US wheat markets are weaker on more profit-taking from last week off their 2026 highs… Minnie spring wheat futures are losing 6 to 7 cents this morning, HRW is 8 to 9 cents lower and SRW is down 3 to 6 cents.

Latest on the war in the Middle East…

Crude oil prices are higher this morning following reports that two missiles struck a US warship after it ignored Iranian warnings. But news agencies could not independently verify the report. The US has denied any of its ships have been attacked.

Meantime, a fresh plan announced by US President Donald Trump to help escort commercial vessels through the Strait of Hormuz has left shipping executives perplexed, as attacks continue and traffic remains at a near standstill, Bloomberg reports. Trump said Project Freedom will see the US guide ships trapped in the Persian Gulf safely out of these restricted Waterways, so that they can freely and ably get on with their business. No further details were announced.

The head of the Iranian parliament s National Security Commission, meanwhile, has already responded that US interference in Hormuz would constitute a violation of a fragile ceasefire in place since last month. And Iran has doubled down by declaring that they will attack anyone trying to pass through the Strait of Hormuz…and has followed that up with a variety of attacks designed to send a message to ship owners and insurers that Trump’s plan is not to be trusted.

Iran s latest proposal to the United States wants issues between them to be resolved within 30 days and aims to end the war rather than extend the ceasefire, according to Iran s state-linked media. Officials reiterated these were not nuclear negotiations. Trump on Saturday said he was reviewing the proposal but expressed doubt it would lead to a deal. Clearly, US negotiations with Iran are not progressing smoothly.

In other war news… Ukraine launched drone attacks across Russia on Sunday, hitting the Baltic Sea port of Primorsk, stepping up attacks on energy infrastructure.

In Other News

– Broad commodity inflation cycle developing… An energy-led commodity rally broadened out in April, with grain market bulls looking to money flows to provide a continued tailwind for agricultural commodities. Grain and oilseed markets have caught the energy market s coattails, with soyoil futures notching another round of contract highs, canola tapped contract highs last week, while corn grinds higher. Wheat has broken out to trade at nearly two-year highs, aided by a war premium, but driven largely by the persistent drought and deteriorating crop conditions in the US Plains (HRW country). The fertilizer crunch also plays a role, with producers around the world seen trimming plans for wheat and corn acres.

But producers also face an intensifying squeeze as diesel prices ratchet higher and surging fertilizer prices further squeeze margins from the input side.

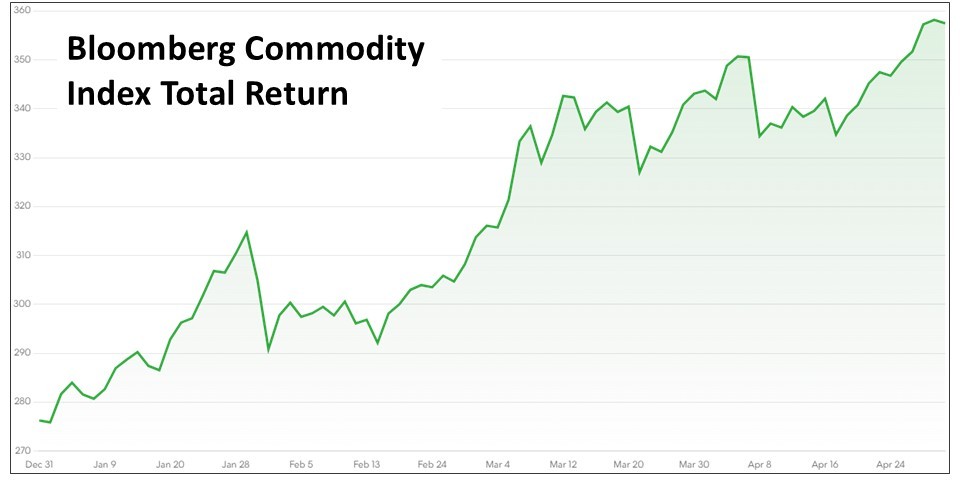

The Bloomberg Commodity Total Return Index delivered a 4.2% monthly gain in April, noted Ole Hansen, head of commodity strategy at Saxo Bank. That brought the index s year-to-date return to 30%, with all sectors except precious metals posting positive returns.

