AM Market Report – April 29, 2026

GOOD MORNING…HERE IS YOUR MORNING MARKET NEWS

OVERNIGHT GRAIN TRADE

ICE canola futures winning streak is continuing this morning with posted gains of $7 to $10/tonne, with the nearby July contract rallying $46/tonne since April 17 in a push to a fresh contract high.

Chicago soybean futures are seeing 5 cents/bu gains this morning, led by rallying soyoil (new contract highs). But bean prices remain stuck in a sideways channel. The fastest US soy planting pace since the 1980s is keeping a cap on soybean rallies.

Read Also

AM Market Report – April 28, 2026

GOOD MORNING…HERE IS YOUR MORNING MARKET NEWS OVERNIGHT GRAIN TRADE ICE canola futures are trading $3 to $4/tonne higher so…

CBOT corn futures are mostly 1 to 2 cents higher this morning, holding up at a 4-week high.

US wheat markets are also higher this morning…Minnie spring wheat futures are up another 6 to 8 cents…new contract highs and the highest levels in almost 2 years. HRW wheat futures are at 2-year highs, up 7 to 9 cents this morning. SRW wheat is rising 5 to 6 cents.

Wheat futures markets are leading ag market rallies amid a deteriorating US HRW crop. (See item below) However, bulls need to beware that corn and wheat markets have moved into technically overbought territory and are now due for at least routine downside price corrections.

Updated weather forecasts through the end of April and into the start of May will grip traders’ attention on crop price direction. Meanwhile, energy prices continue to trend higher amid stalled peace talks between the US and Iran.

Latest on the war in the Middle East

– US signals no letup of naval blockade as it aims to squeeze Iran

– Nymex WTI crude oil futures prices back above $100 a barrel

– US warns of sanctions risks for Chinese refiners of Iranian oil

– California jet fuel woes deepen as Asia flows hit decade low

– Bond traders ramp up wagers hedging for 5% 10-year US Treasury yields as oil surges

– European airports warn of tough outlook as war disrupts flights

Commodity markets appear to be coming to terms with the possible outcomes of a prolonged closure of the Strait of Hormuz, with gasoline and diesel markets leading the way higher. Reports suggest that US President Trump has instructed aides to plan for an extended blockade of Iranian ports in an attempt to force them to concede to US terms.

In Other News

– US hard red wheat missing rain at the worst time… World Weather Inc on Tuesday afternoon issued a special report saying a system that brought rain and thunderstorms to portions of the US Plains, Midwest, and Delta this past weekend brought some precipitation to portions of key HRW wheat producing states of Kansas and Nebraska. However, several of the main hard red winter wheat areas in the central and southern Plains missed out on meaningful precipitation, southern and western Kansas in particular. Drought is firmly in place across US hard red wheat country and there is still a pressing need for more rain.

Rain is predicted for Texas and southern Oklahoma later this week, but much of Kansas and northern Oklahoma may be missed again. Other opportunities for showers and thunderstorms will come and go during the following week to ten days, but the odds are not favoring a general soaking and that implies ongoing crop stress and a rising risk to production, said World Weather. The only good news is that there should not be any excessive heat during the next 10 days.

– Commodity prices could rise further if the war persists… Energy prices are expected to surge by 24% in 2026 to their highest level since Russia s full-scale invasion of Ukraine four years ago…and that s IF the most acute disruptions caused by the war in the Middle East END in May, the World Bank said on Tuesday. Commodity prices could rise even further if hostilities in the region escalate further and supply disruptions last longer than expected, the global development bank said in its latest Commodity Markets Outlook.

The bank said its baseline scenario assumed that shipping volumes through the crucial Strait of Hormuz waterway would gradually return to near pre-war levels by October, but said the risks were “markedly tilted” toward higher prices. The bank’s baseline projects a 16% increase in overall commodity prices in 2026, given soaring energy and fertilizer prices and record-high prices for several key metals.

Oil prices are continuing to rise this week as efforts to end the US-Iran war stalled and the Strait of Hormuz remains largely shut, keeping energy supplies, fertilizer and other commodities from the key Middle East producing region out of the reach of global buyers. Attacks on energy infrastructure and shipping disruptions in the strait have triggered the largest oil supply shock on record, the World Bank said.

