AM Market Report – April 28, 2026

GOOD MORNING…HERE IS YOUR MORNING MARKET NEWS

OVERNIGHT GRAIN TRADE

ICE canola futures are trading $3 to $4/tonne higher so far this morning. But Chicago soybean futures are mostly fractionally to 2 cents/bu weaker…soymeal slightly higher and soyoil slightly lower. The bean market remains trapped in a sideways trading range. Anticipation builds ahead of next month’s US-China trade summit.

CBOT corn futures are mainly 2 to 4 cents higher this morning. Corn is seeing gains amid concerns high fertilizer prices will see some producers limiting applications and thus reducing yields.

Read Also

AM Market Report – April 27, 2026

GOOD MORNING…HERE IS YOUR MORNING MARKET NEWS OVERNIGHT GRAIN TRADE ICE canola futures are trading slightly higher so far this…

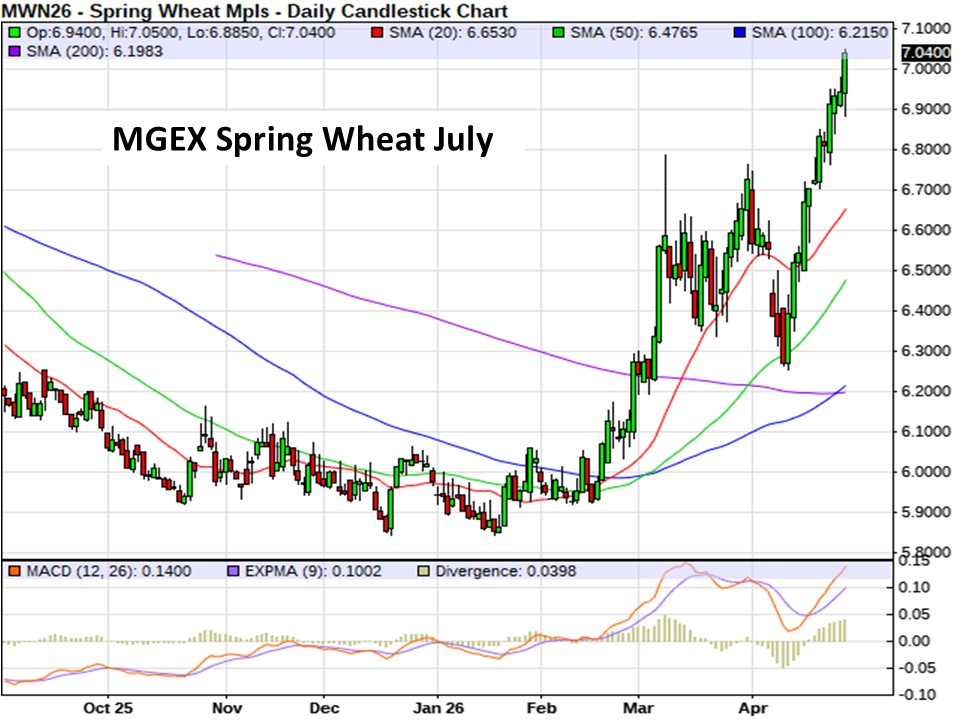

US wheat markets are the leading bullish light of the grain markets today so far… Minnie spring wheat futures are up 7 to 9 cents (22-month high), HRW rallying 12 to 15 cents higher (2-year high) and SRW wheat gaining mostly 10 to 11 cents (7-week high). Wheat futures are attracting more speculator buying interest amid drought conditions in parts of US HRW wheat country.

US corn and soybean planting made solid advances over the past week. Large parts of the US Midwest saw heavy rainfall, but only a handful of states experienced a significant lag linked to that weather, and the precipitation did miss some key growing areas. The USDA says 25% of US corn is planted and 7% has emerged, both ahead of the five-year averages. 23% of soybeans are planted and 8% has emerged, also both ahead of average.

30% of US winter wheat is rated good to excellent, unchanged on the week. Analysts had expected a slip to 29%, reflecting drought conditions and possible freeze damage to the hard red winter wheat crop in the US Plains.