Energy remained in the driver s seat, as oil and fuel prices pushed to new highs in late April on expectations for a lengthy closure of the Strait of Hormuz. The energy sector rose 7.7% in April, following a 40.7% March rise that s left it higher by 74% year to date.

Top individual performers included Brent crude, cotton, gasoline, diesel and soybean oil, while gains in wheat and copper highlighted how support is broadening beyond the hydrocarbon sector, Hansen said, in a note to clients. In many ways, April marked the clearest sign yet that what began as an oil shock is developing into a wider commodity inflation cycle, driven by supply-chain disruption, rising transport costs, fertilizer shortages and growing uncertainty around monetary policy and currency markets.

The Bloomberg Agriculture Spot Index has broken out to trade at its highest since November 2023, but remains well below its 2022 peak. Hedge funds have increased their long exposure to ag complex futures.

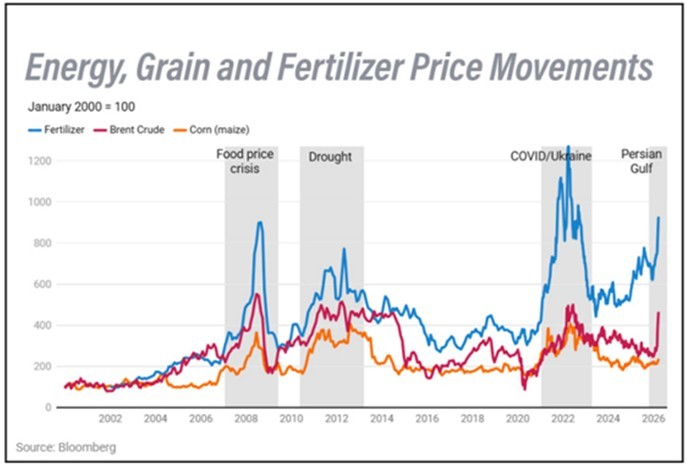

The chart below comes from the International Food Policy Research Institute report by economists Shawn Arita and Joseph Glauber, illustrating how past agricultural price spikes, including 2007-08, 2010-12 and 2021-22, saw energy, fertilizer and corn prices move together.

Past supply shocks offered attractive, long-term marketing opportunities. Producers should be ready to reward rallies and stay nimble, because the speculative floor for the market can drop out just as quickly as it can rise.

– China companies told to ignore US sanctions… China has ordered its companies to ignore US sanctions, an unprecedented act of defiance that threatens to trap a vast banking sector in the crossfire as tensions rise between the world s two largest economies, Bloomberg said in a report. Beijing has often railed against unilateral sanctions and pronounced them illegitimate, but it has also quietly allowed its largest companies to comply with them, in order to avoid blowback on its own economy and to preserve access to the US financial system, said the report.

But Saturday s announcement…coming before a long-awaited meeting later this month between President Donald Trump and his counterpart Xi Jinping…signals a far more aggressive Chinese stance. Beijing has now directed companies not to abide by US sanctions on private refiners linked to the Iranian oil trade, including heavyweight Hengli Petrochemical (Dalian) Refinery Co. which was sanctioned last month.

– Europe ready to respond to any new US tariffs... Europe is ready to respond should US President Trump follow through on his threat to raise tariffs on cars and trucks from the European Union to 25%, according to Eurogroup President Kyriakos Pierrakakis and as reported by Bloomberg. The number-one choice is always dialogue…we want to be a predictable partner in the international economy, we believe in the transatlantic relationship, he told Bloomberg Television. But having said this, if there is a deviation from what we have agreed upon, obviously all options are on the table, and all choices will be on the table.

– Canada canola crush rebounds in March… After dipping below 1 MMT for the first time in the 2025-26 marketing year in February, the Canadian canola crush rebounded in March. Statistics Canada pegged the March canola crush at 1.097 MMT, up a hefty 15.3% from February s 951,353 tonnes, and 7.1% above the same month last year. The year-to-date 2025-26 crush (August to March) now stands at 8.163 MMT, 4.1% above the same period a year earlier. As of the end of March, the cumulative crush for the current marketing year represented 68% of Agriculture Canada s full year projection of 12 MMT…nearly identical to the previous year when the crush totaled a record 11.412 MMT.

