AM Market Report – May 11, 2026

GOOD MORNING…HERE IS YOUR MORNING MARKET NEWS

OVERNIGHT GRAIN TRADE

ICE canola futures are tipping modestly lower this morning, down $1 to $2/tonne after posting sold gains on Friday. Chicago soybean future are up a more promising 7 to 10 cents/bu, with both meal and soyoil futures rising.

Chicago corn futures are posting 3 to 4 cents gains this morning.

US wheat markets are also higher this morning… Minnie spring wheat futures are gaining 6 to 7 cents, while the winter wheats are up 6 to 8 cents.

Market bulls are out of the chute in good fashion to start what is an important trading week for the grain markets. The monthly USDA supply/demand report is out Tuesday and US President Trump and Chinese President Xi meet in China later this week. (See items below).

Grain markets chopped following crude oil most of last week. Headlines have been all over the place regarding developments of the US war with Iran. Crude oil prices surged on Sunday after President Trump deemed the Iranian response to a US proposal to end the war was “totally unacceptable”.

Watching this week

This week could prove to be one of the most important of the year so far when it comes to agricultural markets.

– On Tuesday, USDA will deliver its May World Agricultural Supply and Demand Estimates, or WASDE, report, which will offer the department s initial outlook for the new crop year.

– On Wednesday, the US House of Representatives is slated to vote on long-sought legislation to green-light year-round US domestic sales of E15.

– US President Donald Trump is scheduled to visit China Thursday and Friday, where a meeting with China President Xi Jinping is being watched to bring affirmation that Beijing will follow through on commitments to buy US soybeans…and maybe other agricultural goods. But serious trade and political tensions need to be navigated.

– And then of course, there s the Iran war and the potential for more market-driving headlines.

All the elements are there for relief, exuberance, or disappointment. Take your pick.

Latest on US-Iran war…

The US and Iran remain far apart on a framework to end their war and reopen the Strait of Hormuz, with US President Donald Trump calling Iran’s reply to his proposed peace plan unworkable. Iran demanded a lifting of the US naval blockade and sanctions relief, while maintaining a degree of control over traffic through Hormuz, and insisted that any agreement must result in an immediate end to fighting. Israeli Prime Minister Benjamin Netanyahu said the war was not over because there was more work to be done to remove enriched uranium from Iran.

The impasse means Hormuz remains largely blocked, with Iran and other Persian Gulf countries mostly unable to export energy supplies through the waterway, and a ceasefire that took hold just over a month ago remains fragile.

With Trump due to visit China this week (May 14-15), there has been mounting pressure to draw a line under the war, which has ignited a global energy crisis and poses a growing threat to the world economy. The US president will attend a state banquet in Beijing on Thursday evening and then have a tea and working lunch with his Chinese counterpart, Xi Jinping, on Friday before leaving.

China’s crude oil imports fell to the lowest level in almost four years in April as the closure of the Hormuz Strait choked off supplies to the world’s largest oil importer. Crude oil imports fell 20% in April to 38.5 MMT compared to a year earlier, hitting their lowest level since July 2022, according to customs data released on Saturday.

In Other News

– Grain traders await Tuesday s USDA monthly supply/demand report…Tuesday s monthly USDA supply/demand report will be one of the highlights of the grain trading week. Chicago corn traders are expecting the agency to significantly reduce this year s forecast US corn production level from that seen last year. Traders are also expecting a slight rise in US and global corn stocks, compared to the April USDA S&D report.

Soy complex traders expect a modest rise in estimate 2026 US soybean production, compared to last year. Traders expect a slight dip in US soybean stocks, but a slight rise in global stockpiles, compared to the April USDA S&D report.

Wheat traders expect Tuesday s report to show a significant decline in US all wheat production this year compared to last year. Global wheat stocks are seen near unchanged from last year. Wheat traders will be watching results of this week s annual HRW tour through Kansas sponsored by the US Wheat Quality Council.

– Saskatchewan seeding off to a slow start… Spring planting has started in some areas of Saskatchewan, albeit at a slower pace than in previous years. The province s first weekly crop report of 2026 was released on May 7, saying that 3% of projected acres were planted as of May 4. Cold temperatures, frozen soils and washed-out roads had limited seeding progress to that time when the 5- and 10-year averages were 12 and 13 per cent, respectively.

