AM Market Report – March 19, 2026

GOOD MORNING…HERE IS YOUR MORNING MARKET NEWS

OVERNIGHT GRAIN TRADE

Grain markets were trending generally higher up to less than an hour ago…but have since turned down this morning…currently quoted between $1 and $3/tonne lower. Chicago soybeans are 2 to 7 cents/bu higher, led by the deferreds contracts. Upside movement in the soybean market…particularly in the front month contracts…is limited by Trump s delay in the US-China trade summit.

CBOT corn futures are 3 to 4 cents higher… poised to produce a 10-month high close today. Demand for US corn remains supportive, along with early estimates of 3 to 4 million fewer US corn acres expected for USDA s March Planting Intentions Report on March 31.

Read Also

Prairie Weather

A low pressure system is pushing across the northern Prairies this morning with the heaviest rain/snow falling west of Edmonton. This…

US wheat markets are also in the green this morning…spring wheat futures up a solid 5 to 8 cents, HRW rising 2 to 3 cents, with SRW wheat 2 to 4 cents higher. Wheat is leading crop market gains due to support from a widespread drought in US hard red wheat regions. Additionally, the energy market, soaring sharply amid the war in Iran, is supporting the commodities markets generally.

In Other News

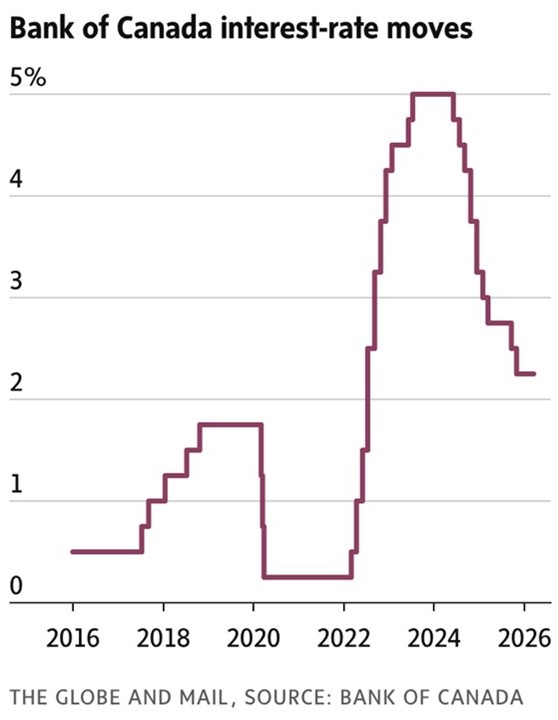

– BoC holds benchmark rate at 2.25% amid oil price shock… The Bank of Canada left its key policy interest rate unchanged at 2.25% on Wednesday, as policymakers weighed a difficult mix of softer Canadian growth and rising global inflation risks tied to the war in the Middle East. It marked the third consecutive time the Bank had held its key rate unchanged, with the last move…a reduction…coming in October.

In its accompanying statement, the Bank said the Canadian economy is still expected to post modest growth as it works through the effects of US tariffs and broader trade uncertainty. However, recent data indicate that the near-term outlook has weakened since the Bank s January forecast. The Bank pointed to a soft labour market and sluggish trade performance as signs that economic momentum has faded in early 2026.

February inflation slowed to 1.8%, down from 2.3% in January, and core measures were described as close to 2%. Still, the February inflation report did not reflect the start of the war in Iran, and the Bank said the recent jump in gasoline and broader energy prices will likely push global inflation higher in the near term…even if the impact on the Canadian economy remains uncertain.

Since the outbreak of the conflict in the Middle East, global oil and natural gas prices have risen sharply, and this will boost global inflation in the near-term, the Bank said. In addition to energy supply disruptions, transportation bottlenecks stemming from the effective closure of the Strait of Hormuz could impact the supply of other commodities, such as fertilizer.

Yesterday s rate decision was widely expected. Economists had largely anticipated the Bank would stay on hold, arguing that inflation was still close to target and that the Canadian economy remained too fragile for a rate increase, even as oil-related risks grew.