In its April supply/demand update, Agriculture Canada left its 2025-26 canola crush forecast unchanged from March at 12 MMT, but lifted its new crop crush outlook by 500,000 tonnes to a new high of 13 MMT.

Earlier this month, Cargill announced that its long-awaited canola processing plant in Regina is now up and running. The plant is expected to process up to 1 MMT of canola annually. According to the Canola Council of Canada, domestic canola processing capacity across the country is expected to reach 15 MMT in 2026, a 40% increase from 2020.

– US biofuel test… US companies that turn soybeans into biodiesel will need to boost production by 60% this year to meet record biofuel blending targets set by the US Environmental Protection Agency…a target that industry groups and experts warn could prove unreachable, Reuters reported, noting that failure risks stoking a further rise in diesel prices.

The EPA set biodiesel and renewable diesel volume requirements of 5.4 billion gallons for 2026 and 5.7 billion for 2027, up from 3.35 billion last year. Factoring in exports and other considerations, EPA estimates that hitting the new obligations will require a supply of 6.07 billion gallons this year, the report noted.

– US soybean crush, corn for ethanol use larger than last year… Strong demand continues to drive the US domestic soybean and corn crushes. The USDA says 227 million bu of soybeans were crushed in March 2026, a little bit below pre-report expectations, but still up 13 million from February and 20 million from March 2025. Soybean meal and oil stocks were both below a month ago because of demand, but above a year ago due to higher production.

474.434 million bu of corn were used during March to make ethanol in the United States, generally in-line with estimates, rising 10% on the month and 5% on the year.

– India begins wheat exports after four-year hiatus... Indian traders have begun exporting wheat for the first time in four years, as a bumper harvest and a rally in global prices and freight rates make shipments of the staple competitive for buyers in Asia and the Middle East, trade sources told Reuters. Consumer goods conglomerate ITC has started loading 22,000 tonnes of wheat at the western port of Kandla for shipment to the United Arab Emirates. India, expecting a record crop, has allowed exports of wheat this year following a 2022 ban. It extended the curb in 2023 and 2024 after extreme heat shrivelled the crop and depleted stocks, leading to record domestic prices, fuelling speculation it might need to turn to imports for the first time since 2017.

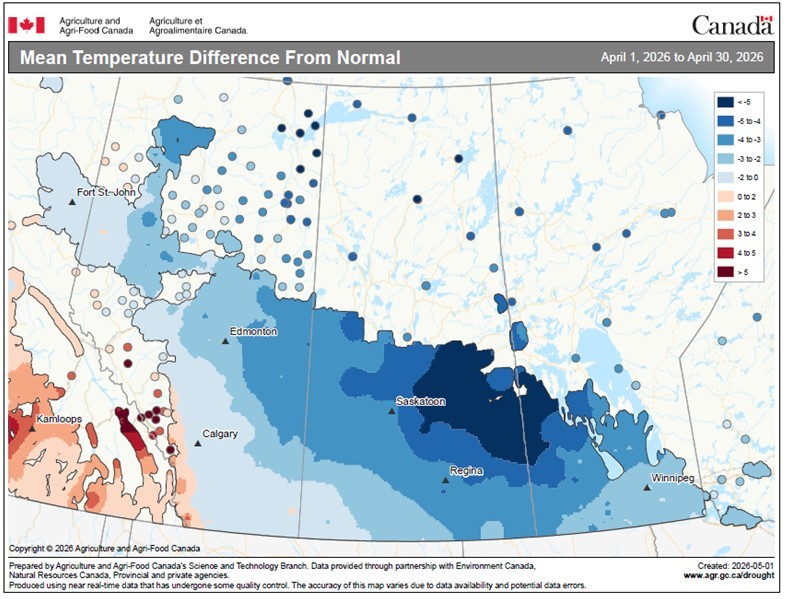

– April brings uneven precipitation; cooler temps to Western Canada… April weather across Western Canada delivered a mix of cooler-than-normal temperatures and uneven precipitation, creating a patchy start to spring seeding preparations across the Prairies.