Saskatchewan s southwest region was the furthest ahead in planting at 7%, while the west-central region was at 1%. The east-central, northwest and northeast regions hadn t begun planting yet.

Durum led the major crops at 10% planted, with field peas at 6%. Barley and lentils were at 4% complete, while chickpeas, mustard and canola were at 3%. Spring wheat, oats and flax were at 2%.

Cropland topsoil moisture was rated at 24% surplus, 69% adequate and 7% short.

– Seeding also slow in Alberta, especially up north… While seeding in southern Alberta was slightly below the expected pace for early May, cold and snow in the rest of the province has put planting on hold as of last Tuesday (May 5). Only 8.3% of the province s projected acres were planted as of that date, compared to the 15.3% for the five-year average, said the province s first weekly crop report of 2026 released Friday.

The south region saw 25.5% of its acres planted, compared to the 36.5% of the five-year average. In central Alberta, 3.5% of acres were seeded, well below the 11.9% average. The northwest and Peace regions were at 0.2%, behind their 3.3% and 6% averages, respectively. The northeast was at 0.1%, compared to its average pace of 2.6%.

Durum wheat led all crops at 33.7% planted, just behind chickpeas (31.3) and lentils (22.3). Spring wheat planting was at 7.4%, while oats and canola were at 0.7 and 0.8 per cent, respectively.

Fall-seeded crops in Alberta were rated at 67% good to excellent, two points behind the five-year average, with the south region at 74%. Only 30% were rated good to excellent in the northwest.

Surface and sub-surface soil moisture were assessed at 68% and 60% good to excellent, respectively. The northeast had the best surface soil moisture rating at 74.4%, while the northwest had the worst at 47.9%.

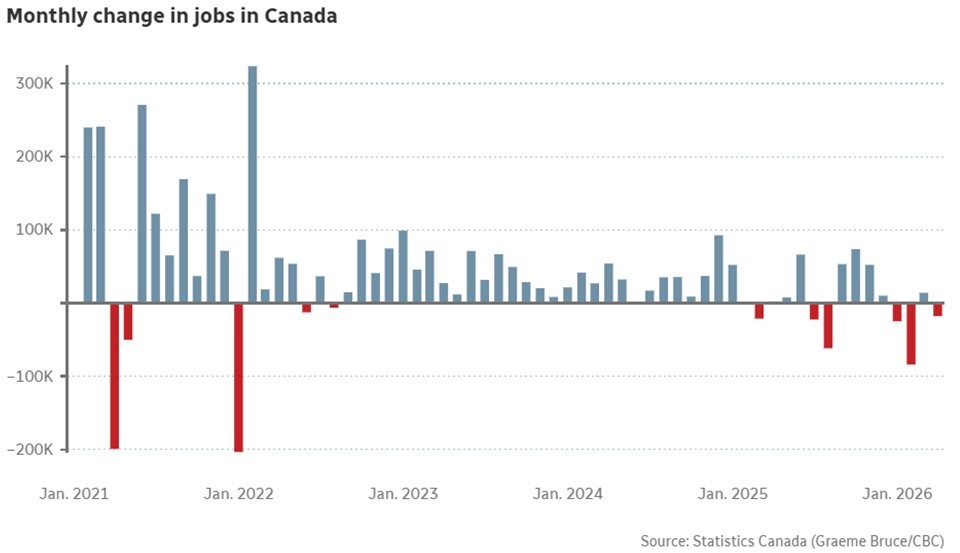

– Unemployment rate rises… Canada’s unemployment ?rate rose to a six-month high of 6.9% in April as the economy lost 17,700 jobs, Statistics Canada data showed on Friday, indicating a continued weakness in the labour market which has struggled in the face of US tariffs and trade uncertainty. Last month’s loss means Canada has lost jobs in three out of the four months so far this year, showing a rocky start for the labour market in 2026. Employment losses were concentrated in information, culture and recreation, construction and in other services.

Average hourly wages of permanent employees, a metric closely tracked by the Bank of Canada to gauge rise in inflation expectations, grew 4.8 ?from a year earlier, versus 5.1% in March.

The participation rate…the portion of the population ?over the age of 15 that is economically active…edged up to 65% in April from 64.9% ?in ?the prior month, StatCan said. A ?higher participation rate along with a higher unemployment rate indicates more people were searching for work.