19% of spring wheat is planted, a little slower than usual, and 5% has emerged, just ahead of the typical pace. Spring wheat planting progress was particularly slow in Minnesota and the top production state of North Dakota.

Latest on the war in the Middle East

US leaders say Iran’s latest offer to stop attacks on ships in the Strait of Hormuz in return for an end to the conflict is sketchy. Under the deal, nuclear talks would be put on hold. US President Donald Trump convened his national security team to discuss Iran s proposal to end a war now entering its third month.

Iran has signaled it may be willing to accept an interim deal to reopen the Strait of Hormuz in exchange for Washington ending its blockade of Iranian ports, while postponing more complex negotiations over the country s nuclear program. It is insisting on keeping some control over shipping through the strait, which Washington is unlikely to accept. Reports said Trump told his advisers he s not satisfied with Iran s latest suggestions.

In Other News

– Canada won’t be ‘chasing a small deal’ to get US tariff relief… Prime Minister Mark Carney says Canada and the US could resolve the ongoing tariff dispute within “days” if the US side had the “bandwidth and the inclination to go through with it.” The US has maintained hefty import levies on a number of Canadian goods including steel, aluminum, copper, some automotive parts, lumber and other wood products.

Carney told CBC News yesterday that the Canadian side is ready to work on a deal that would see some of those tariffs lifted, but added he’s not interested in quickly achieving a small deal. “We need a good deal in the right time, and what we don’t need is chasing a small deal that disadvantages us,” the Prime Minister said. Carney went on to suggest that a good tariff resolution could be reached soon, but that there needs to be more movement from the US side of the table. “It takes two to negotiate it through, and they’re not all the way there.”

In the CBC interview, Carney suggested countries that quickly worked out some form of tariff relief with the US aren’t happy with the deals they got. A number of countries such as the UK, Japan and the EU block reached agreements with the US within the last year, but those deals kept some form of tariff on imports to the US. “A lot of countries rushed into deals with the US. They weren’t really worth the paper they were written on,” Carney said.

– Americas crop updates from Cordonnier… Note crop consultant Dr. Michael Cordonnier s weekly corn and soybean crop perspective and commentary:

US corn, soybean acreage The eventual corn acreage may decline 1-2 million acres due to high fertilizer prices and dry conditions in the mid-South, the southeastern US, and parts of the far western Corn Belt. Due to an anticipated slight reduction in fertilizer applications, especially in the fringe areas, the 2026 US corn yield is estimated between 180 to 182 bu/acre. The eventual soybean acreage may increase 1-2 million acres due to switching from corn and potentially other crops due to fertilizer prices and dry conditions. Soybeans are not as sensitive to reduced fertilizer applications as corn, so a slight reduction in fertilizer applications may or may not impact yields. The 2026 US soybean yield is estimated at 52.0 bu/acre.

The 2025/26 Brazil soybean estimate was left unchanged this week at 179.0 MMT, with a neutral bias. Soybean harvesting in Brazil approached mid-90s percent last week. The 2025/26 Brazil corn estimate was left unchanged this week at 134.0 MMT, with a neutral bias.

– Russian wheat export prices steady second week in a row… Russian wheat export prices remained steady for two consecutive weeks as cold weather delays the start of the sowing season, although the impact of the recent sharp drop in temperatures on winter crops is not yet clear. The price of Russian wheat with 12.5% protein content for free-on-board (FOB) delivery in May was US $237/tonne at the end of last week, unchanged from the previous week, said the IKAR consultancy. IKAR downgraded the export estimate this month to 3.8 to 4.0 MMT from 3.8 to 4.2 MMT a week earlier.

SovEcon expects prices for Russian wheat with 12.5% protein content at $239 to $241/tonne compared to $237 to $239 a ton FOB ? week before. The agency left its export forecast for April unchanged at 4.0 MMT.