For Canadian farmers, the hold is a mixed signal. On one hand, steady rates may help keep operating loan and machinery financing costs from rising further. That matters for farms carrying significant debt or planning land, equipment, or input purchases. On the other hand, the Bank s warning about energy and possible fertilizer supply disruptions is important for agriculture, because higher fuel and fertilizer costs could squeeze margins even without another rate hike.

– US interest rates also unchanged… US Federal Reserve officials yesterday left US interest rates unchanged and maintained expectations of one rate cut this year, acknowledging increasing uncertainty due to the war in the Middle East. The Federal Open Market Committee voted 11-1 to hold the benchmark US federal funds rate in a range of 3.5% to 3.75%. Governor Stephen Miran dissented, calling for a quarter-point reduction.

Fed Chair Jerome Powell emphasized that officials would have to see progress toward lowering inflation, especially goods inflation that had been boosted by tariffs, to resume lowering rates. If we don t see progress, then we won t see the rate cut, Powell noted in post-meeting remarks.

Policymakers, in their post-meeting statement, further underscored the uncertainty they re facing in the economy. It is too soon to know the scope and duration of the potential effects on the economy. The thing I really want to emphasize is that nobody knows, Powell stated.

Powell also indicated that he had no intention of resigning as a member of the Fed s Board of Governors until an investigation by the Department of Justice into a building renovation project at the Fed is well and truly over. He also said that if his successor is not confirmed before his term as chair ends in May, he would serve as chair pro tempore, according to Bloomberg.

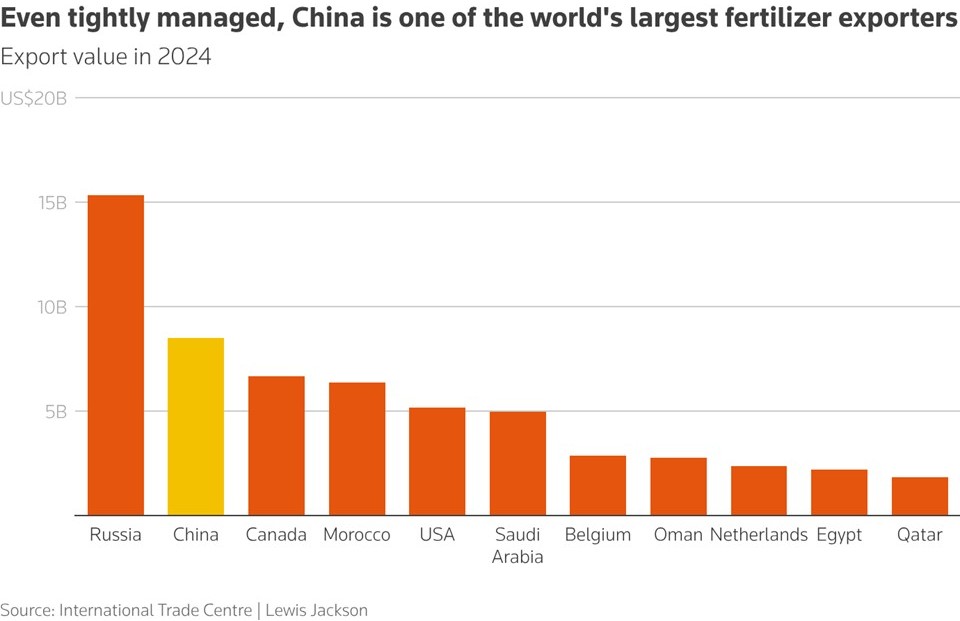

– China restricts fertilizer exports… China is clamping down on fertilizer exports to protect its domestic market, a number of industry sources said, putting an additional strain on global markets that were already grappling with shortages caused by the US-Israeli war on Iran. China is among the largest fertilizer exporters…shipping more than $13 billion worth of it last year…and it has a history of controlling exports to keep prices low for its farmers.

Shipments through the war-blocked Strait of Hormuz account for roughly one-third of the sea-borne supply. In mid-March, Beijing banned exports of nitrogen-potassium fertilizer blends and certain phosphate varieties, sources told Reuters. The ban, which has not been formally unveiled, was reported earlier this week by Bloomberg News.

Added to existing bans and export quotas for urea, only a handful of fertilizers…notably ammonium sulphate…can be exported. That would mean between half and three quarters of China’s exports last year are restricted, potentially up to 40 MMT, according to a Reuters estimate.