The Bank of Canada said in its ?Monetary Policy Report last month ?that indicators such as the employment rate, ?hours worked and job vacancies suggest slack, or underutilized capacity, in the labour market, although layoffs remain modest. The looming uncertainty around the future of the North American free trade deal and the knock-on impacts of the higher prices from the ?Iran war has continued to layer over the impact of US tariffs on the economy for over a year. Subdued economic growth indicates tough times in the job market were likely to continue in 2026.

– Stronger US jobs data… The US economy added 115,000 jobs in April, government data showed Friday. Economists surveyed by the Wall Street Journal had forecast a gain of 55,000. The unemployment rate held steady at 4.3% as expected. Signs of a solid US labor market will reinforce expectations the US Federal Reserve will be reluctant to resume cutting interest rates as policymakers assess the inflationary impact of a surge in crude oil prices as a result of the Iran war.

– El Nino causing heat wave in Asia, food inflation upticks… Asia is grappling with a new threat to inflation on top of an oil shock as a looming El Ni o brings soaring temperatures and dry weather to countries from India to New Zealand, driving up food costs. Inflation accelerated to multiyear highs across much of Asia, latest figures showed, led by higher transport, logistics and utility costs. The biggest spikes were in the Philippines and Pakistan, where inflation soared above 7% and to 11%, respectively, said a Bloomberg report.

Those pressures could intensify further as El Ni o is forecast to bring drier conditions and hotter weather later this year. Those threats could be compounded if governments impose export restrictions to protect domestic food supplies, similar to 2022 and 2023 in the wake of Russia s full-scale invasion of Ukraine and extreme weather in some countries. Upward pressure on food prices will likely only be more visible from the second-half of the year as a recent surge in fertilizer costs driven by the Middle East conflict will take time to feed into food prices, economists warn, said the report.

– US federal court disavows Trump s 10% global tariffs… US President Trump s 10% global tariffs were declared unlawful by a federal trade court in a fresh blow to the administration s economic agenda, just months after the US Supreme Court vacated earlier levies he d imposed. A divided three-judge panel at the US Court of International Trade in Manhattan granted a request by a group of small businesses and two dozen mostly Democrat-led states to invalidate the tariffs. Trump imposed the 10% duties in February under Section 122 of the Trade Act of 1974, which had never previously been invoked.

– Russia’s IKAR cuts 2025/26 wheat export forecast… Russia’s IKAR consultancy said it had cut its 2025/26 wheat export forecast for the world’s biggest wheat exporter to around 44.5 MMT from 46.0 MMT previously. IKAR’s head, Dmitry Rylko, said that the downgrade was linked to the strong rouble, which makes exports less profitable, and to a seasonal slowdown in exports towards the end of the marketing season.

– World vegoil prices hit nearly 4-year high… The UN Food and Agriculture Organization s Food Price Index rose 1.6% in April, a third straight monthly rise that puts it up 2% from a year ago, amid rising energy prices and supply disruptions resulting from the Iran war. Vegetable oil prices jumped 5.9% from March, to hit its highest level since July 2022. The gains were largely driven by the prospect of higher demand from the biofuel sector, with several countries taking steps to incentivize production. Support also comes from fears of lower production in Southeast Asia, the FAO noted.

– China soybean imports jump in April… China’s soybean imports rose sharply in April from the same month last year, although shipments were slightly below forecasts made by analysts expecting a surge of arrivals from the US and Brazil. Soybean imports in April came in at 8.48 MMT, more than double the 4.02 MMT notched in March and up 40% on year. Imports averaged 9.3 MMT a month last year. Analysts expect soybean arrivals from April to June to average above 10 MMT per month as more US shipments and Brazil’s record crop reach Chinese ports.

Traders are watching a summit between US President Trump and his Chinese counterpart Xi Jinping on Thursday and Friday for clues about future Chinese purchases of US soybeans.

From January to April, total soybean arrivals in the world’s biggest buyer totalled 25.2 MMT versus 23.19 MMT over the same period last year.

Outside Markets

The Dow Jones Industrial Average edged up 12.19 points on Friday to settle at 49,609.16, and the S&P 500 closed up 61.82 points at 7,398.93. Canada s S&P/TSX composite stock index rallied 221 points higher to finish Friday at 34,078.

Global stock markets are mixed coming into this morning as stalled US-Iran peace negotiations ?weighed on risk appetite. Early Monday, the June Dow Jones Futures are down 9 points. TSX futures are also the red.