“The war is hitting the global economy in cumulative waves: first through higher energy prices, then higher food prices, and finally, higher inflation, which will push up interest rates and make debt even more expensive,” World Bank chief economist Indermit Gill said.

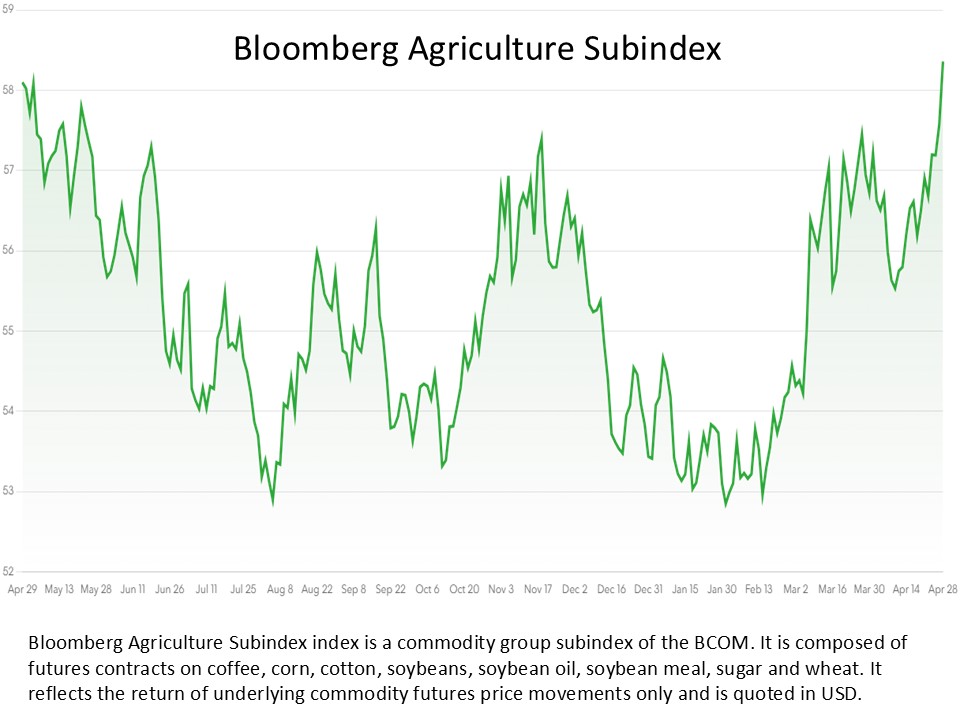

– Bloomberg ag price Index climbs to 2.5-year high… The extended closure of the Strait of Hormuz and extreme weather have jolted the price index for farm commodities to a two-year high as fertilizer headaches and the prospect of smaller harvests drive food inflation risks, said Bloomberg. The Bloomberg Agriculture Spot Index, which tracks 10 of the world s top-selling crop products, has climbed for a third straight month to the highest level since November 2023. That s a pronounced shift from before the war, when most crop prices were weighed down by abundant inventory and bumper harvests. Now, farmers from Asia to Australia and the US are grappling with converging challenges posed by the Iran war and drought, pressuring the prices of staple food products from bread to pasta and cooking oil. The war has changed that balance materially, primarily through energy, fertilizer, and logistics channels.