Beijing’s curbs, like its move last week to ban refined fuel exports, come as governments limit exports of products whose inputs have been threatened by disruption from the war, worsening shortages and higher prices around the world. International urea prices have risen by around 40% from pre-war levels.

– Big US corn acres… S&P Global Energy has released its US planting projections for the 2026, which are based on the results of a monthly survey of farmers and agribusinesses. It forecasts US farmers will plant 95.2 million acres of corn and 85.0 million acres of soybeans.

The firm s corn acreage projection was up slightly from its January estimate of 95.0 million acres, but well below 98.8 million acres seeded in 2025. Its soybean acreage projection also rose slightly from January s 84.5 million acres, and well above the 81.2 million acres planted in 2025.

The firm estimated US winter wheat plantings for harvest in 2026 at 44.05 million acres, 40,000 acres above its January projection, but down by around 1.3 million acres from 2025.

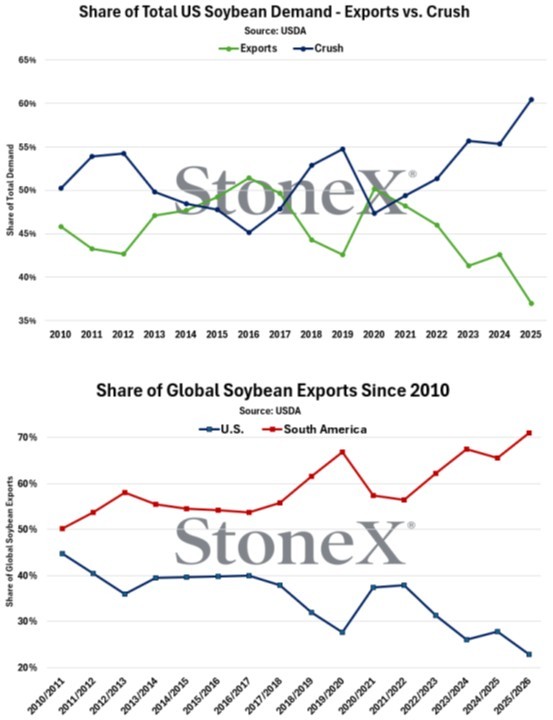

– US soybean demand evolution…The charts below highlight the importance of the upcoming finalized US Environmental Protection Agency (EPA) policy guidance amid the backdrop of a shifting global soybean landscape. The top chart below shows the sharp divergence in the share of total US soybean demand going to exports vs crush, with the latter now accounting for over 60% of our total demand.

Obviously, a big part of this shift is the ongoing expansion of South American soy production and subsequent takeover of the world export market, with Argentina/Brazil/Paraguay combining to account for over 70% of global exports for the first time on record in 2025-26. With this context in mind, US domestic biofuel policy support and new uses become more important for supporting overall US soybean demand in the longer-term.

– Cattle disease spreads in Russia… Cattle diseases officially identified as pasteurellosis or rabies have spread across Russia, affecting at least 10 regions as of Wednesday, but some farmers and scientists are questioning the diagnosis and the sweeping culls ordered by authorities. Officials on Wednesday imposed a cattle quarantine in part of the Chuvashia region in the Volga, more than 2,500 km west of Siberia’s Novosibirsk region, where a state of emergency has been declared.

Farmers in Novosibirsk…who have been confronting police and officials in the biggest non-political protests since the start of the war in Ukraine…say pasteurellosis, a bacterial infection, can be treated with antibiotics. Veterinary expert Svetlana Shchepyotkina said regulations require treating animals sick with pasteurellosis and vaccinating healthy herds. Animals with rabies can be removed only after the diagnosis is confirmed. “Destroying livestock due to pasteurellosis is sheer unprofessionalism and, frankly, outright madness,” she said.

Kremlin spokesman Dmitry Peskov said rapid action was needed in such cases, without commenting further. The agriculture ministry did not respond to a request for comment.

A government commission led by Sergei Dankvert, head of the agriculture watchdog, has arrived in the region to examine local measures that include burning thousands of culled cattle. Russian media have also reported outbreaks in regions bordering Novosibirsk, including the Republic of Altai, which neighbours China…a country known for strict veterinary controls.