The conflict in the Middle East is now entering its 11th week, noted Bruce Kasman, global head of economics at JPMorgan. Energy prices have surged but remain at levels that are headwinds rather than expansion-ending obstacles.

The June US Dollar Index is up 0.011 at 97.995. The Canadian dollar strengthened against its US counterpart…currently quoted at 73.21 US cents.

June crude oil futures are up $1.48 at US $96.90/barrel. Oil prices are up a day after US President Trump said Iran s response to a US peace proposal was unacceptable, raising supply fears as the Strait of Hormuz stayed largely closed, which kept the global market tight.

The oil market continues to trade like a geopolitical headline machine, with prices swinging sharply based on every comment, rejection, or warning coming from Washington and Tehran, said Priyanka Sachdeva, senior market analyst at Phillip Nova.

Grain Markets

Chicago soybean futures are trading 7 to 10 cents/bu higher this morning. Bean futures were higher on Friday, with contracts 10 to 17 cents in the green at the close. July soybean futures gained 4.75 cents higher on the week.

Soymeal futures are up $2 to $3/ton this morning after gaining was up 80 cents to $2.50/ton on Friday, with July up 40 cents on the week. Soyoil futures are 55 to 61 points higher right now after ending 17 to 45 points higher on Friday, with July slipping 84 points last week.

Commitment of Traders data indicated managed money increasing their net long position in CBOT soybean futures as of May 5 by 36,335 contracts, taking they net long position to 221,617 contracts. Specs in bean oil futures extended their record net long position by 3,417 contracts to 169,142 contracts.

USDA s supply/demand report will be out on Tuesday, with a Bloomberg survey of estimates looking for old crop US soybean stocks at 349 million bu, steady with the 350 million bu projected in April. New crop data will also be released, with traders looking for 366 million bu of US bean stocks for September 1, 2027, and a range of 308 to 479 million bu.

Traders seem optimistic about the upcoming US trade talks with China. There are a lot of unknowns, including how much of the negotiations will be about ag trade, or even soybeans specifically, but any potential improvement in demand from the world s biggest buyer of beans would be positive. China continues to largely rely on Brazil for its soybean needs at this time though due to prices and politics.

Chicago corn futures are up 3 to 4 cents/bu this morning. The corn market closed Friday s session with contracts also up 3 to 4 cents across the board, though the July contract was still down 9 cents on the week.

The weekly CFTC Commitment of Traders report from Friday showed managed money increasing their net long in CBOT corn futures by 79,822 contracts to 343,925 contracts as of Tuesday.

Traders looking for old crop US corn stocks estimated at 2.13 billion bu in Tuesday s USDA supply/demand report vs 2.127 billion bu in April. The first 2026/27 US balance sheet will be released for the World Ag Outlook Board, with analysts surveyed by Bloomberg at an average of 1.942 billion bu and a range of 1.776-2.11 billion bu. Brazil and Argentina’s corn outputs are expected to be higher at 133.7 MMT and 56.2 MMT, respectively.

Traders are monitoring US planting conditions, with more near-term rain delays ahead of a generally warmer, drier pattern into later this month. Traders are also watching harvest in Argentina and second crop development weather in Brazil.

US wheat markets are also up this morning across all three markets…generally 6 to 8 cents higher. The US wheat complex traded with gains across the three markets on Friday…spring wheat posted 4 to 7 cent gains at the close, but the July contract still fell 25 cents last week.

Tuesday will see the release of the May USDA supply/demand report, with old crop Us wheat stocks down 8 million bu at 930 million bu according to a Bloomberg survey. New crop data will also be released, with US wheat stocks seen at 845 million bu in a range of 759 to 955 million bu.

The annual Kansas HRW wheat tour will take place this week. The US Drought Monitor shows 70% of US winter wheat growing areas are in some stage of drought, most of that impacting the hard red winter crop. Drier conditions in the northern US Plains recently have allowed for spring wheat planting to proceed, though some areas still experiencing daily low temperatures below freezing has likely slowed farmer activity.

Wheat may have topped, but with the Kansas Wheat Quality Tour this week could that shock the market into causing some weather premium to be added back in to market prices.

I think that we ll all look to the Kansas tour results and the USDA production estimate on Tuesday as kind of giving us what the probabilities are in terms of how small is small. There s some of us that see the US hard red winter wheat crop down in the 575 to 585 million bu region. If it goes below that, then that will be somewhat bullish.