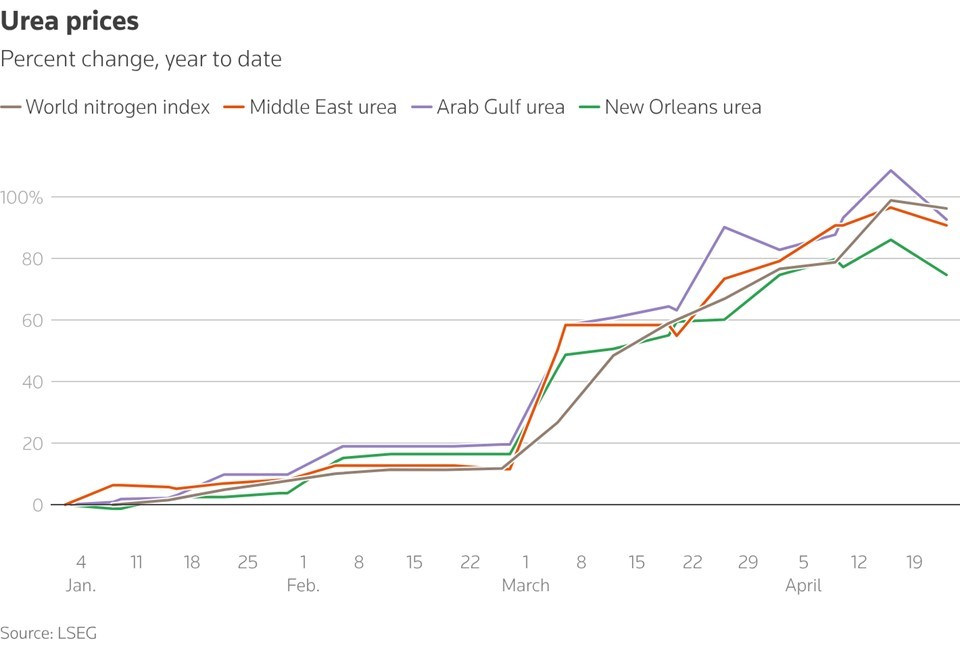

– Iran war fertilizer squeeze could spell trouble for next year’s grain harvests… Farmers around the world are facing a second surge in fertilizer prices in four years due to the Iran war. But with grain prices too low to cushion the blow from the deeper supply crunch this time around, many are rethinking planting plans, putting global food ?production at risk. The Middle East is a leading fertilizer production hub, and much of the global fertilizer trade typically passes through the Strait of Hormuz, which has seen traffic brought to a ?standstill by the conflict.

Supplies of nitrogen-based urea fertilizer from the world’s largest production facility in Qatar have been halted, and flows of sulphur and ammonia, common inputs for a range of fertilizers, have also been curbed.

With a resolution of the conflict proving elusive, analysts, traders, fertilizer producers and agronomists are looking back at the last supply crisis, Russia’s 2022 invasion of Ukraine, worried that this time things could get even worse. “Back in 2022, a lot of the fertilizer was ultimately flowing through,” said Shawn Arita of the Agricultural Risk Policy Center ?at North Dakota State University. “It’s a much steeper supply crunch that we’re seeing now.”

As fertilizer prices have jumped since the onset of the war in late February, urea has seen the sharpest price spike, reflecting the loss of the roughly one-third of globally traded volumes typically exported from the Gulf.

Some are paying. India, the world’s largest rice producer and ?second-biggest wheat grower, has booked record volumes of urea in a single import tender, paying nearly twice as much as it did just two months ago. But such price levels are beyond the reach of many, analysts say.

In 2022, high global ?grain prices helped farmers offset the steep increase in input costs caused by the Ukraine war. But ample harvests of grains and oilseeds in recent years have restrained crop prices. As a result, many growers today lack the revenue to absorb ballooning fertilizer bills.

Many farms still have fertilizers on hand, while record harvests last year have boosted global grain stocks. So the immediate impact of the current crisis on global food supplies may be limited. But agricultural bodies, including the International Grains Council, are already cutting their forecasts for the next harvests. And the United Nations, which is trying to ?negotiate shipping access for fertilizer through the Gulf, has sounded ?the alarm over food security in developing nations.

– Fertilizer export clampdown… China is stepping up customs inspections to enforce its new fertilizer export controls, Reuters reported. The intensification comes as gaps widen between domestic and international prices that have surged after disruptions linked to the closure of the Strait of Hormuz. The report, citing three fertilizer traders, said exports of ammonium ?sulphate…one of China’s largest fertilizer exports by volume, which was excluded from restrictions introduced in March…are now subject to customs inspections.

– Argentina meal rejection fallout… The Netherlands flagged four Argentine and two Brazilian soymeal shipments containing banned genetically modified organisms, leading to at least three withdrawals and prompting Argentina on Tuesday to question Dutch testing methods. The findings put a spotlight on GMO compliance from the European Union’s largest suppliers of the livestock feed and could boost demand for other origins including the US and Ukraine.