Outside Markets

The Dow Jones Industrial Average plunged down 768.11 points on Wednesday to settle at 46,225.15, while the S&P 500 down 91.39 points to 6,624.70. Canada s TSX Composite index dropped a steep 616 points yesterday to 32,312 points. Early Thursday, the June Dow Jones Futures are down another 241 points.

Global stock markets are weaker after a major escalation in the US and Israel s war with Iran rattled investors. Wall Street futures are in the red after major North American markets closed sharply down yesterday in the wake of hawkish central bank commentary. TSX futures followed sentiment lower.

This latest (war) escalation feels like a turning point for markets because the conflict is no longer just about ?military headlines or Strait of Hormuz closure, said Charu Chanana, chief investment strategist at Saxo in Singapore. It is ?now hitting the plumbing of the global energy system. What is unsettling markets now is the growing stagflation risk… It means this is no longer just a geopolitical story but a macro one.”

The June US Dollar Index is down 0.188 at 99.685. The Canadian dollar weakened against its US counterpart…currently quoted at 72.88 US cents.

May crude oil futures are up $0.71 at US $96.17/barrel. Oil prices are slightly higher this morning, but have pared sharper gains posted during the overnight session sparked by news Iran attacked energy facilities across the Middle East following Israel s strike on its South Pars gas field, a major escalation in the war.

Escalation in the Middle East, precise attacks on oil infrastructure, and the death of Iranian leadership all point to a prolonged disruption in oil supplies, Phillip Nova analyst Priyanka Sachdeva said in a note. Adding fuel to the fire, the US Federal Reserve served steady rates with a hawkish narrative, pointing to the economic concerns that follow a war.

Qatar’s state oil giant QatarEnergy said on Wednesday that Iranian missile attacks on Ras Laffan, the site of the country’s core LNG processing operations, caused “extensive damage”, while the UAE shut gas facilities after intercepting missiles early on Thursday. The attacks, which drew a furious response from US President Donald Trump, came hours after Iran issued evacuation warnings for several oil facilities across Saudi Arabia, the UAE and Qatar, following strikes on its own energy infrastructure in South Pars and Asaluyeh.

Grain Markets

Chicago soybean futures are trading 2 to 7 cents/bu higher, led by gains in the deferreds contract months. Bean futures posted 4 to 10 cent gains across the front months on Wednesday, as new crop also led the charge. Upside movement in the soybean market…particularly in the front month contracts…is limited by Trump s delay in the US-China trade summit.

Soymeal futures are trading $2 to $6/ton higher this morning (nearbys leading) after posting strong $4 to $10/ton gains on Wednesday. Soyoil futures are down a modest 8 to 26 points this morning after falling back late yesterday, finishing steady to 44 points lower. It appears the spreaders are now unwinding long bean oil, short meal spreads.

USDA this morning reported US soybean export sales of 298,200 tonnes for the week ended Mar 12, which came in disappointingly below the range of trade expectations of 350,000 to 800,000 tonnes.

Soybean planted acres are estimated to be 85.66 million acres in 2026 according to an Allendale survey of producers, a 4.46 million acre increase yr/yr. USDA will release their March Intentions report on the 31st.

Soy traders are waiting for more details on the delayed trade meeting between the US and China, originally set for the end of the month. The timeline remains unclear, but it looks like the face-to-face meeting between President Trump and President Xi will happen. While there s been a lot of talk about China buying more US soybeans this marketing year, recent USDA export sales reports have shown only routine (disappointing) sales.

Meanwhile, China and Brazil are expected to talk soon about phytosanitary issues. Brazil s harvest is over 60% complete and their beans offer a substantial price discount to US origin.

Chicago corn futures are generally 3 to 4 cents/bu higher this morning…attempting to post a 10-month high close today. The corn market closed Wednesday s session with front end contracts 7 to 9 cents higher and some deferred contracts 2 to 4 cents in the green.

Demand for us corn remains generally solid and there was spillover price support from the gains in crude oil. That strength in crude continues to be tied to supply concerns caused by the military action in Iran and the Middle East.