Cold weather in Russia has led to a significant delay in the pace of spring sowing, Agriculture Minister Oksana Lut said last week. IKAR agency has lowered its forecast for the 2026 wheat harvest by 1 MMT to 90 MMT, against the backdrop of difficulties with the sowing campaign across Central and parts of Volga districts. As of today, the agency’s analysts estimate the delay in spring field activities to be three weeks. SovEcon, on the other hand, has raised its forecast for the 2026 wheat harvest by 2.1 MMT to 89.7 MMT last week, citing favourable weather and improved prospects for winter wheat.

It is currently difficult to assess the impact on winter crops of the cold snap that hit at the end of April, mainly in the central regions of the country, IKAR said.

– EU crop monitor raises grain outlook… The European Union’s crop monitoring service MARS on Monday lifted its outlook for this year’s grain yields, pointing to broadly favourable growing conditions, but warned of persistent low rainfall in some parts of the bloc. MARS projected the EU’s soft wheat yield at 6.05 metric tons per hectare (t/ha), up from 5.98 t/ha forecast last month. That was 4% below the yield in last year’s harvest but 3% above the five-year average.

“Crop conditions across Europe remain generally favourable as the season progresses, supported by mild temperatures and adequate soil moisture in many regions. Winter crops are developing under mostly good conditions, while spring sowing campaigns are advancing across much of the EU,” it said. Persistent low rainfall across central, northern and eastern Europe since March is stoking concern as crops begin drawing more heavily on water supplies in spring, but soil moisture levels remain adequate for now, MARS said.

In contrast, excess rainfall in southwestern and parts of eastern Europe has triggered localized waterlogging, and brief cold snaps may have caused limited damage on crops in some areas, it said.

For winter barley, the overall EU yield was estimated by MARS at 5.23 t/ha, up from 5.13 t/ha forecast last month but 8% below 2025. In its first projection for spring barley, MARS pegged the EU yield at 4.96t/ha, up 4% on the five-year average. For rapeseed, MARS projected the EU’s 2026 yield at 3.25 t/ha, up from 3.22 t/ha last month.

– The cost of supply chain disruptions... MarketsFarm reporter Glen Hallick writes that a new economic analysis from the Agriculture Transport Coalition found a single week of rail and port disruptions during peak export season costs Canada s grain sector up to $540 million, largely in unrecoverable export sales. The ATC analysis examined the economic impact of labour disruptions across rail and port operations during peak grain export periods and found that losses compound rapidly and fall disproportionately on farmers and exporters, with missed sales that cannot be recovered once shipments are delayed.

The coalition released the findings on April 27 as part of Too Much on the Line, its national campaign calling on the federal government to reform Canada s labour relations framework and reduce the risk of future supply chain shutdowns. The coalition is encouraging Canadians to visit KeepGrainMoving.ca and send a letter to their Member of Parliament, adding that participation in the federal consultation process is critical to ensuring government decisions reflect the economic realities of Canada s grain supply chain.

Every time grain stops moving, the consequences are immediate and unrecoverable, said Bruce Burrows, executive director of Grain Growers of Canada. Missed sales, broken contracts, and a reputation as a reliable supplier that takes years to rebuild. Canada cannot keep accepting this as the cost of doing business. There is simply too much on the line.

The ATC said the grain sector is uniquely exposed. Canada exports over 70% of its grain production, with 94% moving by rail. The analysis found that even the threat of disruption triggers losses, with up to $112 million in missed sales occurring before a work stoppage begins.

The findings come against the backdrop of the unprecedented dual railway stoppage in 2024, which brought grain shipments to a halt and cost the sector millions of dollars per day. Repeated disruptions have raised questions about Canada s reliability as a global supplier at a time when agricultural exports are central to economic resilience.

– Prediction markets firm Kalshi adds commodity hub… Kalshi has launched a new commodities hub on its prediction markets platform. Commodities have become a hot topic due to the conflict in the Middle East and the closure of the Strait of Hormuz, said company spokesperson Jack Such.