However, the world wheat carryover of old and new crop wheat is still quite adequate. So, there s no immediate overall shortage of wheat in the world.

CANADIAN GRAIN MARKET

ICE canola futures closed strongly higher on Friday, boosted in part by renewed speculative buying ahead of next week s USDA supply/demand report. Strength in Chicago soybeans and soyoil, along with European rapeseed, provided underlying support to canola prices. Ongoing uncertainty surrounding the Iran conflict and its impact on global energy markets also continued to underpin crude oil prices.

Traders were also positioning ahead of key market-moving events next week, including the Trump-Xi summit (May 14-15) and updated global supply/demand estimates from the USDA.

July canola climbed $13.90 on Friday to finish at $753.10/tonne, and November added $14.70 to $757.90.

For today… canola futures are easing lower this morning, down $1 to $2/tonne on the front month contracts. Benchmark July canola futures are down $2.40 at $750.70/tonne after rallying strongly on Friday, though was still down $1.60/t for the week.

Somewhat strange that canola is struggling this morning despite gains in the CBOT soy complex and crude oil. Perhaps canola s rally on Friday got ahead of itself. Nonetheless, the bull trend in canola futures trade remains intact presently. EU rapeseed and Malaysian palm oil futures are also higher this morning.

Grain and oilseed markets are generally leaning higher this morning after last week’s price pressure as the reason for it is now officially debunked. Iran’s response to the US peace proposal was virtually the same as their position was a month ago, and deemed as unacceptable to the US as it was a month ago. Their strategy of outlasting Trump’s patience is clearly working for them, making Trump look even more the fool, with little the world can do than await his next knee-jerk move (probably military escalation). With that, energy markets continued their recovery which are helping most ag markets rally ahead of Trump’s trip to China later this week.

While canola price action is weaker this morning, the relative strength in soyoil continues to lend bullish help to canola, as more countries continue raising biofuel blend mandates. Energy markets will remain a major driver here.

Canadian canola exports hit their highest level of crop year-to-date during the week ended May 3, topping 300,000 tonnes for the first time since April 2025, according to the latest Canadian Grain Commission data. Weekly canola exports of 315,600 tonnes were up by 63% from the previous week and about 90,000 tonnes above the previous five-week average. The solid movement brought the 2025-26 canola export total to 6.5 MMT. While that was still about 1.3 MMT behind the pace at the same time the previous year, the gap is narrowing. Exports had been 1.7 MMT behind the year-ago pace as of March 1, 2026, when China lowered its import tariffs on Canadian canola.

On the feed grains… Feed grain bids in Western Canada continued to show some strength in early May, outpacing corn imports from the United States. Feed barley delivered into Lethbridge-area feedlots was priced at about $310 to $322/tonne at the start of May, having risen $3 to $7/tonne over the last week of April, according to provincial data. Feed wheat ranged from $305 to $317/tonne. Meanwhile, prices for imported US corn continued to lag to the upside, rising by about $4 over the week, with current bids at about $302/tonne delivered into Lethbridge.

Barley prices are in line with where they were at the same time a year ago, while feed wheat is currently about $10 per tonne cheaper. Corn imports from the United States are priced about $20 per tonne lower than at the same time in 2025.

The cheaper US corn continues to find its way into Canadian rations. Canada has imported 484,200 tonnes of US corn from Sept 1 through April 30. An additional 141,700 tonnes are on the books to move later. Corn futures in Chicago hit their highest levels of the past year in sympathy with crude oil, but have since run into some resistance and fallen back.

Supportive seasonal price trends for the Prairie feed grain market should soon start to fade, as temperatures improve and more cattle are moved out to pasture.

Solid export demand continued to underpin the feed barley market, with more grain moving offshore this year. Canadian Grain Commission data shows 2.786 MMT of barley exported through 39 weeks of the marketing year, up by 1.142 MMT from the same point a year ago. Country-specific data through March shows China remains the largest single destination for Canadian barley in 2025-26, accounting about 60% of the movement to date. Japan and Saudi Arabia were also major buyers.

Stay informed with our daily market videos. Each video quickly covers key futures moves, price trends, and market signals that matter to Canadian farmers. Get clear, timely insights in just a few minutes. Bookmark https://www.producer.com/markets-futures-prices/videos

To access the latest futures prices, go to https://www.producer.com/markets-futures-prices/

Source: producer.com