EIA data yesterday showed US ethanol production averaging 1.093 million barrels per day for the week ended Mar 13, down 33,000 bpd from the previous week. Stocks data were building on that week, up 827,000 barrels to 26.407 million barrels. The US national regular gasoline price has risen from $2.94/gallon at the end of February to $3.72 for the week of Mar 16.

USDA this morning reported US corn export sales of 1.172 MMT for the week ended Mar 12, near the middle of trade expectations ranging between 0.6-1.8 MMT.

An Allendale survey of producers estimates the US corn acreage this year at 93.68 million acres, which would be a 5.12 million acre drop last year.

Traders are monitoring the harvest in Argentina, along with the first crop harvest and second crop planting in Brazil.

US wheat markets are higher this morning… Minnie spring wheat futures are rallying 5 to 8 cents higher, HRW up 2 to 3 cents on the front months, and SRW wheat gaining 2 to 4 cents. The US wheat complex rallied double digits on Wednesday…spring wheat finishing the day with 11 to 13 cent gains at the close.

There are concerns about winterkill in parts of the US Midwest and Plains after recent bitterly cold temperatures in some areas, with drought, also expected to have an impact on this year s US winter wheat crop, especially hard red winter. A big portion of the US Plains are in some form of drought, with a sharp turn to record high temperatures expected in parts of the region later this week.

USDA this morning reported US wheat export sales of 189,900 tonnes for the week ended Mar 12…coming in below the bottom of trade expectations ranging between 300,000 to 550,000 tonnes.

An Allendale survey estimates all US wheat planted area in 2026 at 44.877 million acres, just under the USDA s Ag Outlook Forum and 451,000 below a year ago, including declines for all types. Allendale has winter wheat planted rea at 33.092 million acres and non-durum spring wheat at 9.678 million acres, falling 61,000 and 312,000 acres from 2025, respectively.

Fundamentally, old crop world wheat ending stocks remain robust, with mostly record production around the world for 2025-2026.

CANADIAN GRAIN MARKET

ICE canola futures ended modestly lower Wednesday, giving up earlier gains and ending lower in late trading as traders took profits, and the market lost support from crude oil.

Canola had been higher for much of the session, but turned lower late in the day as US crude oil backed off and traders locked in gains after the recent rebound from Monday s sharp break. Because canola is closely tied to the broader vegetable oil and energy complex, the later declines in US crude undermined prices even though Brent oil remained elevated.

Chicago soybeans managed gains yesterday, but soyoil ended the day lower. European rapeseed was mixed, while Malaysian palm oil was higher. The Canadian dollar was lower after the Bank of Canada announced earlier in the day it was holding its key overnight lending rate steady at 2.25%.

May was down $3.30 at $726.20/tonne, and November fell $1 to $726.30.

For today… canola futures were trading higher just an hour ago, but have now started turning lower…currently down $1 to $3/tonne on the front month contracts. May canola futures are now $2.00 lower at $724.20/tonne as the Jan-Feb-into the start of March rally appears to be stalling out…at least for the time being. May canola seems caught between $720 and $740/tonne…20-day average technical support down at $712. Bull flag or topping pricing action…indeterminate at this time.

We are seeing CBOT soyoil futures weaken slightly, while soybeans and meal are highs…seems to be some unwinding of long soyoil/short soymeal spreads).

Diesel markets globally remain strong…price supportive to vegoils and oilseeds. The ongoing conflict in the Middle East continues to rattle the energy markets…commodity markets generally, and canola is no exception.

This winter s rally in canola pricing remains a cash pricing opportunity for the grower for an incremental old crop sale and perhaps a modest forward pricing opportunity for a small new crop sale.

Export demand for old crop so far in recent weeks has not matched hopeful expectations after China reduced its tariffs against Canadian canola. Domestic crusher demand remains solid though…just lacking the canola seed export sales volume. But as long as domestic crush margins remain strong…will likely continue to support the current price environment.

Stay informed with our daily market videos. Each video quickly covers key futures moves, price trends, and market signals that matter to Canadian farmers. Get clear, timely insights in just a few minutes. Bookmark https://www.producer.com/markets-futures-prices/videos

To access the latest futures prices, go to https://www.producer.com/markets-futures-prices/

Source: producer.com