Prediction markets are a form of futures markets. But instead of trading on the underlying price of certain goods, they trade on whether or not an event will occur, he said. They provide investors with binary (yes/no) options on a variety of topics such as whether somebody will win an election or an Oscar or in the case of commodities, whether the price of wheat will be above a certain amount on a certain date.

They differ from gambling sites, where people bet against the house. We re much like the CME (Chicago Mercantile Exchange) or ICE (Intercontinental Exchange) in the sense that we are simply the exchange, a platform connecting buyers and sellers, said Such.

Seventy per cent of the platform s users have never deposited any money into Kalshi. They just see it as a source of information. Canada is currently a restricted jurisdiction, so Canadians cannot make trades on the platform, but the company is working on an international rollout to expand beyond the US market.

Outside Markets

The Dow Jones Industrial Average dipped 62.92 points lower on Monday to settle at 49,167.79, but the S&P 500 firmed up 8.83 points to 7,173.91. Canada s S&P/TSX composite stock index yesterday declines 86 points to 33,818.

Early Tuesday, the June Dow Jones Futures are up 110 points, but S&P 500 and Nasdaq indexes are weaker after notching their latest in a series of record closing highs yesterday. Canada s TSX futures are little changed this morning ahead of the federal government s economic update this afternoon. European stock markets are mixed this morning.

Global stock markets are mixed this morning as investors braced for a week packed with central bank meetings and corporate earnings, and also weighed a diplomatic impasse in US-Iran negotiations.

Inflation expectations have risen uncomfortably over the past two months, driven by a notable jump in energy prices, Ipek Ozkardeskaya, senior analyst at Swissquote, wrote in a note. At this stage, no one…including central bankers…can predict what comes next if Middle East tensions continue to disrupt energy flows. What we do know is that the longer the Strait of Hormuz remains under strain, the stronger the impact on markets will be.

Monetary policy makers in Canada, the US and across the Group of Seven will probably keep their interest rates steady this week. The Bank of Canada and the US Federal Reserve s Open Market Committee meeting begins this morning and ends Wednesday afternoon. The UK, Germany and Japan are widely anticipated to leave their interest rates unchanged as well.

The June US Dollar Index is up 0.292 at 98.610. The Canadian dollar weakened against its US counterpart…currently quoted at 73.18 US cents.

June crude oil futures are up $3.67 at US $100.04/barrel. Oil prices are extending gains this morning as efforts to end the US-Iran war appear stalled, with the crucial Strait of Hormuz still mainly shut, keeping energy supplies from the key Middle East producing region out of the reach of global buyers. ?

Talks around peace still look largely superficial and lack concrete evidence of de-escalation. Despite the rhetoric, vessel movement through the Strait of Hormuz remains curtailed, and that prolonged disruption is what s keeping oil risk premiums elevated, said Phillip Nova s senior market analyst Priyanka Sachdeva.

Grain Markets

Chicago soybean futures are fractionally to 2 cents/bu weaker this morning. Nearby bean futures rallied up 10 to 13 cents on Monday, with deferreds up 5 to 9 cents. Soymeal futures are up $1 to $2/ton this morning after finishing $1 to $9/ton higher yesterday. Soyoil futures are 6 to 22 points weaker this morning after gaining 27 to 36 points on Monday. Assumed soybean crush margins are now exceeding the highs from 2022.

There are a lot of questions about next month s trade US talks with China. That at least to some degree hinges on what happens in Iran and the Middle East. Crude oil was higher Monday on concerns about lagging conflict negotiations.

USDA yesterday tallied US soybean export shipments at 628,826 tonnes for the week ended on April 23. That was 16.9% below the week prior, but 36.9% above the same week last year. US marketing year exports for 2025/26 are now 32.81 MMT since September 1, which is now 24% below the same period last year.

The weekly Crop Progress report from USDA showed the US soybean crop at 23% planted by April 26, well above the 12% average pace for this time of year. Emergence was at 8%, vs. 1% on average.

Chicago corn futures are trading 2 to 4 cents higher this morning. The corn market on Monday posted gains of 1 to 5 cents across the board.