Temperature data show much of Alberta, Saskatchewan and Manitoba experienced below-normal readings through late April, with some areas running 3 to 5 degrees Celsius colder than average. The coldest conditions were centred over central and eastern Saskatchewan, where a persistent chill slowed soil warming and delayed early field activity.

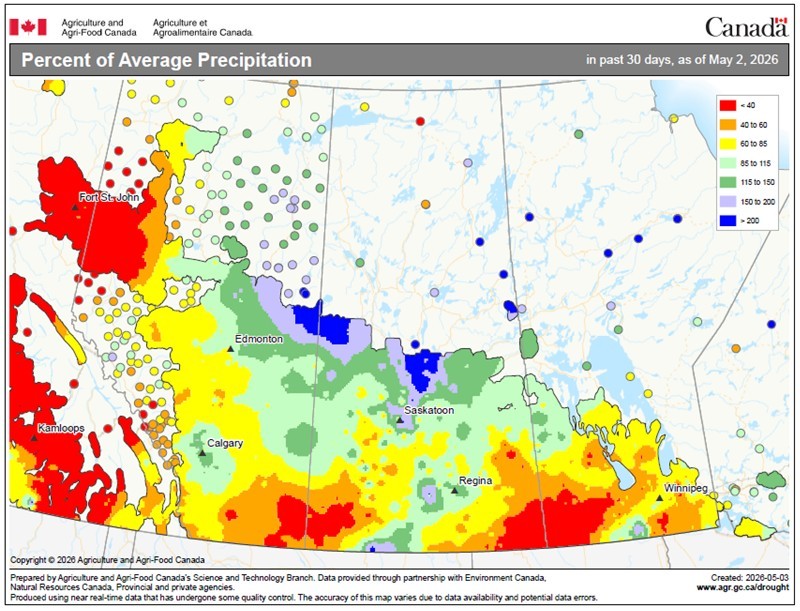

Precipitation patterns were far less uniform. Parts of central Saskatchewan and northern Alberta received near to above-average moisture, with localized pockets well above normal. In contrast, southern Alberta remained notably dry, with some regions receiving less than 60% of average precipitation over the past 30 days. Southern Manitoba also saw mixed conditions, with drier pockets emerging alongside areas of heavier rainfall.

In drier regions, especially southern Alberta, moisture deficits remain a concern heading into planting, raising the risk of uneven emergence if timely rains do not materialize.

Weather across the Canadian Prairies over the next week is expected to remain somewhat unsettled, with a gradual transition toward warmer temperatures after the recent cold stretch. Early in the period, lingering cool air…especially across Saskatchewan and Manitoba…will keep soil temperatures below ideal levels, potentially slowing germination for early-seeded crops. However, forecasts point to a warming trend developing by mid- to late-week, which should help accelerate field activity.

Precipitation will be mixed, with scattered showers moving through parts of Alberta and Saskatchewan, while some southern areas may remain on the drier side.

– June tipping point for energy markets… The crude oil market is four weeks from a tipping point that would see prices shoot significantly higher, traders warned in a Financial Times report, as the shutdown of the Strait of Hormuz continues to draw down global stockpiles. Traders and analysts cited in the report warned that global stocks of crude oil, gasoline, diesel and jet fuel will fall to critically low levels by the end of May, which would be followed by a rapid escalation in prices.

We do not have months, Frederic Lasserre, head of research at Gunvor, one of the world s largest oil traders, told the FT. It goes beyond gasoline at the pumps to industry shutting down and you enter recession. The tipping point is clearly June…this is the point at which something has to give.

Contrarian view: Phil Flynn of Price Futures Group argues in a Friday note that a case can be made that there s more risk to the downside than the upside for the crude oil market. He contends that while headline risk has kept a floor under prices, the lack of actual full closure or major new incidents has allowed crude to stabilize rather than run away to the upside. If US President Trump greenlights new military action, Brent crude oil could surge back to the $120-$130 a barrel zone in a heartbeat, he acknowledged, but until then the market is pricing in maximum pressure that is delivering pain to Tehran. Any signs that Iran comes to their senses, then oil could crash to fill the Iran war gap on the charts, he wrote.