Outside Markets

The Dow Jones Industrial Average ticked 25.86 points lower on Tuesday to settle at 49,141.93, while the S&P 500 dipped 35.11 points to 7,138.80. Canada s S&P/TSX composite stock index fell 234 points yesterday to 33,585.

Early Wednesday, the June Dow Jones Futures are down 41 points, while the S&P 500 and Nasdaq indexes are slightly higher. TSX futures are little changed this morning to slightly weaker, with Canada s main stock market on its longest daily losing streak this year. European stock markets are slightly lower this morning, while Asian markets were mixed overnight.

Global stock markets are mixed to slightly weaker this morning as attention turned to interest rate policy decisions by the Bank of Canada and US Federal Reserve later today, and Big Tech earnings after markets close. Central banks on both sides of the border are expected to keep interest rates steady.

For us, earnings are the most important part of the story right now, said Kate Moore, chief investment officer at Citi Wealth. First-quarter earnings are tracking year-over-year growth and climbing, she said.

The June US Dollar Index is up 0.119 at 98.595. The Canadian dollar weakened against its US counterpart…currently quoted at

June crude oil futures are rallying up $3.90 at US $103.83/barrel. Oil prices are on the rise this morning, extending a multiday rally, on media reports the US will extend ?its blockade of Iranian ports, likely prolonging supply disruptions from the key Middle East producing region.

The recent rise in oil prices ?has been driven by the Strait blockade. ?If Trump is prepared to extend the blockade, supply disruptions would worsen further and continue to push oil prices higher, said Yang An, ?an analyst at Haitong Futures.

Grain Markets

Chicago soybean futures are trading 5 cents/bu higher this morning as the bean market is trying to push up and above a sideways channel its has operated in for the past 7 weeks. Bean futures closed Tuesday s session with front months down 1 to 4 cents in the front months and fractionally to 1 cent higher in the deferreds. Soymeal futures are about unchanged this morning after ending down $0.40 to $1.50/ton yesterday across the front months. Soyoil futures are up a solid 90 to 105 points this morning (fresh contract highs) after gaining 50 to 112 points yesterday on the front months.

US domestic soy crush margins remain firm and are at new all time highs, using the CBOT formula. D4 RIN biodiesel values are over $1.90/gallon, the highest since late 2022.

The fast pace of US soybean planting is noted, with some crops already emerging in Iowa. Plenty of rain is falling for the Midwestern crops as of Tuesday.

Market eyes remain on the trade summit scheduled in May between the US and Chinese leaders. What happen there may hinge, at least to some extent, on what happens in negotiations about the conflict in Iran and the Middle East. China is a major trading partner of both the US and Iran.

On the export front, Brazil’s freshly harvested record large crop is price competitive to US soybeans.

Chicago corn futures are up 1 to 2 cents/bu this morning. The corn market closed Tuesday with 3 to 6 cent gains, as spillover support from an explosive wheat market is supportive. As it moves closer to March 2026 highs, the corn market has finished up in six of the past seven sessions.

US crop weather remains favorable for the corn already seeded. Planting and emergence are ahead of average. How many acres will actually get planted this year is still up in the air.

Argentina s corn harvest is ongoing, and parts of Brazil need rain, but most of the crop is still in good shape.

Over 30 US renewable fuels stakeholder groups sent a letter to US lawmakers on Tuesday, urging them to attach an amendment to the Farm Bill that would allow the nationwide, year-round sale of E15 gasoline. A floor debate on the Farm Bill has not been scheduled.

US wheat markets are still charging higher this morning to fresh contract and near 2-year highs… Minnie spring wheat futures up 6 to 8 cents. HRW gaining 7 to 9 cents and SRW wheat 5 to 6 cents higher. The US wheat complex posted a strong double digit rally across the three exchanges on Tuesday…SRW futures up 17 to 28 cents, HRW 18 to 29 cents higher and spring wheat 12 to 21 cents higher.

The next 7-day outlook via the NOAA forecast looks dry in much of Kansas, with parts of Oklahoma and Texas seeing 1 to 2 inches. With OK at 43% headed and TX at 65%, that may come too late.