USDA s export inspections report on Monday showed 1.644 MMT of US corn shipped in the week ended April 23. That was 1.33% below the same week last year and a 5.67% drop from last week. The US marketing year total is now 53.441 MMT of corn shipped since September 1, which is 30.64% above the same period last year.

USDA crop progress data showed the US corn crop at 25% planted as of Sunday, which was 6% ahead of the 5-year average pace of 19%. The crop was also 7% emerged, which is 3 percentage points faster than normal.

Traders are monitoring US planting weather, expecting more rain in parts of the Corn Belt for much of this week. While widespread rainfall is seen as a long-term benefit for development, the precipitation has missed portions of the region and some areas have also experienced severe storms and flooding.

Dry weather is an issue for some second crop growing areas in Brazil, leading to some talk about production cuts.

US wheat markets are the strongest of the ag sector this morning…Minnie spring wheat futures are up 7 to 9 cents, HRW 12 to 15 cents higher and SRW wheat rising mostly 10 to 11 cents. The US wheat complex saw strength across most contracts on Monday. HRW/HRS wheat futures contracts are trading near 2-year highs now.

USDA export inspections data showed US wheat at 365,156 tonnes shipped in the week ended April 23. That was down 29.53% from last week and 43.84% below the same week last year. US marketing year shipments have totaled 21.856 MMT, which is up 24.7% yr/yr.

USDA crop progress data showed the US spring wheat crop at 19% planted, now 3 percentage points behind the pace from the last 5 years (22%). Emergence was pegged at 5%. The winter wheat crop was at 34% headed, which was 13 percentage points head of normal. Condition ratings were unchanged at only 30% good to excellent, and 35% poor to very poor (2 points worse than last week). That compares with last year’s 49% good-to-excellent rating. The key HRW wheat state of Kansas is rated only 23% G/E, with 41% of that crop rated poor to very poor.

Traders are monitoring rain chances for very dry portions of the central and southern US Plains. Recent rainfall has missed some areas and while there are more chances in the hard red winter region this week, coverage and totals are uncertain…and it might even be too little, too late. In comparison, some US soft red winter growing areas might be too wet.

Fertilizer availability and dry weather could impact planted area in Australia. The trade s also looking at conditions in Argentina, Canada, Europe, Russia, and Ukraine. There is the potential for frost damage in parts of the Black Sea region this week.

CANADIAN GRAIN MARKET

ICE canola futures ended little changed on Monday, as gains in crude oil were offset by a stronger Canadian dollar.

Continued concerns around the US-Iran conflict and the blocked Strait of Hormuz pulled crude higher, while the Canadian dollar climbed to its highest in seven weeks. A stronger Canadian dollar makes canola appear more expensive to foreign buyers, limiting export interest.

July canola eased 40 cents yesterday to close at $741.80/tonne, while November settled 20 cents higher at $738.

For today… canola futures are trading $3 to $4/tonne higher this morning, maintaining a near 2-week uptrend and now looking to test the winter highs. July canola is up $3.80 this morning at $745.60/tonne amid a lack of fresh fundamental developments, with chart resistance at $750 looming ever closer. And while CBOT soyoil futures are slightly weaker this morning so far, the last time bean oil was trading over 70 cents/lbs, canola was trading around $850/mt.

Chicago soybeans are modestly weaker this morning…as is soyoil. Malaysian palm oil was only steady to barely higher overnight thanks to gains in energy markets offsetting weak export shipments. European rapeseed is higher, but the real story continues to be an apparent short squeeze going on in the May contract as it nears its April 30 expiry.

Crude oil trading back right at $100/barrel on a lack of optimism over any end in sight to the Iran standoff surely is helping. Time is running out for fuel and fertilizer to pass through the Strait of Hormuz before significant impacts are seen.

Stay informed with our daily market videos. Each video quickly covers key futures moves, price trends, and market signals that matter to Canadian farmers. Get clear, timely insights in just a few minutes. Bookmark https://www.producer.com/markets-futures-prices/videos

To access the latest futures prices, go to https://www.producer.com/markets-futures-prices/

Source: producer.com