Outside Markets

The Dow Jones Industrial Average finished Friday down 152.87 points at 49,499.27, but the S&P 500 edged up 21.11 points to 7,230.12. Canada s S&P/TSX composite stock index slid 73 points lower on Friday to close at 33,891.

Early Monday, the June Dow Jones Futures are down 189 points. Global stock markets are generally weaker this morning amid the continued impasse in the Middle East as Iran warned US forces not to enter the Strait of Hormuz after Us President Trump s offer to guide ships stranded there.

The June US Dollar Index is up 0.185 at 98.190. The Canadian dollar weakened against its US counterpart…currently quoted at 73.52 US cents.

June crude oil futures are up $0.43 at US $102.37/barrel. Oil prices are edging up as Iranian state TV reported that country s navy said it prevented the entry of US warships in the Strait of Hormuz area.

The broader market remains tightly supported by persistent supply disruptions and geopolitical uncertainty, said Priyanka Sachdeva, analyst at Phillip Nova. Unless there is a clear and sustained resolution that restores normal flows through the Strait of Hormuz, oil prices are likely to remain elevated, with risks still tilted toward further upside.

Grain Markets

Chicago soybean futures are trading 3 to 6 cents/bu higher this morning, led by the front month contracts. Bean futures are working the higher end its sideways range and were threatening to break above $12.00/bu in the July contract. Bean futures closed Friday s session with 5 to 12 cent gains, as July was 23 cents higher last week.

Soymeal futures are steady to $1/ton higher this morning after finishing Friday steady to $2/ton higher. Soyoil futures are up a modest 3 to 12 points right now after closing 29 to 93 points higher on Friday, with the July contract rallying 383 points higher last week to fresh contract highs.

Commitment of Traders data showed speculators in CBOT soybean futures trimming 7,602 contracts from their net long position as of April 28, taking their net long position to 185,282 contracts. Bean oil extended their record net long by 281 contracts to 165,725 contracts.

USDA s monthly Fats & Oils report from Friday afternoon showed March US soybean crush at 227.36 million bu, shy of the 231.1 million bu estimate. That was still 6.15% above February and 9.98% above the same month in 2025. US marketing year crush since Sept 1 is now 1.651 billion bu, up 8.5% from the same period last year. US soyoil stocks were tallied at 2.456 billion lbs.

US soy planting conditions generally look favorable into mid-month. There are some areas of concern, but again, on the balance, the trade expects US soybean planting to remain at a record pace. The USDA s weekly national crop progress and condition numbers are out Monday afternoon.

Chicago corn futures are easing down a penny or two this morning. The corn market posted gains of 1 to 5 cents across the board on Friday, with July rallying 16.75 cents on the week.

Monthly US Grain Crush data from USDA showed 474.4 million bu of corn used in ethanol production in March. That was a 10.2% increase from February and 4.76% larger than last year. US marketing year US corn grind since Sept 1 has totaled 3.225 billion bu, now 20 million bu above last year in the same period.

Weekly CFTC data showed managed money adding 79,697 contracts to their net long position in CBOT corn futures in the week ended April 28. That took their net long back to 264,103 contracts.

Planting weather looks generally good for most of the US Corn Belt. Still, portions of the region were missed by recent rainfall, other areas got excessive precipitation, and some areas will see cooler near-term temperatures, possibly inhibiting early development.

Export demand for US corn remains solid, but Argentina s prices are falling as their record harvest moves forward, which could cut into the US advantage. Parts of Brazil s second crop corn growing areas need rain.

US wheat markets are weakening this morning, trimming back from the highs posted mid-week last week…leaving bearish candles on price charts. This morning…Minnie spring wheat futures are down 6 to 7 cents, HRW losing 8 to 9 cents and SRW wheat off 3 to 6 cents. Last week…July spring wheat futures finished 10.75 cents higher at $7.04/bu, but off the week s high close of $7.15. July is down 7.75 cents this morning at $6.9625.