Analysts see the wheat market getting technically overbought following the early week rally, but no topping signal yet. Continued deterioration of this year s US winter wheat crop, super-charged with spec fund buying, has rallied US wheat futures. Additionally, rain chances have been removed from the two-week outlook for western Kansas, where the crop is struggling the most. The crop is not dead, but it is dying. It looks increasingly like hard red winter acreage abandonment rates will be significant due to widespread drought.

Additionally, there are some concerns about excessively wet conditions impacting soft red winter in parts of the eastern US, and US spring wheat planting is slower than normal.

Globally, the trade is monitoring the potential for freeze damage in parts of Russia and Ukraine, slower planting in Canada, and probable issues with fertilizer availability impacting planted area in Australia.

CANADIAN GRAIN MARKET

Crude oil helped to lead the way higher as ICE canola futures settled with gains on Tuesday. US crude oil futures gained for the seventh straight session yesterday, climbing above the $100/barrel benchmark, as the US and Iran still appear no closer to ending their conflict which has largely closed the Strait of Hormuz. About 20-25% of the world s seaborne oil supply flows through the strait.

The gains in crude sent Chicago soyoil futures higher as well, although soybeans were just mixed on the day. European rapeseed was also higher, while Malaysian palm oil closed with losses. Weakness in the Canadian dollar was supportive for canola.

July finished Tuesday up $6.10 at $747.90/tonne, and November added $6.70 to $744.70.

For today… canola futures are showing solid $8 to $10/tonne gains this morning on strengthening world vegoil and energy markets. Benchmark July canola futures are up $10.20 at $758.10/tonne, up an impressive $46/t since April 17 and for the first time punching above chart resistance at $750.

US soybean product rallies have resulted in the May canola crush margin hitting another record of $371.21/tonne Tuesday according to the ICE crush margin calculation. That compares to $111.95/mt a year ago. For the record, the $259.26/t difference represents a $5.88/bu improvement in the canola crush margin in a year. It appears there is room for canola seed values to improve now that they are breaking through resistance. It’s also worth repeating that the last time US soyoil was at these price levels, canola was trading around $870/tonne.

Interesting to note… The USDA s Foreign Ag Service office in the European Union says the European Commission is looking at phasing out soybeans as a biofuel feedstock by 2030, which would have an impact on US soybean and soyoil exports to the bloc…potentially opening the door to more canola/rapeseed use.

On the feed grains… Feed barley and wheat prices are staying strong as planting begins in some areas of the Prairies. Evan Peterson, a trader with JGL Commodities in Saskatoon, said delivered feed barley in Lethbridge was selling at a range of $310 to $315/tonne. In addition, feed wheat was also selling at around $305/tonne in Lethbridge.

Peterson added that seasonal trends are keeping prices elevated due to growers shifting their mindset from marketing to planting. Strong export demand is also pushing prices higher. We re seeing Saskatchewan bids moving more aggressively than feed grain bids in southern Alberta, he said. A lot more of the grain has been funneling into the export market than the domestic market this year.

Seeding has already started in parts of southern Alberta, but most of the Prairies are dealing with cool conditions. In central Saskatchewan, a recent snowstorm has further delayed fieldwork. Northern Saskatchewan is still covered in snow from the winter. Eastern Saskatchewan is still covered in a blanket, Peterson said. There has been substantial moisture province-wide, it seems.

Feedlot demand is also creeping back up , he added. We ll just see what kind of demand there is.

Saskatchewan feed barley cash pricing ranged from $5.12 to $5.45/bu as of April 27, while Manitoba s prices ranged from $4.94 to $5/bu. Both provinces saw no change from the previous week. Meanwhile, Alberta s prices were up seven cents at $5.01 to $6.86/bu.

Stay informed with our daily market videos. Each video quickly covers key futures moves, price trends, and market signals that matter to Canadian farmers. Get clear, timely insights in just a few minutes. Bookmark https://www.producer.com/markets-futures-prices/videos

To access the latest futures prices, go to https://www.producer.com/markets-futures-prices/

Source: producer.com