Negative feedlot margins soften feeder markets

For the week ending May 9, western Canadian feeder cattle markets traded steady to $10 per hundredweight lower on average.

There were a couple locations, such as Vermillion, Alta., that reported stronger values, but most order buyers had smaller decks last week with lower price limits.

Feedlot operators appeared to be more aggressive on larger packages, in some cases, but there was definitely a softer tone overall.

A producer reported that a pen-sized group of medium to larger frame, mixed steers averaging 985 pounds on controlled weight gain diet of barley and silage with full processing records sold for $450 per cwt. f.o.b. farm northwest of Saskatoon.

The VJV Ponoka market report included 73 tan mixed heifers averaging 828 lb. on light grain and silage diet with full processing data and implants that sold for $480.

At the same sale, Charolais Simmental cross steers with a mean weight of 843 lb. on two lb. of barley and corn silage with preconditioning data, including implants, sold for $519 per cwt.

Read Also

At the Vermillion presort sale, 22 tan heifers averaging 702 lb. traded for $570, and 12 tan steers averaging 741 lb. sold for $605 per cwt.

In Westlock, a smaller package of Angus cross Simmental heifers averaging 681 lb. coming off a diet of hay, barley and oats on the full herd health program sold for $527 per cwt.

At the Clyde sale, red heifers averaging 519 lb. sold for $720 and red steers averaging 596 lb. traded for $695 per cwt.

At the Killarney sale, a package of 11 black steers weighing 555 lb. sold for $730, and an eight-pack of black steers weighing 477 lb. silenced the crowd at $841 per cwt.

Alberta packers were buying fed cattle on a dressed basis at an average price of $565 per cwt., up $5 per cwt. from seven days earlier. Using a 60 per cent grading, this equates to a live price of $339 per cwt. delivered.

The break-even fed cattle price (live basis) for calves bought last October are in the range of $555-$565 per cwt.

Major feedlot operators finally took a step back last week and lowered their bids across Western Canada for all weight categories. Feedlots have endured five consecutive months of negative margins.

Western Canadian feedlot inventories are running seven to nine per cent above year-ago levels.

Cattle on feed 150 days or longer are up 30 per cent from last year.

Steer marketing weights in Western Canada are up 65 lb. from year-ago levels.

This environment shows there is limited demand for replacements at this time. At some point, there will be severe liquidation of fed cattle, which will pressure the live and feeder cattle markets.

Western Canadian feeder cattle prices have been premium to U.S. values, resulting in a year-over-year decline in Canadian feeder cattle exports.

Canadian year-to-date feeder cattle exports for the week ending April 25 were 36,598 head, down from the year-ago figure of 72,859 head.

U.S. feedlot margins are now hovering around breakeven and will slip into negative territory for a prolonged period. Cattle on feed 180 days or more in the United States are up sharply from last year.

The Canadian dollar is expected to appreciate against the U.S. greenback moving forward.

We’re looking for the Canadian dollar to reach up to US80 cents by the end of the year, up from the current level of 73.25 cents. This will contribute to lower demand from U.S. buyers for Canadian feeder cattle.

U.S. feeder cattle outside feedlots as of April 1, 2026, were 18.777 million head, up 416,000 head from April 1, 2025. This was a surprise to the trade.

Look for a year-over-year increase in U.S. feedlot placements in the May or June Cattle On Feed Report.

Our contacts from south of the border are expecting a decision or announcement from the U.S. Department of Agriculture regarding a phased-in opening of the border to Mexican feeder cattle.

We believe the U.S. will start by importing 10,000 to 20,000 head of cattle per month, and this number will slowly work up to 120,000 head per month. This will weigh on the fed and feeder markets for the final quarter of 2026 and first quarter of 2027.

There was minor heifer retention in Canada and the U.S. during 2025. These calves will come on the market this fall. The beef cow slaughter remains at historical lows.

According to Statistics Canada, on-farm barley stocks as of March 31, 2026, were 2.4 million tonnes, down 200,000 tonnes from last year. This was lower than trade estimates.

The barley market has potential to rally $20-$30 per tonne over the next couple of months as the 2025-26 carryout drops to historically low levels. U.S. corn acres may be down more than expected due to historically high fertilizer prices.

On a positive note, McDonald’s reported first quarter 2026 results on May 7 with adjusted earning per share of $2.83 on revenue of $6.52 billion, driven by 3.8 per cent global comparable sales growth.

Same-store sales rose on the strength of customers spending more. Earnings and revenue were better than pre-report estimates.

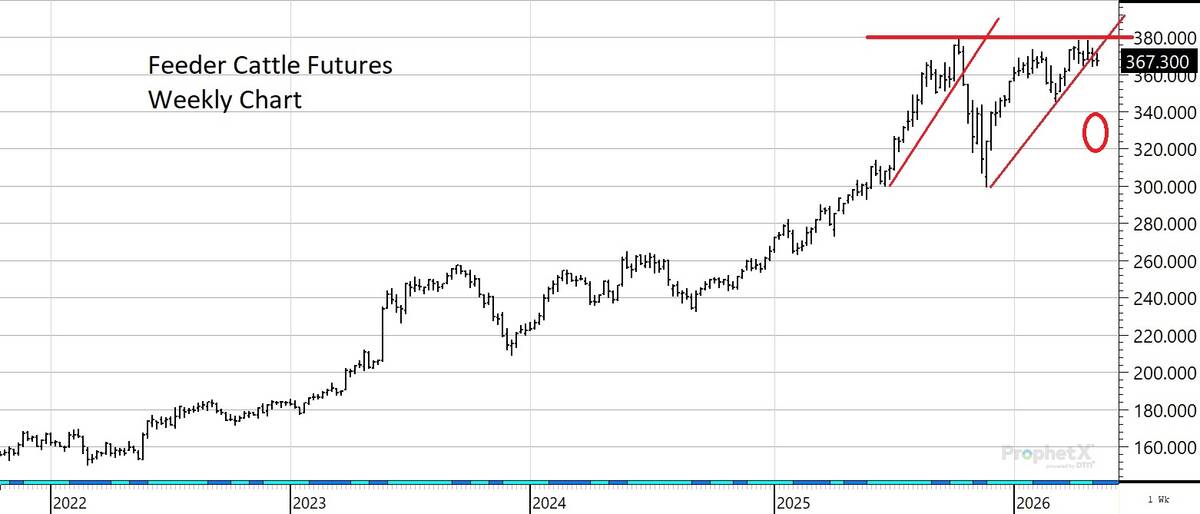

Photo:

Courtesy of DTN Prophet X

Concerns are that higher energy prices will result in lower disposable income and decrease beef demand vis-a-vis lower consumer spending at restaurants.

In conclusion, feeder cattle prices have been hovering at or near historical highs over the past month.

Feedlots in Canada and the U.S. are backed up with market-ready cattle. Marketing weights are up sharply from last year.

U.S. feeder cattle supplies outside finishing feedlots are up from year-ago levels.

There is potential for a phased-in opening of the U.S. border to Mexican feeder cattle.

Beef demand has held up so far, despite higher gas prices. Concerns are that beef demand will ease if the U.S. led war on Iran is prolonged for another couple of months.

Barley and corn prices have potential to percolate higher.

Given this environment, we’ve advised cow-calf producers and backgrounding operators to forward contract 50 per cent of expected fall marketings. Get some sales on the books. Prices are at historical highs.

Source: producer.com