Last week we saw old crop CWRS 13.5 wheat bids hit as high as $8.90/bu with CPS not that far behind.

The quarterly US Flour Milling report from USDA showed a total of 222.4 million bu of wheat ground for flour in January through March, a 4.2 million bu drop from the same period last year.

Despite the rain in this week’s forecast for the US Plains states, the market feels less confident of a turnaround in US HRW wheat crop ratings. Any scattered precipitation might be too little, too late for part of the US HRW crop. Soft red winter conditions are comparatively good, but some areas might have too much soil moisture. Traders are also monitoring North American spring wheat planting.

Globally, wheat crops in the EU, the Black Sea, and India look favorable, while those in the US, Canada, and Australia are expected to be lower in 2026-27.

World supplies are ample and the recent price rally might have priced US wheat out of the export market, except for some of the usual buyers.

CANADIAN GRAIN MARKET

ICE canola futures declined on Friday, following the crude oil market lower. Crude oil futures were volatile but ultimately lower on Friday, as prices pulled back from recent highs amid shifting geopolitical signals.

Proft taking on Friday after recent gains also weighed on canola, while advances in Chicago soybeans and soyoil helped limit the downside.

July fell $7.50 on Friday to close at $756.30/tonne, and November dropped $3.10 to $758.20.

For today… canola futures have see-sawed between small gains and losses through the overnight session, but are currently posting $1/tonne declines. Benchmark July canola futures are down $1.70 right now at $754.60/tonne…still holding above resistance now turned support at $750. July canola last week gained $14.10/t.

Soyoil futures trade seems a little shaky this morning, but are holding modest gains at fresh contract and 3.5 year highs as US biofuel demand accelerates amid the developing global energy crisis. EU rapeseed futures are trading higher this morning and at new highs for the Jan-April rally period.

Persistent bean oil strength has pushed calculated ICE canola crush margins to a fresh record high last week at $382.62/tonne according to exchange data, compared to $330.68/t a month ago and $107.99/t a year ago. The $6.23/bu improvement in gross canola crush margin versus last year would certainly suggest the domestic crush sector runs flat out.

Biofuels are a structural bull story for oilseed and vegoil markets. Canola price charts are technically still trending higher…but watch for potential double top signals ahead of spring planting.

Lentil prices moving up and down

Green and red lentil prices are going in opposite directions. David Nobbs of Harvest Grain in Saskatoon says current small green lentil prices are staying put or moving lower because demand is traditionally front-loaded as crops in Europe, Morocco, Mexico and the United States enter the market. He added that large green lentil prices are two to three cents per pound off their seasonal highs. However, red lentil prices are making gains and there could be more room to the upside.

Traders are kind of positioning themselves for stronger Indian demand and El Ni o potentially hurting the predicted crop. But the big issue is that Canada and Australia have big stocks, he said. We have markets inching up a bit, but I d like to say it (won t be for) a significant period just because of the sheer volume (for carryout).

Delivered bids for Laird and Eston green lentils ranged from 12 to 25 cents/lbs as of the end of April, with monthly price movement at a loss of 1.5 cents to a gain of 0.3 cents/lbs. higher quality red lentils were priced at 25 to 26 cents, steady to up 2 cents.

Statistics Canada projects a heavy carryout of 1.57 MMT of lentils at the end of the 2025-26 marketing year, nearly triple the amount from the year before. The ending stocks for 2026-27 are expected to be similar with total seeded lentil area at 4.13 million acres. The figure is slightly less than in 2025, but Nobbs said high fertilizer prices could yet convince growers to add more pulse acres.

I see acres moving in and out, he said, adding there could be a shift towards growing more red lentils and less greens. I think the StatCan (projection) is probably right.

Stay informed with our daily market videos. Each video quickly covers key futures moves, price trends, and market signals that matter to Canadian farmers. Get clear, timely insights in just a few minutes. Bookmark https://www.producer.com/markets-futures-prices/videos

To access the latest futures prices, go to https://www.producer.com/markets-futures-prices/

Source: producer.com